European Private Credit Fund Structures: Navigating Regulatory Frameworks

Understanding european private credit fund structures is crucial for navigating the evolving European private credit market. This guide details the legal and operational frameworks, including the impact of AIFMD II and ELTIF 2.0, on direct lending funds. It explores strategic fund domicile choices like Luxembourg and Ireland, outlining how these decisions influence cross-border lending, regulatory compliance, and investor attraction. Fund managers and institutional LPs gain insights into optimizing structures for efficiency and market access.

DDTalks provides expert analysis on European private credit markets, offering comprehensive guidance on regulatory updates and strategic fund structuring. Our platform facilitates high-level networking and knowledge exchange among industry leaders at premium B2B financial conferences.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

Understanding european private credit fund structures requires knowledge of regulatory frameworks like AIFMD and ELTIF 2.0. The expanding European private credit market offers opportunities for institutional investors and direct lenders. This guide covers the legal forms, regulatory requirements, and strategic domicile choices that shape investment outcomes for fund managers, investors, and legal professionals.

What Are European Private Credit Fund Structures?

European private credit fund structures are the legal and operational frameworks used to pool capital from investors to originate or invest in debt instruments of private companies across Europe. These structures facilitate direct lending, distressed debt, and other credit strategies while complying with complex national and pan-European regulations. The choice of structure dictates how a fund is managed, marketed, and regulated.

These frameworks must balance manager flexibility with investor protection. The legal vehicle, its domicile, and its regulatory status are critical decisions impacting tax efficiency and the ability to distribute the fund across borders. These decisions are heavily influenced by the EU regulatory regime.

The Role of AIFMD in European Fund Structuring

The Alternative Investment Fund Managers Directive (AIFMD) is the primary fund regulation in the European Union. It creates a harmonized framework for managing and marketing alternative investment funds (AIFs), which includes nearly all private credit funds. AIFMD establishes rules on manager authorization, capital requirements, conduct of business, and transparency.

AIFMD provides a “marketing passport” allowing authorized EU AIFMs to market their funds to professional investors across all member states. This passport drives cross-border capital raising but requires significant compliance obligations, including risk management, valuation, and reporting. Understanding the impact of AIFMD II and its predecessors is essential for managers in Europe.

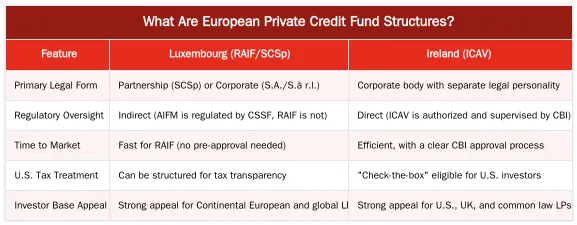

Luxembourg vs. Ireland: Choosing Your European Fund Domicile

Choosing a domicile is a critical decision when establishing a European credit fund. Luxembourg and Ireland are the dominant hubs, offering legal advisors, administrators, and depositaries. Both provide access to the AIFMD marketing passport and offer tax-efficient, flexible fund vehicles.

Luxembourg offers diverse fund structures, including the Reserved Alternative Investment Fund (RAIF) and the Special Limited Partnership (SCSp), popular for private credit strategies. Its network of double taxation treaties attracts funds with a global investor base or complex international investment strategies. The financial regulator, the CSSF, is experienced with alternative assets.

Ireland is popular for its Irish Collective Asset-management Vehicle (ICAV). The ICAV is a corporate structure for investment funds, offering tax transparency (“check-the-box” eligibility for U.S. tax purposes) and operational efficiencies appealing to U.S. and UK-based managers. The Central Bank of Ireland has a pragmatic and accessible regulatory approach.

Strategic Considerations for GPs and LPs

The decision depends on the General Partner’s (GP) needs and the target Limited Partners’ (LPs) preferences. A GP targeting U.S. institutional investors may prefer the Irish Collective Asset-management Vehicle (ICAV) for its tax advantages. A manager focused on German or French LPs might prefer a Luxembourg domicile for investor familiarity and treaty benefits. Operational factors, like the availability of experienced service providers for complex securitisation or direct lending funds, are also crucial.

Structuring for Success: Attracting Institutional LPs and Managing Risk

The internal architecture of european private credit fund structures attracts Limited Partners (LPs). DDTalks industry forums highlight that institutional investors focus on governance, alignment of interests, and risk management. A well-structured fund features a clear investment mandate, a transparent fee structure, and conflict-of-interest policies.

GPs often use a master-feeder structure, using special purpose vehicles (SPVs) to accommodate different investor types or hold assets in specific jurisdictions. This optimizes taxes and isolates risk. For asset-backed finance strategies, securitisation vehicles may be integrated to create tranched notes appealing to investors with varying risk appetites. Legal agreements, including the Limited Partnership Agreement (LPA), must balance GP discretion with LP protections, covering key-person clauses, co-investment rights, and advisory committee roles.

Key Legal and Operational Considerations for Cross-Border Lending

Operating across multiple European jurisdictions is complex. Each country has its own lending licensing requirements, insolvency laws, and tax withholding rules. Effective fund management requires understanding these local nuances. For instance, originating loans in Germany versus Spain involves different legal documentation and enforcement procedures. Managers must work with legal advisors to ensure their direct lending fund structures are compliant and operationally sound for cross-border lending, mitigating legal and tax risks.

The Future of European Private Credit: Trends and Opportunities

The European private credit market in 2026 is shaped by trends influencing fund structuring and strategy. Integrating Environmental, Social, and Governance (ESG) criteria is now required. LPs demand that GPs incorporate ESG risk analysis into due diligence and report on sustainability metrics, leading to the rise of ESG-linked credit funds under Article 8 or 9 of the SFDR.

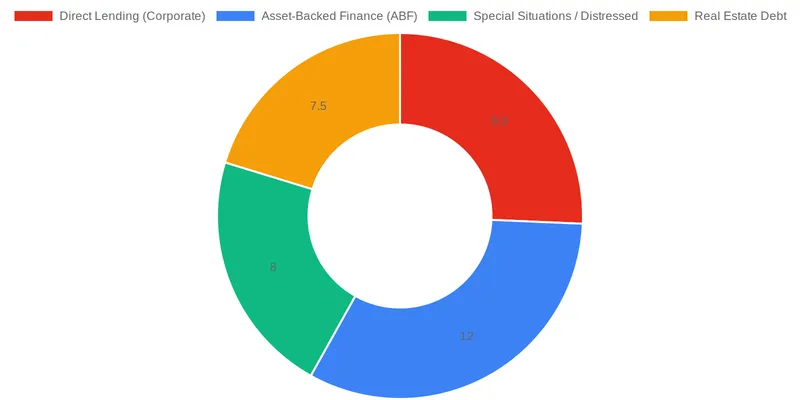

Technology is transforming operations. Fund managers use data analytics and AI for credit underwriting, portfolio monitoring, and risk management, which enhances efficiency and provides a competitive edge in sourcing and evaluating deals. New asset classes are emerging. Asset-backed finance (ABF), including receivables and inventory financing, is a core strategy for funds seeking secured, shorter-duration exposure. This diversification offers opportunities for GPs and LPs.

Connect with Industry Leaders at DDTalks Private Credit Conferences

DDTalks provides a platform for General Partners, Limited Partners, legal advisors, and investment bankers to connect, share insights, and facilitate deal-making. Our conferences in London and Madrid cover the practical implications of AIFMD II, opportunities within ELTIF 2.0, and innovations in fund structuring.

Gain direct access to the decision-makers shaping the asset class. To explore upcoming events, book your ticket. For detailed information on panel discussions and networking opportunities, Request Agenda.

Conclusion

Adapting to regulatory evolution, understanding investor demands, and making strategic choices are key to managing European private credit funds. Decisions on AIFMD II, ELTIF 2.0, and domicile selection between Luxembourg and Ireland impact a fund’s success. Focusing on governance, operational efficiency, and trends like ESG and technology helps managers attract institutional capital and deliver performance. To connect with professionals in this market, contact us or Request Agenda for our next event.

Frequently Asked Questions

What defines the most common european private credit fund structures?

In the European context, private credit fund structures are typically Alternative Investment Funds (AIFs) that pool capital to invest in non-publicly traded debt. These vehicles facilitate direct lending and other credit strategies as an alternative to traditional bank financing. The choice of specific european private credit fund structures, such as a Luxembourg RAIF or an Irish ICAV, depends on the manager’s strategy and target investors.

What is the primary purpose of AIFMD for european private credit fund structures?

The Alternative Investment Fund Managers Directive (AIFMD) creates a harmonized regulatory framework for fund managers operating within the EU. Its main purpose is to enhance investor protection, increase transparency, and manage systemic risk for all alternative funds. This directive is foundational for establishing compliant european private credit fund structures marketed to professional investors.

How does ELTIF 2.0 impact european private credit fund structures?

The updated European Long-Term Investment Fund (ELTIF 2.0) framework makes it easier to launch funds targeting both professional and retail investors. It broadens the scope of eligible assets and offers more flexible rules, making it a more attractive vehicle for certain private credit strategies. This update provides a significant new option for managers considering different european private credit fund structures for long-term capital.

Why are Luxembourg and Ireland preferred domiciles for setting up private credit funds in Europe?

Luxembourg and Ireland are popular domiciles due to their political stability, sophisticated regulatory environments, and deep pools of fund administration expertise. They offer access to the EU marketing passport under AIFMD, allowing managers to raise capital across the Union. Both jurisdictions provide a range of flexible and tax-efficient legal vehicles ideal for these investment vehicles.

Can a single European fund vehicle accommodate both direct lending and distressed debt?

Yes, a single, flexible fund vehicle can be structured to pursue multiple credit strategies. For instance, a Luxembourg special limited partnership (SCSp) or an Irish Collective Asset-management Vehicle (ICAV) can have an investment mandate broad enough to cover both direct lending and opportunistic distressed debt investments. The fund’s specific documentation and risk disclosures to investors are the key determining factors.

How can I learn more about the latest trends in European private credit and connect with fund managers?

Staying current with market trends and regulatory changes is crucial for GPs and LPs. Attending specialized industry events, such as the private credit conferences hosted by DD Talks, provides direct access to leading fund managers, investors, and legal experts. You can request an agenda to see the topics and speakers at our next European forum.

0 Comments