Single-case Vs Portfolio Funding: Optimizing Distressed Debt Recovery

The choice between single-case vs portfolio funding directly impacts risk, capital deployment, and potential returns in distressed asset recovery. This article details how these litigation finance models differ. Single-case funding invests in one legal claim, carrying concentrated risk. Conversely, portfolio funding spreads capital across multiple legal claims, providing crucial risk diversification. This strategy is often preferred for managing NPL portfolios and complex commercial disputes, offering more predictable returns and aligning with broader asset recovery goals for institutional investors and legal professionals.

DD Talks provides authoritative insights into European private credit, NPL, and distressed debt markets. Our content supports institutional investors and legal professionals in navigating complex financial strategies and optimizing asset recovery outcomes.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

The choice between single-case vs portfolio funding directly impacts risk, capital deployment, and potential returns in distressed asset recovery. These litigation finance models are strategies to unlock value from non-performing loan (NPL) portfolios. This article explains the differences, benefits, and strategic implications for institutional investors, NPL servicers, and legal professionals in European markets.

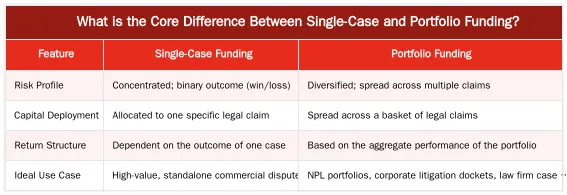

What is the Core Difference Between Single-Case and Portfolio Funding?

The distinction between these litigation finance approaches is the scope of investment and method of risk distribution. Single-case funding is an isolated investment in one legal claim, while portfolio funding spreads capital across a basket of multiple legal claims.

Single-Case Funding: Focused Risk, Individual Returns

Single-case funding is a non-recourse agreement where a third-party funder provides capital for a single lawsuit. The funder’s return is contingent on the outcome of that one case. If the case is lost, the funder receives nothing. This model is best suited for high-value, high-probability standalone claims where the potential return justifies the concentrated risk.

Portfolio Funding: Diversified Risk, Strategic Capital Deployment

Portfolio funding finances a group of legal claims under a single agreement. This provides risk diversification, as the portfolio’s success is not dependent on any single case. Stronger cases can offset losses from unsuccessful ones. This model is favored for managing NPL portfolios and complex commercial disputes because it provides more predictable returns and aligns with broader litigation funding models for asset recovery.

Why is Portfolio Funding Preferred for Distressed Debt Litigation?

Portfolio funding is a more strategic approach for distressed debt than financing claims individually. An NPL portfolio—a collection of assets with varying quality, documentation, and recovery prospects—is ideal for a diversified funding strategy.

Mitigating Inherent Risks in NPL Portfolios

An NPL portfolio contains a mix of claims, some with a high probability of recovery and others that are more speculative. Pursuing each claim individually exposes the investor to the binary risk of each case. Portfolio funding smooths this volatility. By bundling claims, returns from stronger claims can absorb the costs and losses from weaker ones, creating a more stable and predictable return profile for the entire NPL portfolio.

Optimizing Capital Deployment for Asset Recovery

Portfolio funding enables more efficient capital deployment. A funder can assess the portfolio as a whole instead of underwriting dozens of individual claims, reducing transaction costs and administrative burden. This structure aligns the legal strategy with the investment thesis for the distressed asset pool, maximizing asset recovery without over-committing resources to any single, high-risk claim.

Cross-Collateralization and Risk Diversification in Practice

Cross-collateralization and risk diversification are the mechanisms that make portfolio funding effective for distressed assets. They directly impact the performance and stability of an investment in legal claims.

How Cross-Collateralization Strengthens Portfolio Performance

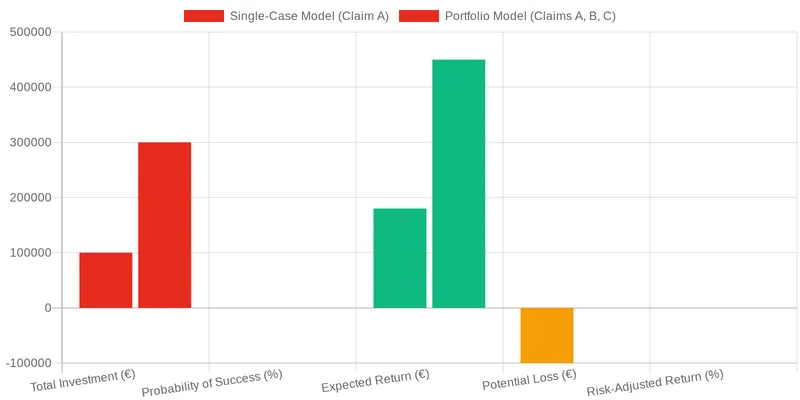

Cross-collateralization is the engine of portfolio funding. Proceeds from all successful cases in the portfolio are pooled to cover legal costs and the funder’s return across all cases—including unsuccessful ones. For example, if a portfolio has ten claims and seven are successful, the proceeds from those seven wins pay for the costs of all ten. This prevents the losses from three unsuccessful cases from creating a net loss, protecting the investor’s capital and enhancing overall returns.

Comparing Risk Profiles: Single-Case vs. Portfolio

A portfolio approach significantly de-risks the investment compared to a series of isolated, single-case bets, a critical factor when managing distressed assets in portfolio management.

Strategic Considerations for Institutional Investors and Law Firms

The choice between single-case and portfolio funding is a strategic decision for institutional investors acquiring distressed assets and the law firms managing their recovery. This topic is often discussed at DD Talks forums, where GPs, LPs, and legal advisors share insights on capital allocation and risk management in European markets.

Aligning Funding Models with Investment Thesis and Deal Flow

For General Partners (GPs) and Limited Partners (LPs), the funding model must align with their investment thesis. An investor acquiring large, diverse NPL portfolios will favor portfolio funding. It enables efficient capital deployment at scale and provides a risk management framework for a diversified asset base. The choice also depends on deal flow; a firm with a consistent pipeline of similar legal claims can use portfolio funding to create economies of scale and secure more favorable terms. This strategic alignment is key for asset recovery and litigation funding.

The Role of Third-Party Funding in European Asset Recovery

The market for third-party funding in Europe has matured, becoming an integral component of asset recovery in financial hubs like London and Madrid. Regulatory frameworks are becoming more defined, providing greater investor certainty. As noted by the European Securities and Markets Authority (ESMA), transparency and standardized practices are improving investor confidence. This ecosystem allows distressed debt investors to partner with specialized funders, transferring legal and financial risk to focus on their core competency of asset management.

Maximizing Value: Outcomes and Future Trends in Litigation Finance

The strategic application of litigation finance directly correlates with maximizing value from distressed assets. The choice between single-case and portfolio funding is a central element of this strategy.

Enhanced Returns and Predictability for Distressed Debt Investors

For investors in distressed debt, portfolio funding creates more predictable cash flows from an otherwise unpredictable asset class. By de-risking the litigation process, it allows investors to pursue more meritorious claims within an NPL portfolio, increasing the overall recovery rate. This predictability is valued by institutional investors who require stable, risk-adjusted returns.

The Evolving Landscape of Legal Claims and Investment Opportunities

The future of litigation finance is expanding beyond commercial disputes into areas like group actions, arbitration funding, and intellectual property claims. As reported by Bloomberg Law, economic shifts lead to new types of legal disputes and investment opportunities. For distressed debt investors, this means future NPL portfolios may contain a more diverse array of legal claims, strengthening the case for portfolio-based funding to manage complexity and optimize returns.

Connect with Industry Leaders at DD Talks Events

DD Talks provides a platform for discussing distressed debt and litigation finance, bringing together key players in European private credit and NPL markets.

Unlock Exclusive Insights and Deal-Making Opportunities

Our exclusive B2B financial conferences facilitate connections and high-value deal-making. Attendees gain direct access to experts, investors, and advisors in asset recovery and capital deployment strategies. Explore trends and forge partnerships. Request Agenda to see our upcoming events in London and Madrid.

Conclusion

The choice between single-case and portfolio funding is a critical strategic decision in distressed debt litigation. While single-case funding suits high-value standalone claims, portfolio funding provides a superior framework for managing NPL portfolio risks through diversification and cross-collateralization. For institutional investors and legal professionals in Europe, leveraging the right model is fundamental to optimizing capital, stabilizing returns, and maximizing asset recovery. To explore these strategies with industry leaders, contact us or Request Agenda for our next event.

Frequently Asked Questions

What is the core difference in the single-case vs portfolio funding debate?

Single-case funding finances one specific legal claim, with the return tied exclusively to its outcome. In contrast, portfolio funding finances a basket of multiple claims, allowing risk to be diversified and returns to be generated from the overall performance of the portfolio. This fundamental difference in scope and risk management is central to the single-case vs portfolio funding decision.

For distressed debt, why is portfolio funding often preferred over single-case funding?

Portfolio funding is often superior for holders of distressed debt because it aligns with their asset base of multiple non-performing loans (NPLs). It allows them to secure capital against a group of recovery litigations, often on better terms, by leveraging diversification to mitigate the risk of any single case failing. This approach provides a more holistic financing solution for large NPL servicers and institutional investors.

What are the main advantages of single-case funding when considering single-case vs portfolio funding?

Single-case funding can be faster to arrange for a high-value, straightforward claim, as due diligence is focused on a single asset. It also avoids cross-collateralization, meaning a successful outcome is not used to offset losses from other unrelated cases. This makes it a viable option in the single-case vs portfolio funding decision for unique, high-probability claims where speed is critical.

How does cross-collateralization impact the single-case vs portfolio funding choice?

Cross-collateralization is exclusive to portfolio arrangements and is a key differentiator in the single-case vs portfolio funding analysis. It means proceeds from successful cases within the portfolio are used to cover the costs of unsuccessful ones. This mechanism is crucial for the funder’s risk mitigation strategy but means the claimant’s overall return is based on the aggregate performance of the entire basket of claims.

Which funding model generally offers better economic terms for the claimant?

Generally, portfolio funding offers more attractive economic terms for the claimant. Because the funder’s risk is spread across multiple cases, they can typically offer a lower share of the proceeds or a lower funding multiple. This contrasts with the higher-risk premium often associated with financing a single, isolated legal action.

How can I learn more about litigation finance trends from industry experts?

To gain deeper insights into litigation finance strategies and connect with leading GPs, LPs, and legal advisors, consider attending a specialized industry event. You can explore the topics and speaker lineup for our upcoming European distressed debt forums. Request the agenda to see how you can join the conversation.

0 Comments