Bank Capital Requirements Npls: Navigating Regulatory Compliance

Bank capital requirements npls mandate that financial institutions hold sufficient capital against non-performing assets to absorb potential losses. This article details how regulatory frameworks like Basel III and the Capital Requirements Regulation (CRR) shape these requirements, impacting bank solvency and CET1 ratios. It explores the calculation of risk-weighted assets (RWA) and the role of prudential backstops in managing provision shortfalls. Understanding these frameworks is crucial for banks and investors navigating the European distressed debt market, ensuring financial stability and compliance with ECB guidance.

DD Talks organizes premium B2B financial conferences, connecting institutional investors, GPs, and NPL servicers across Europe. Our events facilitate high-value deal-making and provide insights into complex regulatory landscapes, including NPL and distressed debt markets.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

Bank capital requirements npls compel institutions to hold sufficient capital against loans at high risk of default. This framework ensures banks can absorb losses from non-performing assets, protecting depositors and maintaining confidence in the financial system. This article analyzes the regulatory landscape, including Basel III and the CRR, the impact of NPLs on solvency metrics like the CET1 ratio, and strategic implications for banks and investors in the European distressed debt market.

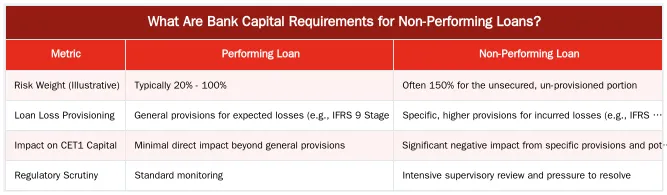

What Are Bank Capital Requirements for Non-Performing Loans?

Bank capital requirements for non-performing loans (NPLs) are regulations requiring financial institutions to set aside more capital for loans where the borrower has failed to make scheduled payments for a period, typically 90 days. This increased capital buffer covers the heightened risk of loss, ensuring the bank remains solvent and stable.

Defining Non-Performing Loans and Their Inherent Risk

A non-performing loan is a loan where the borrower is in default and has not made interest or principal repayments. These assets represent a significant credit risk. The probability of recovering the full loan amount diminishes once a loan becomes non-performing, threatening a bank’s earnings and capital base.

The Core Principle: Why NPLs Demand More Capital

NPLs require more capital for loss absorption. Capital acts as a financial cushion. Because NPLs have a higher likelihood of loss, regulators mandate a thicker cushion. This ensures a bank can write off the loan without jeopardizing its financial health or ability to meet obligations to depositors and other creditors.

How Do Regulatory Frameworks Shape NPL Capital Requirements?

International and European regulations provide a structured approach to managing NPL risks. These frameworks establish minimum capital levels and specific treatments for NPLs to prevent the accumulation of bad debt and fortify bank balance sheets against economic downturns.

Basel III and CRR: Pillars of Prudential Regulation

The Basel III framework, implemented in the European Union through the Capital Requirements Regulation (CRR) and Capital Requirements Directive (CRD), defines the minimum capital banks must hold relative to their risk-weighted assets (RWA). For NPLs, these frameworks assign a higher risk weight, which increases the capital a bank must allocate. These rules dictate the cost of holding distressed assets, making an understanding of the evolving regulatory environment for EU NPL transactions critical for banks and investors.

Understanding the Prudential Backstop for NPL Provision Shortfalls

The CRR includes the “prudential backstop,” a mechanism addressing the risk of NPLs being insufficiently covered by loan loss provisions. It establishes a mandatory timeline for banks to build provisions to cover 100% of the non-performing exposure. If a bank’s provisions fall short of this level (a “provision shortfall”), the shortfall is deducted directly from its Common Equity Tier 1 (CET1) capital. This incentivizes banks to provision adequately or dispose of NPLs promptly.

Impact on Bank Solvency: CET1 Ratios and RWA Calculation

Non-performing assets negatively affect a bank’s key solvency metrics. NPL accumulation erodes capital through increased provisioning and higher risk-weighted assets, pressuring the bank’s ability to meet regulatory thresholds and impacting its market valuation.

NPLs and the Common Equity Tier 1 (CET1) Ratio

The CET1 ratio, a bank’s core equity capital against its risk-weighted assets, is the primary indicator of financial strength. NPLs impact this ratio in two ways. First, loan loss provisions for NPLs reduce retained earnings, a component of CET1 capital. Second, provision shortfalls under the prudential backstop are deducted directly from CET1 capital, further weakening the ratio.

Calculating Risk-Weighted Assets for Non-Performing Loans

Under Pillar 1 of the Basel framework, assets are assigned a risk weight based on credit risk. NPLs are considered high-risk. Exposures not covered by provisions often receive a 150% risk weight, compared to lower weights for performing loans. This higher weighting inflates the RWA denominator of the CET1 ratio, causing the ratio to decrease even if capital remains unchanged. This effect penalizes banks for holding un-provisioned NPLs.

What Are the Future Trends in NPL Capital Requirements?

The regulatory landscape for NPLs evolves as policymakers refine rules to address emerging risks. Future capital requirements will be shaped by new legislation, technological advancements, and market dynamics.

Evolving Regulatory Landscape and Policy Adjustments

The final implementation of Basel III standards (Basel IV) and updates to the EU’s CRR/CRD package (CRR3/CRD6) will introduce refinements. Key areas include the standardized approach for credit risk and an “output floor,” limiting the capital benefit from internal models. As detailed by the Bank for International Settlements, these changes aim to improve the comparability and consistency of capital ratios across banks. For NPLs, this could lead to more standardized and stricter capital treatments, reinforcing proactive management.

Technology and Data’s Role in NPL Management and Capital Optimization

Technology is becoming indispensable for managing NPLs and optimizing capital. Banks and servicers use artificial intelligence and machine learning to improve early warning systems, predict recovery rates, and segment NPL portfolios for effective workout strategies. Better data analytics allows for more accurate valuation and provisioning, which can minimize capital deductions from provision shortfalls. This data-driven approach enables more informed decisions about whether to hold, restructure, or sell distressed assets.

Optimizing Capital Management for NPL Portfolios

Effectively managing non-performing loans is a core component of strategic capital management, not just risk mitigation. The regulatory framework has made passively holding NPLs economically unviable for most banks, necessitating a proactive approach to resolution and disposal.

The Interplay of NPLs, Capital, and Market Confidence

A high non-performing loans to total loans ratio signals asset quality issues that can erode investor and counterparty confidence. By actively managing NPLs and adhering to capital rules, banks strengthen their balance sheets, improve solvency ratios, and demonstrate risk management. This enhances their reputation and access to funding markets.

Strategic Approaches for Banks and Investors in a Regulated Environment

For banks, strategies must focus on early intervention, efficient workout processes, and strategic disposals, which may involve dedicated internal workout units or partnering with specialized third-party servicers. For investors, understanding the regulatory drivers compelling banks to sell is key. This knowledge allows for better timing of market entry and more effective negotiation. Success requires expertise in valuation, legal frameworks, and operational servicing, particularly in complex jurisdictions such as with Italian banks and their non-performing exposures.

Connect with European NPL Market Leaders at DD Talks Events

DD Talks organizes B2B conferences across Europe, bringing together institutional investors, NPL servicers, investment bankers, and regulatory experts. Our events in financial hubs like London and Madrid provide a platform for deal-making, sharing strategic insights, and understanding trends in distressed debt and private credit. Gain direct access to decision-makers shaping the European NPL landscape.

Explore our upcoming forums. Request Agenda for our next NPL and Distressed Debt summit.

Conclusion

Bank capital requirements for NPLs fortify the banking system against credit default risks. Frameworks like Basel III and the CRR, enforced through mechanisms like the prudential backstop, force banks to confront non-performing assets proactively. This regulatory pressure shapes the European distressed debt market, creating a continuous flow of opportunities for investors and servicers. Understanding these capital rules is fundamental to strategic decision-making for all market participants. To deepen your expertise and network, contact us or Request Agenda for our next event.

Frequently Asked Questions

Why are bank capital requirements npls so stringent?

The stringent nature of bank capital requirements npls stems from the high risk of loss these assets pose. Regulators mandate that banks hold more capital against NPLs to absorb potential losses, ensuring the bank’s solvency and protecting the financial system. This capital acts as a crucial buffer against financial instability.

What is the “prudential backstop” for non-performing loans?

The prudential backstop is a regulatory mechanism that requires banks to automatically provision for losses on new NPLs over a specific timeline. This rule directly impacts capital by forcing deductions from earnings. It creates a strong incentive for banks to resolve non-performing assets promptly to avoid the escalating capital impact.

How do non-performing assets affect a bank’s Risk-Weighted Assets (RWA)?

Non-performing loans carry a much higher risk weight than performing loans, which significantly increases a bank’s total Risk-Weighted Assets (RWA). A higher RWA figure directly reduces a bank’s capital ratios, such as the CET1 ratio. This calculation is a fundamental component of how bank capital requirements npls are enforced by supervisors.

How do bank capital requirements npls influence a bank’s decision to sell a loan portfolio?

The pressure from bank capital requirements npls is a primary driver for banks to sell NPL portfolios. By removing these high-risk, capital-intensive assets from their balance sheets, banks can reduce their RWA, improve capital ratios, and free up capacity for new lending. This creates a steady supply of distressed assets for investors in the secondary market.

What are the key considerations for investors regarding bank capital requirements npls?

For investors, understanding the nuances of bank capital rules is critical for identifying opportunities in the distressed debt market. A bank facing significant pressure from its capital position is more likely to sell NPL portfolios at a discount. Therefore, analyzing a bank’s capital adequacy in the context of its NPL holdings can signal potential investment opportunities.

Where can professionals learn more about navigating the European NPL market?

The best way to gain in-depth knowledge and connect with industry leaders is by attending specialized financial conferences. DD Talks events in key European hubs like London and Madrid focus specifically on the NPL and distressed debt landscape, offering direct networking with top investors, servicers, and advisors. You can request an agenda to explore upcoming topics and speakers.

0 Comments