Senior Secured Vs Unitranche: Optimizing Mid-market Capital Structures

Understanding the distinctions between senior secured vs unitranche loans is critical for private equity sponsors navigating mid-market deals. This article clarifies how each debt instrument impacts capital structure, execution speed, and covenant flexibility. Senior secured loans involve distinct first-lien and subordinated debt layers, often from multiple lenders, requiring complex inter-creditor agreements. Unitranche financing, conversely, blends these into a single facility, simplifying deal execution and lender relationships. The choice influences cost of capital and overall financing efficiency for European acquisitions and recapitalizations.

DDTalks provides expert insights into European private credit markets, offering a platform for institutional investors and GPs to understand complex financing strategies. Our content reflects deep industry knowledge, supporting informed decision-making in direct lending and structured finance.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

Understanding the differences between senior secured vs unitranche loans is crucial for private equity sponsors and institutional investors. This article dissects these debt instruments, their impact on capital structures, and the strategic trade-offs for European acquisitions or recapitalizations.

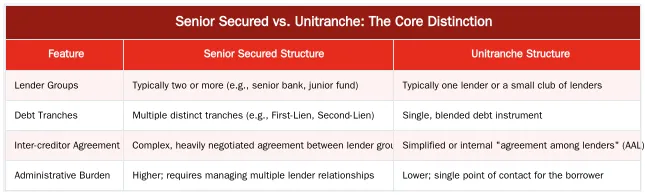

Senior Secured vs. Unitranche: The Core Distinction

The core distinction between a senior secured loan and a unitranche facility is their structure. A senior secured arrangement involves separate layers of debt, typically a first-lien loan and a junior or subordinated piece from different lenders. Unitranche financing combines these layers into a single, blended debt instrument from one lender or a small club of lenders.

What Defines a Senior Secured Loan?

A senior secured loan is the most traditional form of leveraged finance. It is a first-lien loan at the top of the capital structure, giving its holders priority claim on the borrower’s assets in a default. This structure often includes a separate, smaller tranche of subordinated debt (like a second-lien or mezzanine loan) from a different group of lenders. The relationship between these lender groups is governed by an inter-creditor agreement, which defines rights regarding payments, enforcement, and standstill periods.

What is a Unitranche Loan?

Unitranche financing is a streamlined alternative popular in the private credit market. It is a single debt facility that blends the characteristics of senior and junior debt. While technically a first-lien loan, it carries a higher blended interest rate to compensate the lender for risk that would otherwise be allocated to a separate junior tranche. This structure simplifies negotiations and administration by creating a single point of contact for the borrower.

How Do These Structures Impact Capital Stacks?

The choice between these financing options alters a company’s capital structure, influencing financial covenants and fundraising flexibility. The debt stack’s architecture has implications for borrowers and creditors.

The Layered Approach of Senior Secured Debt

A senior debt structure creates distinct layers of risk and reward. The senior lenders have the strongest security and lowest risk, resulting in a lower cost of capital for that tranche. The junior or subordinated debt holders accept a higher risk profile for a higher return. This stratification allows sponsors to source capital from different types of lenders with varying risk appetites, such as commercial banks for the senior piece and specialized credit funds for the junior debt. This complexity requires careful negotiation of the inter-creditor agreement to manage potential conflicts between lender groups.

Unitranche: A Blended Solution for Simplicity and Efficiency

Unitranche financing flattens the capital structure by consolidating debt into one instrument. This eliminates the need for a complex inter-creditor agreement between separate lender groups. For the borrower, this means a single set of covenants, one reporting package, and a unified relationship. The unitranche lender may still have an internal “agreement among lenders” (AAL) if multiple funds are participating, but this is managed away from the borrower. This streamlined approach drives its popularity in European mid-market direct lending.

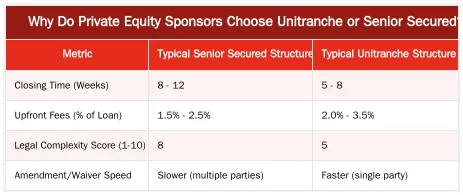

Why Do Private Equity Sponsors Choose Unitranche or Senior Secured?

For private equity sponsors executing leveraged buyouts (LBOs), the financing decision is strategic. It balances pricing, execution speed, and operational flexibility. Each structure offers advantages for different deal situations.

Balancing Speed, Flexibility, and Cost of Capital

Unitranche financing’s primary appeal for sponsors is execution speed. Negotiating with a single lender or a small club reduces the time to close a deal, a key advantage in competitive auctions. Unitranche facilities also offer greater covenant flexibility, as lenders are often more accommodating on terms like leverage multiples and add-backs. In contrast, a senior secured structure may offer a lower blended cost of capital, as banks can price the senior tranche competitively. This cost saving, however, requires a longer, more complex execution process.

The Strategic Role of an Agreement Among Lenders (AAL)

In a senior secured deal, the agreement among lenders (AAL), or inter-creditor agreement, is critical. This agreement dictates the rights and remedies of each creditor class. It can cause friction during negotiations and limit the borrower’s flexibility post-closing. For example, obtaining waivers or amendments may require consent from multiple lender groups with conflicting interests. A unitranche structure largely eliminates this external complexity for the borrower. While an AAL may exist between the unitranche lenders, it is an internal matter that does not typically involve the sponsor, providing greater operational certainty.

European Mid-Market Lending: An Expert Perspective

The European private credit market has evolved, with direct lenders playing a vital role. The senior secured vs unitranche decision is shaped by regional trends and the sophistication of sponsors and lenders.

Current Trends in European Private Credit Markets

The European market has embraced unitranche solutions, driven by capital raised by direct lending funds. According to data from S&P Global Market Intelligence, flexibility and execution certainty make unitranche a preferred tool for mid-market LBOs. Regulatory frameworks like the Alternative Investment Fund Managers Directive (AIFMD II) shape how these funds operate and deploy capital. This environment fosters competition, giving sponsors more options and negotiating leverage.

Optimizing Capital Structures for European LBOs

For European LBOs, the debt structure choice depends on the jurisdiction and target business. For a stable business, a senior loan from a local bank might offer the best pricing. For a complex, high-growth, or cross-border transaction, the speed and bespoke nature of a unitranche facility from a pan-European credit fund is often superior. Understanding these nuances is critical to optimize leveraged buyout financing.

Key Considerations for Your Next Deal

Selecting the right financing requires assessing the transaction, borrower needs, and lender landscape. The optimal choice depends on several factors.

Assessing Deal Complexity and Borrower Needs

Analyze the transaction’s characteristics. Is speed of execution the highest priority to win a competitive bid? Does the company have a complex growth story that requires flexible capital? A stable cash-flow business may be suited for a lower-cost senior secured loan. Conversely, a sponsor undertaking a buy-and-build strategy with multiple follow-on acquisitions may benefit from the simplicity and scalability of a unitranche facility. The comparison between mezzanine capital and private credit also plays into this strategic evaluation.

The Lender Landscape: Direct Lenders vs. Traditional Banks

Lender type is linked to the financing structure. Traditional banks primarily provide senior secured loans and are more conservative, with stricter covenants and lower leverage tolerance. Direct lending funds, which favor unitranche, offer flexibility and speed. They can underwrite larger positions and offer more customized terms. When evaluating senior secured vs unitranche, sponsors must consider their long-term relationship goals and which capital provider aligns with their investment thesis.

Connect with European Private Credit Leaders at DDTalks

Our European financial conferences allow private equity sponsors, institutional investors, and advisors to gain insights from leaders shaping the private credit landscape. Engage with decision-makers to discover the latest strategies in direct lending and structured finance.

Conclusion

The choice between senior secured and unitranche loans is critical in structuring mid-market deals. While senior secured structures can offer a lower blended interest rate, unitranche financing provides advantages in speed, simplicity, and covenant flexibility. For private equity sponsors in Europe’s M&A market, the certainty and efficiency of a unitranche loan often outweigh the cost savings of a traditional approach. Request Agenda for our next conference or contact us to learn more.

Frequently Asked Questions

What is the core structural difference in the senior secured vs unitranche debate?

The primary difference lies in the capital structure. A senior secured deal involves separate debt layers, like a first-lien and a second-lien loan from different lenders. In contrast, a unitranche facility combines senior and junior debt into a single, streamlined loan, simplifying the core senior secured vs unitranche decision.

For private equity sponsors, what are the key advantages in the senior secured vs unitranche comparison?

Private equity sponsors often favor unitranche financing for its speed, certainty of funding, and simplicity. This structure eliminates complex inter-creditor negotiations common in traditional senior secured deals, accelerating the transaction timeline. The choice between senior secured vs unitranche often comes down to the sponsor’s need for execution speed.

From a lender’s risk perspective, how do these two debt structures differ?

A traditional senior secured loan is generally lower risk for a lender because it holds the first-priority claim on a borrower’s assets in a default. A unitranche loan presents a blended risk profile, as the lender is exposed to the entire debt column. This higher risk is compensated with a higher overall yield compared to a standalone senior loan.

How does pricing compare when evaluating senior secured vs unitranche financing?

The all-in yield on a unitranche loan is typically higher than a standalone senior loan to compensate for the blended risk. However, the total cost of a unitranche can be more economical than the combined cost of a separate senior and subordinated debt package. This pricing dynamic is a critical factor in the senior secured vs unitranche evaluation.

How does the choice between a senior loan and a unitranche facility affect a company’s capital structure?

A unitranche loan significantly simplifies a company’s capital structure by consolidating multiple debt tranches into one instrument with a single creditor. This creates greater operational flexibility for the borrower. A traditional senior secured structure involves multiple creditor groups and a more complex intercreditor agreement.

Where can I connect with experts on European private credit financing?

To gain deeper insights and connect with industry leaders discussing the latest trends in European direct lending, you can explore our upcoming private credit conferences. DDTalks gathers top-tier GPs, LPs, and advisors to dissect these financing structures. You can request the full agenda to see our expert speaker lineup.

0 Comments