EU NPL Regulation: Navigating Europe’s Distressed Debt Markets

Understanding eu npl regulation is essential for participants in European credit markets. This article outlines the EU’s strategy to enhance financial stability by preventing NPL accumulation and fostering efficient secondary markets. It details key frameworks like the Credit Servicers Directive and the NPL Directive, which harmonize cross-border NPL transactions and improve market transparency. Readers will gain insights into optimizing deal-making strategies within this evolving regulatory landscape, preparing for future trends and opportunities in distressed debt.

DD Talks provides expert insights into European private credit and NPL markets. Our platforms connect institutional investors, servicers, and financial professionals with critical regulatory updates and high-value deal-making opportunities.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

The European Union’s regulatory landscape for Non-Performing Loans (NPLs) evolves to strengthen financial stability and foster efficient secondary markets. Understanding eu npl regulation is critical for banks optimizing balance sheets, servicers managing distressed assets, and institutional investors identifying opportunities in European credit markets.

What is the Primary Goal of EU NPL Regulation?

The EU’s primary goal for non-performing loan rules is to strengthen the European banking sector by preventing excessive NPL accumulation and creating a harmonized, efficient secondary market for their resolution. This strategy strengthens financial stability across member states and supports lending to the real economy.

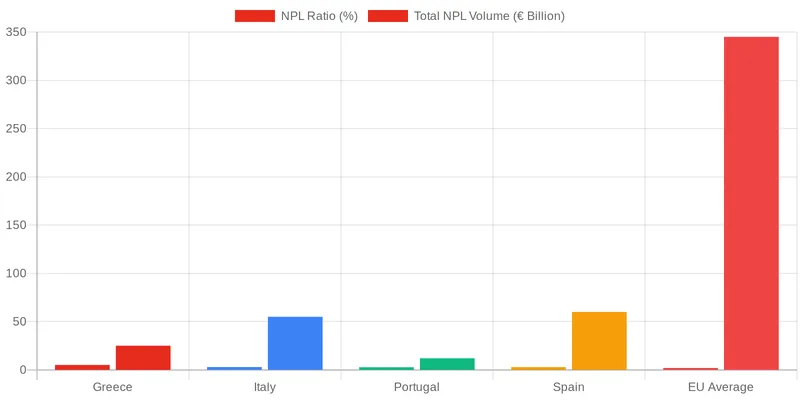

A Non-Performing Loan (NPL) is a loan where the borrower is 90 days or more past due on contractual payments. High NPL levels burden a bank’s balance sheet, tying up capital that could be used for new lending and impacting profitability. The EU’s regulations respond to challenges from the 2008 financial crisis, creating a proactive system for managing credit risk.

The EU’s Strategy to Mitigate Systemic Risk

The strategy has two parts: prevention and resolution. Prevention regulations promote prudent lending and risk management to reduce the likelihood of loans becoming non-performing. Resolution frameworks give banks incentives and tools to manage NPLs. This includes setting minimum loss coverage requirements and facilitating NPL portfolio sales to specialized investors, transferring risk out of the banking system and improving financial institutions’ health.

How Do Basel III Endgame & AIFMD II Shape NPL Strategies?

Broader financial regulations impact NPL strategies for banks and investors. Finalized global banking standards and updated fund management rules create new incentives and constraints for market participants.

Basel III Endgame’s Influence on Bank NPL Portfolios

The `Basel III Endgame` reforms standardize the calculation of risk-weighted assets (RWAs), impacting bank capital requirements. These rules increase the capital cost of holding higher-risk assets, including NPLs and certain real estate loans. This capital pressure prompts banks to accelerate balance sheet optimization, often by selling non-core or non-performing asset portfolios. The market anticipates increased NPL transaction volumes as banks offload these capital-intensive assets before the 2026 implementation deadlines. This trend affects securitisation structures used by banks for capital relief.

AIFMD II’s Implications for NPL Fund Structures and SRT

The updated Alternative Investment Fund Managers Directive (`AIFMD II`) affects private credit and distressed debt funds. The directive enhances rules on delegation, reporting, and liquidity management. It increases scrutiny on funds engaged in loan origination, establishing common `loan origination standards` across the EU. This affects funds that purchase NPLs and provide new financing or restructuring solutions. The regulatory environment shapes the use of `Significant Risk Transfer` (SRT) transactions, a securitisation where banks sell a portion of a loan portfolio’s credit risk to investors to reduce their RWA. Understanding AIFMD II and SRT structuring is critical for funds partnering with banks on capital relief trades, as detailed in the implications of AIFMD II for private credit.

Optimizing NPL Deal-Making in a Regulated Landscape

Executing NPL transactions in Europe requires understanding the regulatory environment. Navigating European NPL rules is a key determinant of investment success, a theme highlighted at our NPL & Distressed Debt Forums. GPs and LPs emphasize that while harmonization has progressed, local market nuances remain critical.

Effective deal-making requires due diligence on the requirements of the Credit Servicers Directive and EBA guidelines. Investors must verify seller data compliance and servicer authorization. A theme from industry events in London and Madrid is the importance of data quality and technology platforms in streamlining compliance and portfolio management.

Strategic Approaches for Cross-Border NPL Sales

Cross-border NPL transactions present challenges. Differences in national insolvency laws, judicial system efficiency, and tax treatments impact the recovery process and returns. A successful strategy, detailed in our guide to Europe’s NPL markets, involves partnering with local experts. This combination of pan-European regulatory understanding and local execution capability is key for successful investors. Building these partnerships is a focus for industry forum attendees.

The Future of EU NPL Markets: Trends and Opportunities

The European NPL market will remain active, shaped by the macroeconomic environment and implementing regulatory frameworks. Elevated interest rates and slowing economic growth in 2026 are expected to create new NPLs, particularly in sectors like commercial real estate and SME lending.

Emerging NPL Asset Classes and Geographic Focus

While secured real estate loans have dominated the market, investors are focusing on other asset classes. Granular portfolios of unsecured consumer loans and SME debt are more common. Interest is growing in “Unlikely-to-Pay” (UTP) assets, which require more restructuring expertise than traditional NPLs. While Italy and Spain remain active, opportunities are emerging in Central and Eastern Europe (CEE) as their banking systems align with EU standards.

| Regulatory Framework | Primary Impact on Banks | Primary Impact on Investors | Primary Impact on Servicers |

|---|---|---|---|

| NPL Directive / CSD | Standardized process for selling NPLs; enhanced data requirements. | Improved market access; greater transparency and data availability. | EU-wide operational passport; harmonized authorization and supervision. |

| Basel III Endgame | Increased capital pressure to dispose of high-risk assets, including NPLs. | Potential for increased supply of NPL portfolios from banks. | Indirect impact through increased transaction flow from banks. |

| AIFMD II | N/A (primarily affects the buy-side). | Enhanced reporting and governance; rules for loan origination activities. | Increased due diligence requirements from fund clients. |

Connect with Industry Leaders at Our NPL & Distressed Debt Forums

Navigating the European NPL market requires timely information and connections. Our NPL & Distressed Debt Forums provide a platform for institutional investors, servicers, and financial advisors to analyze market trends and regulatory shifts. Gain insights from deal-makers and build relationships to execute transactions. Request Agenda for our upcoming events or contact us for participation opportunities.

Conclusion

The evolving framework for eu npl regulation is reshaping the European distressed debt landscape. By fostering transparency, harmonizing rules, and creating incentives for banks to manage credit risk, these initiatives build a more mature, resilient secondary market. This regulated environment presents opportunities for informed investors and specialized servicers. Staying ahead requires continuous learning and industry engagement. Join the conversation at our next forum to gain strategic insights. Request Agenda to see our upcoming topics and speakers.

Frequently Asked Questions

What is the primary goal of the current eu npl regulation?

The primary goal is to strengthen the EU banking sector by preventing the future build-up of non-performing loans and fostering a more efficient secondary market for their disposal. This comprehensive approach to eu npl regulation involves harmonizing rules for credit servicers and encouraging banks to proactively manage distressed assets, thereby enhancing overall financial stability.

How does the Credit Servicers Directive impact the NPL market?

The Credit Servicers Directive is a key piece of the EU’s NPL framework that creates common rules for the regulation and supervision of credit servicers. It allows authorized servicers to operate across the EU with a single ‘passport’, which significantly simplifies cross-border NPL transactions and boosts market integration.

What role do EBA guidelines play within the broader European NPL rules?

The European Banking Authority (EBA) guidelines set out prudent and consistent practices for banks in managing their non-performing exposures. They cover critical areas like NPL strategy, governance, forbearance, and collateral valuation. These guidelines push banks towards more realistic provisioning and timely resolution of bad loans, aligning their internal processes with regulatory expectations.

How does the evolving eu npl regulation create opportunities for investors?

This stringent eu npl regulation forces banks to continuously manage and sell down their NPL portfolios, ensuring a consistent supply of assets for the secondary market. Furthermore, the harmonization of rules reduces legal fragmentation and uncertainty, making it easier and more attractive for institutional investors to operate and deploy capital across different EU member states.

What is the ‘prudential backstop’ component of the eu npl regulation?

The prudential backstop is a critical component of the eu npl regulation that requires banks to set aside a minimum amount of capital against their non-performing loans. This rule acts as a strong incentive for banks to resolve NPLs in a timely manner, either through sales or write-offs, rather than letting them age on their balance sheets. It directly supports the goal of reducing legacy NPL stocks within the European banking system.

How can professionals stay updated on the latest trends in European NPLs?

Staying current requires engaging directly with market leaders and regulatory experts. Attending specialized industry events, such as our NPL & Distressed Debt Forums, provides direct access to insights on deal-making, workout strategies, and the future of the market. You can request the latest agenda to see the topics and speakers shaping the industry.

0 Comments