EU NPL Directive: Streamlining Cross-border Loan Servicing

The eu npl directive, Directive (EU) 2021/2167, establishes a harmonized framework for non-performing loan (NPL) sales and servicing across the EU. This directive streamlines cross-border loan servicing by introducing a single authorization regime and passporting rights for credit servicers, significantly reducing administrative burdens. It aims to foster a more efficient NPL secondary market, enhancing financial stability by enabling banks to offload distressed assets. The framework standardizes compliance requirements for loan purchasers and servicers, creating new opportunities for investors in European distressed debt.

DDTalks provides authoritative insights into European private credit and NPL markets, drawing from extensive experience in organizing premier financial conferences. This content reflects our commitment to delivering accurate, timely information on critical regulatory developments impacting institutional investment and deal-making.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

The eu npl directive, Directive (EU) 2021/2167, creates a more efficient, integrated secondary market for non-performing loans (NPLs) by harmonizing rules for credit servicers and purchasers. This article analyzes the directive’s impact on cross-border loan servicing, investor opportunities, and compliance requirements. The framework reshapes investment strategies and facilitates deal-making across the European distressed debt landscape.

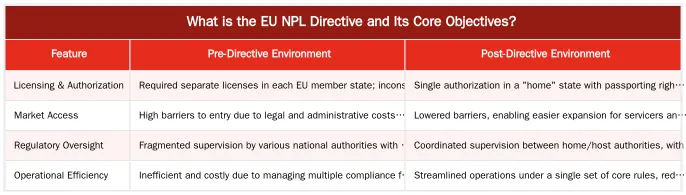

What is the EU NPL Directive and Its Core Objectives?

Directive (EU) 2021/2167 addresses high levels of non-performing loans on bank balance sheets by fostering a secondary market. It creates a harmonized legal framework for the sale and servicing of NPLs across the European Union. This enhances financial stability by allowing banks to offload distressed assets more efficiently, freeing up capital for new lending and strengthening the banking system. The directive prevents future NPL accumulations by making their disposal a more standardized and transparent process.

Key Provisions for Credit Servicers and Purchasers

The regulation introduces common rules for credit servicers and credit purchasers. For credit servicers, the directive establishes a mandatory authorization regime. Entities servicing NPLs on behalf of a purchaser must obtain a license from their home member state’s national competent authority. This authorization includes strict requirements for governance, operational procedures, and consumer protection.

For credit purchasers, the directive imposes information and notification obligations. When selling an NPL portfolio, credit institutions must provide prospective buyers with information to assess its value and risks. Purchasers must appoint an authorized credit servicer (or be one themselves) to manage the loans, ensuring servicing activities adhere to harmonized EU standards. This standardization is a core component of the evolving regulatory environment for EU NPL transactions.

How Does the NPL Directive Streamline Cross-Border Loan Servicing?

The credit servicers directive directly impacts cross-border loan servicing. Previously, servicers operating in multiple EU countries faced fragmented national licensing requirements, creating significant administrative burdens and operational costs. This complexity was a major barrier to entry and limited the secondary NPL market’s efficiency.

The framework introduces a single, harmonized authorization process, allowing servicers and investors to operate on a pan-European scale with greater ease and predictability. By reducing legal and administrative friction, the directive encourages competition among servicers, leading to better service quality and more favorable terms for loan purchasers. This approach helps create a liquid, integrated European market for distressed assets.

The ‘Passporting’ Mechanism for EU Credit Servicers

Passporting rights are central to this streamlining. Once authorized in one EU member state (its “home” state), a credit servicer can provide services in any other member state (a “host” state) without obtaining a separate license. The servicer notifies its home authority, which then communicates with the host authority.

This passporting mechanism applies a principle from other EU financial services to NPL servicing. The European Banking Authority (EBA) ensures consistent application of the rules and fosters supervisory convergence among national authorities. This system replaces disparate national regulations with a coherent, EU-wide framework, enabling servicers to scale their operations and follow investment capital.

Unlocking Secondary Market Potential: Opportunities for Loan Purchasers

The directive makes European NPL secondary markets more attractive for loan purchasers, including institutional investors, private credit funds, and distressed debt specialists. By standardizing rules, the regulation reduces uncertainty and transaction costs. Transparency is enhanced; credit institutions must provide more detailed and standardized information on NPL portfolios before a sale, allowing more accurate due diligence and asset valuation.

Improved data availability and a larger pool of authorized cross-border servicers create a more liquid and competitive market. Investors can access opportunities across more jurisdictions with greater confidence in the operational and regulatory framework. This facilitates efficient capital allocation and supports sophisticated investment strategies for different distressed assets, from corporate loans to secured real estate debt. For example, the EU directive opens Cyprus’s troubled loan market to foreign investors.

Strategic Investment in European NPLs Post-Directive

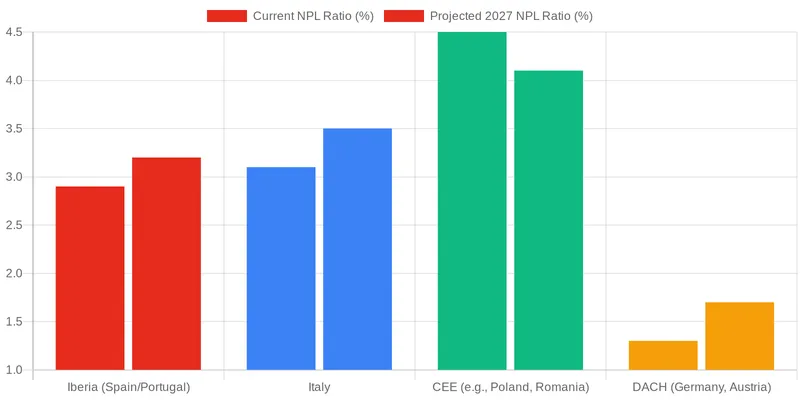

The harmonized framework opens new strategic avenues for investors. Markets in the Iberian Peninsula (Spain and Portugal) and Central and Eastern Europe (CEE), previously presenting both opportunities and regulatory complexities, are now more accessible. Partnering with a single, pan-European servicer to manage portfolios across these regions simplifies operations and allows investors to focus on asset-level strategy.

The directive supports the efficient transfer of large, complex NPL portfolios, which is relevant for large-scale institutional investors. It creates a more predictable environment for structuring deals and managing workout processes. This stability encourages long-term capital deployment into European distressed assets, contributing to legacy NPL resolution and supporting economic recovery in key regions.

Comparing Pre- and Post-Directive Cross-Border Servicing

The eu npl directive has altered the operational and regulatory environment for cross-border servicing. The shift from a fragmented, country-by-country approach to a harmonized, EU-wide system improves market efficiency and accessibility.

Operational Shifts for European Credit Servicers

To leverage the new framework, European credit servicers have made operational adjustments, including investing in internal compliance frameworks that meet the high standards for authorization. Servicers must demonstrate corporate governance, risk management protocols, and fair treatment of borrowers across all jurisdictions. The harmonized licensing procedures are thorough and require significant preparation. Aligning internal processes with the technical standards and guidelines from the European Banking Authority (EBA) is critical for firms operating in this environment.

The Future of European NPL Markets and Investment Strategies

The European NPL market will be shaped by this regulatory framework and interconnected regulations like AIFMD II. The directive is expected to foster greater market depth and liquidity, attracting more international investors. This increased competition and transparency will impact asset valuations and require more sophisticated investment strategies. Private capital will play a crucial role in resolving distressed assets within this clearer regulatory structure.

The focus may shift from large, legacy portfolio sales to more specialized or forward-flow transactions as banks become more proactive in managing their balance sheets. Navigating this evolving market, understanding regional nuances, and building partnerships with compliant, high-quality servicers will be key differentiators for successful investors.

Emerging Trends and Regional Investment Hotspots

As the market matures under the directive, certain regions and asset classes are expected to become investment hotspots. The Iberian Peninsula and Italy have significant volumes of distressed and sub-performing assets, particularly in commercial real estate and SME loans. In CEE, as seen with Croatia’s implementation of the NPL directive, regulatory alignment is creating clearer pathways for investment in corporate debt. These regional and macroeconomic trends are topics explored at industry conferences, providing market intelligence for capital allocation decisions.

Engage with Industry Leaders at DDTalks NPL Forums

Navigating the European NPL market requires access to industry leaders and expert insights. DDTalks’ premium B2B financial conferences in European hubs like London and Madrid provide this. Our events bring together senior-level GPs, LPs, investment bankers, and workout professionals to discuss the impact of regulations like the NPL Directive. Attending provides a platform for networking, deal origination, and staying ahead of market trends in European distressed debt and private credit.

Conclusion

The eu npl directive reshapes the European distressed debt market. By harmonizing rules and introducing passporting rights for credit servicers, it creates a more efficient, transparent, and integrated secondary market for non-performing loans. The framework presents opportunities for investors and servicers who can navigate the compliance requirements. To learn more about upcoming NPL and distressed debt forums, contact us or Request Agenda for our next event.

Frequently Asked Questions

What is the primary goal of the EU’s NPL Directive?

The primary goal of the eu npl directive, officially Directive (EU) 2021/2167, is to create an efficient secondary market for non-performing loans within the European Union. It achieves this by harmonizing the rules for credit servicers and credit purchasers. This framework reduces barriers to cross-border NPL transactions and promotes overall financial stability.

How does the eu npl directive impact cross-border loan servicing?

The directive introduces a “passporting” system, allowing authorized credit servicers in one EU member state to operate in others without needing separate authorization. This key provision of the eu npl directive simplifies cross-border loan servicing, reduces operational costs, and increases competition among servicers. It effectively creates a more integrated and efficient single market for NPL management.

What new compliance rules does the eu npl directive introduce?

The new framework imposes significant compliance requirements, including a mandate for credit servicers to obtain authorization in their home member state. The eu npl directive also sets out specific conduct rules, governance standards, and robust obligations regarding the protection of borrowers’ rights. These measures ensure a consistent and high standard of practice across the Union.

How does the directive affect non-EU investors purchasing NPL portfolios?

The directive directly impacts non-EU credit purchasers by requiring them to appoint an EU-based and authorized credit servicer to manage the NPL portfolio. This ensures that all non-performing loans within the EU are managed by regulated entities subject to the directive’s harmonized standards. This requirement maintains regulatory oversight regardless of the purchaser’s location.

When did the new NPL regulations become applicable?

EU member states were required to transpose the directive into their national law by 29 December 2023. As a result, the new harmonized regulations have been applicable to all relevant NPL transactions and servicing activities since 30 December 2023. This timeline is critical for all current and future deal-making in the European distressed debt market.

How can I learn more about investment strategies under the new NPL framework?

To gain expert insights and discuss investment strategies in the post-directive landscape, we recommend engaging with industry leaders at our specialized NPL and Distressed Debt Forums. You can explore the key topics and expert speakers by visiting our website to request the latest event agenda. This is the premier venue for connecting with key servicers, investors, and advisors.

0 Comments