Private Credit Performance: Navigating High-interest Rate Challenges

Private credit performance in a high-interest rate environment presents both opportunities and challenges for institutional investors. This analysis details how floating-rate loan structures enhance direct lending returns for lenders while simultaneously increasing debt servicing burdens and credit risk for European borrowers. Understanding these dynamics is crucial for optimizing private credit portfolios, mitigating default rates, and ensuring resilience amidst economic headwinds. The article explores vintage performance and strategic approaches to portfolio diversification in this evolving market.

DDTalks provides expert insights into European private credit markets, offering a platform for institutional investors and GPs to discuss direct lending strategies and navigate market complexities. Our content reflects the expertise gained from hosting premium B2B financial conferences focused on these critical topics.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

Analysis of private credit performance in a high-interest rate environment shows a tradeoff between enhanced returns and heightened risk. This article examines how rising rates impact direct lending yields, credit quality, and portfolio strategy for institutional investors, covering floating-rate loan mechanics, challenges for European borrowers, and the role of underwriting and active management.

How Does a High-Interest Rate Environment Affect Private Credit Performance?

In a high-interest rate environment, private credit performance is affected through its floating-rate loan structures. As central banks raise benchmark rates, interest payments on these loans increase, boosting yields for lenders. This same mechanism elevates debt servicing costs for borrowers, which can strain their cash flows and increase default risk.

Private credit, direct lending from non-bank institutions to companies, is a significant component of institutional portfolios. Its appeal includes higher potential yields than public debt and a floating-rate structure that hedges against rising rates. While returns initially increase, managers must monitor the secondary effect on borrower health. The outcome depends on balancing higher income against potential credit losses.

Floating-Rate Loans and Direct Lending Returns: A Double-Edged Sword

Most private credit deals are floating-rate loans. This structure benefits investors during rising rates but pressures borrowers, affecting the future of European private credit.

Understanding the Mechanics of Yield Enhancement

Private credit loans are priced as a spread over a benchmark rate, such as the Euro Interbank Offered Rate (Euribor) or the Secured Overnight Financing Rate (SOFR). When these base rates rise, the borrower’s total coupon automatically adjusts upward. This increases a fund’s interest income without renegotiating loan terms.

This mechanism passes higher rates to investors, enhancing direct lending returns and protecting against inflation. Unlike fixed-rate bonds that lose value as rates rise, floating-rate private credit assets can generate higher cash yields, making them an attractive allocation for institutional investors seeking income.

The Rising Burden of Debt Servicing for Borrowers

The mechanism benefiting lenders burdens borrowers. As interest rates climb, so does the cost of debt servicing. For middle-market companies, the primary recipients of private credit, this can impact financial stability. Higher interest payments consume more of a company’s earnings before interest, taxes, depreciation, and amortization (EBITDA), reducing free cash flow for growth, operations, and capital expenditures.

If a company’s revenues do not grow with its rising debt costs, its interest coverage ratio deteriorates, which can lead to covenant breaches and payment defaults. Lenders see higher yields but must prepare for increased portfolio credit stress.

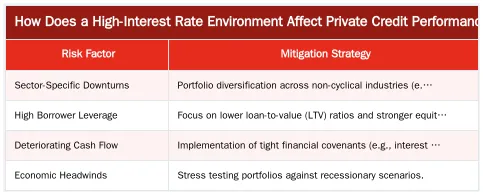

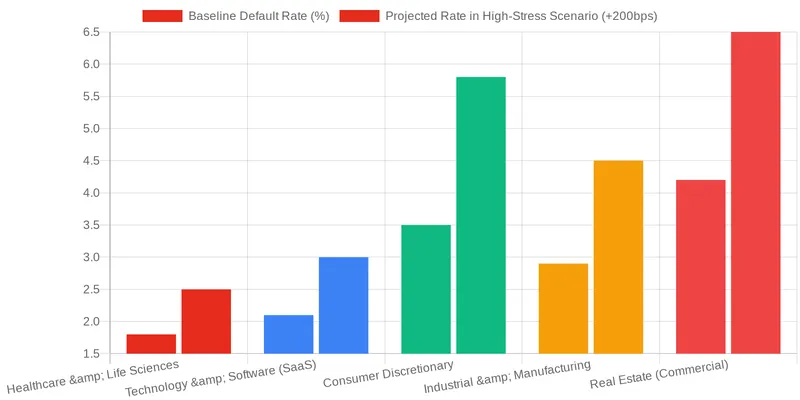

Navigating Credit Risk and Default Rates in European Private Credit

A high-interest rate environment increases focus on credit risk and potential default rates. For general partners (GPs) managing private credit funds in Europe, the challenge is capitalizing on higher yields while managing increased borrower default risk. This requires understanding sector-specific vulnerabilities and implementing risk management frameworks.

Key Drivers of Increased Default Risk

High interest rates heighten default risk. Economic headwinds like slowing GDP growth or inflation can suppress corporate earnings, making debt service harder. Sectors like consumer discretionary or construction may be more sensitive to downturns. Companies with high leverage from low-rate periods are vulnerable to increased borrowing costs.

Rigorous Underwriting and Portfolio Management Strategies

Risk mitigation begins with disciplined underwriting. GPs must conduct due diligence on a borrower’s business model, competitive position, and ability to generate cash flow through economic cycles. Structuring loans with strong covenants provides an early warning system, allowing lenders to intervene before a situation deteriorates.

Active portfolio management is also critical. It involves monitoring borrowers’ financial health, communicating with management teams, and engaging in workouts if a company faces distress. Implementing these European private credit risk management frameworks is fundamental to preserving capital and achieving target returns in a challenging macroeconomic environment.

DDTalks Insights: Expert Perspectives on Private Credit Vintage Performance

DDTalks conference discussions highlight analyzing vintage performance—how funds raised and deployed in different years perform. This perspective is crucial for understanding how the current high-rate environment might shape returns for 2024-2026 vintage funds compared to the low-rate era. Insights from GPs and LPs at our events provide a real-time pulse on market sentiment and strategy.

Analyzing Vintage Performance Through Economic Cycles

Vintages originating during periods of economic stress or higher rates can perform well because lenders can command more favorable terms, including higher spreads, stricter covenants, and lower leverage multiples. While default risk is elevated, structural protections and higher entry yields can compensate for potential losses. In contrast, vintages from low-rate periods may face greater challenges as economic conditions tighten. According to analysis from the Bank for International Settlements, the market’s rapid growth has introduced new complexities that vary by economic cycle.

The Role of Conferences in Shaping European Private Credit Strategy

Events like DDTalks’ Private Credit Days in London and Madrid are a nexus for the European financial community. They provide a platform where GPs, LPs, and advisors dissect market flows, debate regulatory changes like AIFMD II, and identify deal-making opportunities. These interactions help build relationships and align on strategies for complex market conditions. The discussions help shape the industry’s response to challenges like rising default rates and economic uncertainty.

Optimizing Private Credit Portfolios for Resilience and Growth

Navigating a high-interest rate environment requires a strategic approach to portfolio construction and manager selection for institutional investors and LPs. The goal is a resilient private credit allocation that withstands economic headwinds while capturing growth opportunities. This requires diversification and due diligence.

Strategic Diversification Across Sectors and Geographies

Portfolio diversification is a cornerstone of risk management. Investors should seek exposure across industries, avoiding over-concentration in cyclical sectors vulnerable to downturns. Geographic diversification within Europe is also important, as countries experience different economic stress levels. Spreading investments across regions like the UK, DACH, and the Iberian Peninsula mitigates country-specific risks and taps into diverse return sources. Staying informed on market growth trends helps identify these opportunities.

Due Diligence and Manager Selection in Direct Lending

In a challenging credit environment, fund manager skill is paramount. LPs must conduct due diligence on a manager’s track record across economic cycles. Key evaluation criteria include their underwriting process, workout and restructuring experience, and sourcing network. According to data from sources like S&P Global, manager return dispersion widens during downturns, making top-quartile GP selection more critical for private credit performance.

Connect with European Private Credit Leaders at DDTalks Events

Navigating the current market requires timely insights and connections. DDTalks provides a platform for European private credit professionals to explore deal-making opportunities and build partnerships. Our conferences in financial hubs like London and Madrid bring together institutional investors, GPs, and advisors to share knowledge.

Gain access to the decision-makers driving the market. To learn about our upcoming events, contact us or Request Agenda for our next conference.

Conclusion

The high-interest rate environment is a nuanced landscape for private credit. Floating-rate structures offer enhanced returns but increase credit risk and debt servicing pressure on borrowers. Success requires disciplined underwriting, active portfolio management, and manager selection. Understanding these dynamics helps institutional investors position portfolios for resilience and capitalize on opportunities. To connect with industry leaders, join a DDTalks event. Explore our upcoming conferences or Request Agenda.

Frequently Asked Questions

How does a high-interest rate environment affect private credit performance?

A high-interest rate environment can positively impact private credit performance because most loans are floating-rate, which increases yields for investors as base rates rise. However, this also elevates the debt service costs for borrowers, heightening the risk of defaults. Therefore, rigorous underwriting and active portfolio management are crucial to sustain strong results.

Are floating-rate loans the key to strong private credit performance in the current climate?

Yes, the prevalence of floating-rate structures is a primary driver of attractive private credit performance in a rising rate environment. This feature provides a natural hedge against inflation, allowing fund managers to pass on higher base rates directly to investors. This is a significant advantage over fixed-rate credit instruments.

What are the main risks to private credit performance in this environment?

The main risks to private credit performance are increased borrower default rates due to higher debt service burdens and a potential economic slowdown. A weaker economy can impact company earnings, making it harder for them to meet loan obligations. Effective risk management, including robust covenant monitoring and proactive engagement with portfolio companies, is critical to mitigate these challenges.

How do top-tier managers maintain strong direct lending results?

Top-tier managers maintain strong direct lending results through disciplined underwriting, focusing on non-cyclical sectors, and structuring loans with robust covenant packages. They also leverage deep industry relationships and operational expertise to proactively support portfolio companies. This active management approach is key to navigating economic uncertainty and protecting investor capital.

What returns can LPs realistically expect from European private credit now?

While past results are not indicative of future returns, LPs can currently expect European private credit to deliver attractive risk-adjusted returns, often with a significant illiquidity premium over public debt markets. Yields are elevated due to high base rates, but net returns will depend on the manager’s ability to control credit losses. Detailed vintage analysis and manager selection remain paramount for investors.

Where can investors and managers discuss strategies for European private credit performance?

Leading institutional investors, GPs, and advisors discuss strategies for optimizing European private credit performance at specialized industry events. DDTalks conferences provide a dedicated forum for high-level networking and deal-making with leaders from firms like Blackstone, Ares, and Goldman Sachs. You can request the agenda for our next European Private Credit conference to learn more.

0 Comments