ESG Covenants: Structuring Sustainable Finance in European Direct Lending

ESG covenants in European direct lending agreements contractually link a borrower’s sustainability performance to their cost of capital. This guide details how these provisions integrate measurable environmental, social, and governance objectives into credit facilities, moving beyond traditional financial metrics. Readers will understand the function of ESG-linked loans, including the role of Sustainability Performance Targets (SPTs) and Key Performance Indicators (KPIs) in driving the margin ratchet mechanism. The article also navigates the relevant regulatory landscape, such as the EU Taxonomy and SFDR, and outlines best practices for structuring effective ESG covenants.

DDTalks specializes in organizing premium B2B financial conferences across Europe, focusing on private credit, direct lending, and structured finance. Our content provides practical insights for institutional investors, GPs, and LPs navigating complex market dynamics and regulatory shifts.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

esg covenants in European direct lending agreements contractually link a borrower’s sustainability performance to their cost of capital. These provisions move beyond traditional financial metrics to incorporate measurable environmental, social, and governance objectives directly into credit facilities.

What Are ESG Covenants in European Direct Lending?

In European direct lending, ESG covenants are binding clauses within a loan agreement that tie financial terms to a borrower’s performance on environmental, social, and governance goals. Unlike traditional financial covenants focused on credit risk, these provisions create a direct incentive for corporate responsibility. The core mechanism links the loan’s interest rate margin to achieving specific Sustainability Performance Targets (SPTs), creating financial consequences for the borrower’s ESG outcomes.

Integrating these terms allows lenders to align portfolios with sustainability objectives and manage long-term risks, while borrowers can reduce financing costs by demonstrating progress on material ESG issues. The framework holds companies accountable for their sustainability commitments and encourages continuous improvement.

Defining Sustainability Performance Targets (SPTs)

Sustainability Performance Targets (SPTs) are specific, measurable, and time-bound goals a borrower must achieve under an ESG-linked loan. Effective SPTs are ambitious yet realistic, aligning with the borrower’s core business strategy and addressing material ESG risks and opportunities. For example, a manufacturing company might set an SPT to reduce its Scope 1 and 2 greenhouse gas emissions by a certain percentage by 2026, or a services firm might target an increase in female representation in senior management.

The loan structure’s credibility depends on its SPTs’ quality. They must be quantifiable and verifiable, often requiring third-party assurance for integrity. The selection process involves negotiation between the lender and borrower to identify targets that are meaningful for sustainability impact and central to the company’s long-term value creation.

How Do ESG-Linked Loans Function in Practice?

ESG-linked loans connect a borrower’s sustainability performance to financial outcomes. The process begins by identifying material ESG issues for the borrower’s industry. The lender and borrower then select Key Performance Indicators (KPIs) to track progress, which form the basis for setting ambitious Sustainability Performance Targets (SPTs) for the loan’s term.

Performance against SPTs is typically measured annually and verified by an independent third party. The results directly influence the loan’s interest rate through a margin ratchet. This mechanism ensures the loan’s terms dynamically reflect the borrower’s ESG performance, creating a continuous incentive for improvement. This approach is common in sector-specific private credit investing in Europe, where lenders embed sustainability into their investment theses.

Selecting Key Performance Indicators (KPIs) for ESG Loans

Selecting KPIs is critical for structuring credible ESG-linked loans. KPIs must be relevant to the borrower’s business, material to its stakeholders, and reliably measured and benchmarked. For a logistics company, a relevant KPI might be ‘grams of CO2 emitted per ton-kilometer’. For a technology firm, it could be ‘percentage of data centers powered by renewable energy’ or ’employee turnover rate’.

The goal is to choose a limited number of high-impact KPIs (typically 2-5) reflecting the company’s core ESG strategy. These indicators should be central to operations, not peripheral metrics achieved without meaningful change. The Loan Market Association (LMA) provides principles for selecting ambitious KPIs, emphasizing they be verifiable and comparable where possible.

The Margin Ratchet: Incentives and Penalties

The margin ratchet is the primary financial mechanism in an ESG-linked loan. It is a pricing grid that adjusts the loan’s interest rate margin up or down based on the borrower’s performance against its SPTs. If the borrower meets or exceeds its targets for a given year, it receives a pre-defined interest rate discount (e.g., a reduction of 5-15 basis points).

Conversely, failing to meet targets can trigger a penalty through an increased interest rate. This two-way adjustment creates a balanced incentive structure. The margin adjustment size is negotiated upfront and reflects the SPTs’ ambition and the ESG component’s importance to the financing.

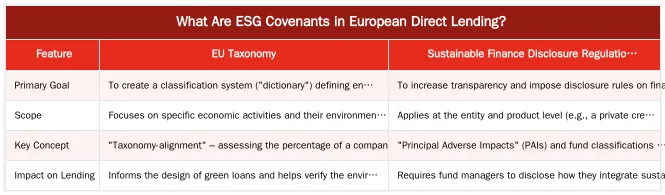

Navigating the Regulatory Landscape: EU Taxonomy & SFDR

The EU’s regulatory framework influences the structure and reporting of sustainable finance products, including direct lending agreements with ESG provisions. Two key regulations, the EU Taxonomy and the Sustainable Finance Disclosure Regulation (SFDR), are central to this landscape. They aim to increase transparency, prevent “greenwashing,” and channel capital towards sustainable activities.

The EU Taxonomy is a classification system defining which economic activities are environmentally sustainable. For direct lenders, it provides a science-based reference for assessing a borrower’s environmental credentials. The SFDR imposes mandatory ESG disclosure obligations on financial market participants, including private credit fund managers. It requires them to report on sustainability risks in their portfolios and the adverse impacts of their investments. These regulations create reporting requirements and define sustainable investment in Europe.

Ensuring Compliance and Reporting

For direct lenders and borrowers, compliance requires data collection, monitoring, and reporting systems. When structuring ESG-linked loans, KPIs and SPTs should, where possible, align with the EU Taxonomy’s technical screening criteria. This alignment helps lenders demonstrate the sustainability credentials of their loan books under SFDR.

Reporting on performance against SPTs must be transparent and backed by independent verification to meet regulatory expectations and maintain market credibility. Borrowers must provide detailed ESG performance data, while lenders must integrate this information into their disclosure reports.

Structuring ESG Covenants: Best Practices for European Direct Lending

Structuring effective esg covenants requires a collaborative, data-driven approach. As discussed at DDTalks’ European private credit forums, market participants emphasize aligning sustainability targets with the borrower’s core business strategy. The provisions should be ambitious enough to drive meaningful change but achievable within the loan’s timeframe. A best practice is to engage external ESG consultants or verifiers early to ensure the chosen KPIs and SPTs are credible.

Negotiations should focus on materiality. Lenders and borrowers should identify the 2-3 ESG issues with the most significant financial and operational impact on the business, rather than adopting generic metrics. This ensures covenants are a tool for risk management and value creation, not a “check-the-box” exercise. Principles from the Loan Market Association (LMA) guide structuring these agreements. Further insights on ESG integration in European private credit strategies highlight this tailored approach.

Differentiating Green Loans from Sustainability-Linked Loans

It is crucial to distinguish between green loans and sustainability-linked loans (SLLs). The key difference is how funds are used and how performance is measured.

Green loans are a “use-of-proceeds” instrument. The loan capital is earmarked exclusively for specific eligible green projects, such as renewable energy installations, energy-efficient buildings, or clean transportation. Covenants in a green loan ensure funds are allocated and tracked for these designated projects.

Sustainability-linked loans (SLLs) are for general corporate purposes. The loan’s financial characteristics, like the interest rate, are tied to the borrower achieving ambitious, pre-defined Sustainability Performance Targets (SPTs). The focus is on the borrower’s overall ESG performance, not a specific project. Most agreements with esg covenants are SLLs, as they incentivize company-wide improvements.

The Future of ESG Covenants in Private Credit: What to Expect

ESG covenants in European private credit are evolving towards greater sophistication, standardization, and breadth. The market is moving from generic targets to bespoke, scientifically-grounded KPIs, particularly those aligned with frameworks like the Science Based Targets initiative (SBTi).

Demand for third-party verification and assurance is increasing. Greenwashing concerns are driving lenders and regulators to require higher standards of data quality and reporting, increasing the role of specialized ESG rating agencies and auditors in loan structuring and monitoring. The scope of these provisions is expanding beyond carbon emissions to include a deeper focus on social impact and governance quality. These principles also influence related fields, like the rise of green and ESG securitisations.

Integrating Social Impact and Governance Metrics

While environmental metrics have dominated ESG-linked finance, the focus is broadening to integrate social and governance KPIs into loan agreements. A company’s long-term resilience and value are linked to its stakeholder relationships and corporate governance.

Social KPIs may include targets for employee health and safety, diversity and inclusion, ethical supply chain management, or community investments. Governance metrics might focus on board diversity, executive pay linked to ESG performance, or anti-corruption policies. As data and measurement methodologies for “S” and “G” factors improve, they will become a standard component of ESG covenant packages in European direct lending.

Connect with European Private Credit Leaders at DDTalks

DDTalks provides a platform for general partners, limited partners, and financial advisors to connect on the latest trends in European private credit and sustainable finance.

Our conferences in London, Madrid, and across Europe facilitate networking and deliver insights from industry experts. Understand how ESG covenants are implemented in practice and discover opportunities in the direct lending space. To connect with key decision-makers, Request Agenda for our upcoming Private Credit Days Europe.

Conclusion

ESG covenants are integral to European direct lending, changing how capital is allocated and corporate sustainability is incentivized. As regulations like the EU Taxonomy and SFDR shape the market, the need for credible, transparent, and ambitious ESG-linked financing grows. Mastering the structure and implementation of these agreements is essential for investors and fund managers in private credit. To engage further, explore upcoming events at DDTalks and Request Agenda to join industry leaders.

Frequently Asked Questions

What are esg covenants in European direct lending?

In European direct lending, esg covenants are legally binding contractual clauses that link a loan’s financial terms to a borrower’s achievement of specific environmental, social, and governance goals. These provisions, often tied to Sustainability Performance Targets (SPTs), create a direct financial incentive for corporate sustainability. Failure to meet these targets can trigger penalties, while success can lead to benefits like a lower interest rate.

How does a ‘margin ratchet’ work with sustainability-linked loan terms?

A margin ratchet is the primary mechanism used in sustainability-linked loans to adjust the interest rate based on performance against agreed-upon targets. If the borrower meets or exceeds its SPTs, the loan’s interest margin is reduced by a pre-agreed number of basis points. Conversely, if the borrower fails to meet the targets, the margin may increase, directly linking financing costs to ESG performance.

What are some common examples of key performance indicators (KPIs) used in esg covenants?

Key performance indicators for esg covenants must be material to the borrower’s business and measurable. Common examples include reducing Scope 1 and 2 greenhouse gas emissions by a set percentage, increasing the representation of women or minorities in senior management, or improving a company’s score from an independent ESG rating agency like Sustainalytics or MSCI.

Are esg covenants legally enforceable in loan agreements?

Yes, esg covenants are fully enforceable contractual terms, just like traditional financial covenants such as leverage or interest coverage ratios. They are integrated into the core loan agreement and are subject to the same legal standards for monitoring, reporting, and enforcement in European jurisdictions.

How do regulations like the EU Taxonomy and SFDR impact sustainability clauses in direct lending?

The EU Taxonomy and Sustainable Finance Disclosure Regulation (SFDR) create a framework that heavily influences sustainability clauses in lending. SFDR requires fund managers to disclose how they integrate sustainability risks, encouraging the use of robust covenants. The EU Taxonomy provides a classification system to define environmentally sustainable activities, helping lenders set credible and standardized KPIs.

How can I learn more about structuring these clauses from industry leaders?

To gain practical insights on structuring and negotiating these complex terms, you can connect directly with leading GPs, LPs, and legal advisors at our European private credit conferences. You can see the full schedule of panel discussions and networking opportunities by requesting the official agenda.

0 Comments