Pan-european Lending: Navigating Cross-border Legal Frameworks

Navigating pan-european lending requires a deep understanding of diverse legal frameworks and regulatory landscapes. This article provides a comparative overview of essential considerations for cross-border financing, including the strategic selection of governing law and jurisdiction clauses. It details how regulations like Rome I and Brussels I facilitate enforcement across member states, alongside practical insights into security perfection and varying insolvency regimes. Understanding these elements is crucial for effective deal structuring and robust risk management in pan-European transactions.

DDTalks provides expert insights into the complexities of European private credit, NPL, and structured finance markets. Our content draws from extensive experience in facilitating high-value deal-making and industry networking at premium B2B financial conferences, offering practical guidance for institutional investors and legal advisors.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

The legal landscape of pan-european lending presents challenges for institutional investors executing cross-border transactions. This article overviews the legal frameworks, regulations, and practical considerations for financing across Europe. It offers a comparative perspective on legal systems—from governing law clauses to security perfection and insolvency regimes—for deal structuring and risk management.

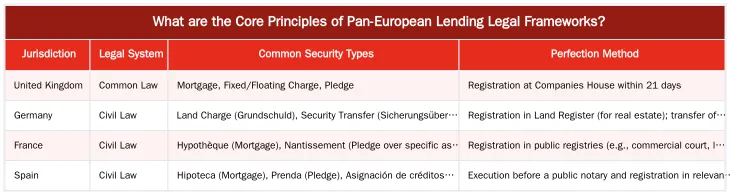

What are the Core Principles of Pan-European Lending Legal Frameworks?

Legal frameworks for cross-border financing in Europe are built on freedom of choice and mutual recognition. Contracting parties can generally select the governing law for their agreement and the courts to resolve disputes. The system creates a predictable legal environment, facilitated by EU regulations that ensure judgments from one member state are recognized and enforced in others, streamlining multi-jurisdictional transactions.

Understanding Rome I and Brussels I Regulations

The Rome I and Brussels I (Recast) Regulations are two pillars of this framework. The Rome I Regulation establishes uniform rules for determining the applicable law for contractual obligations. It upholds party autonomy, allowing lenders and borrowers to choose the governing law in their loan agreements. This choice is, with few exceptions, respected by EU courts.

The Brussels I Regulation (Recast) addresses jurisdiction and the enforcement of judgments. It determines which member state’s courts have jurisdiction in civil and commercial disputes and streamlines the recognition and enforcement of judgments across the EU. This mechanism allows lenders to enforce a judgment against a borrower’s assets in a different member state.

Governing Law vs. Jurisdiction: Key Considerations for Loan Agreements

In cross-border loan agreements, the governing law and jurisdiction clauses are critical. Confusing these concepts is a common error. The governing law clause specifies which country’s substantive laws interpret the contract’s rights and obligations. The jurisdiction clause, or forum selection clause, determines which country’s courts will hear disputes.

For example, a loan agreement between a German lender and a Spanish borrower for a project in France could specify English law as the governing law and the courts of Luxembourg as the chosen jurisdiction. This distinction allows parties to select a predictable legal system for their contract (the “what”) and a neutral or convenient forum for dispute resolution (the “where”).

Strategic Choice of Law and Forum

The choice of law has strategic implications. English law, a common law system, is often chosen for European financing for its flexibility, commercial focus, and extensive case law, which provides predictability. Civil law systems, like those in Germany and France, are more codified and may lack the flexibility of common law for complex financial instruments. Understanding these differences is key to cross-border deal structuring.

Post-Brexit, the UK is not part of the Brussels I framework. While English governing law clauses are respected in the EU under the Rome I Regulation, enforcing English court judgments in the EU is more complex. Enforcement now relies on the Hague Convention on Choice of Court Agreements (for exclusive jurisdiction clauses) or national laws, requiring additional legal consideration.

Navigating Security Perfection and Cross-Border Enforcement in Europe

While governing law can be harmonized by contract, rules for creating and perfecting security interests are typically governed by the law of the asset’s location (lex situs). This creates complexity in multi-jurisdictional financing, as security perfection—making a security interest effective against third parties—varies significantly between countries. Failure to perfect security correctly can leave a lender unsecured in an insolvency.

The divergence between common law and civil law systems is pronounced. The UK’s common law allows for flexible security like the floating charge, covering a shifting pool of assets. Civil law jurisdictions like Germany and France require more specific asset identification and formal registration for perfection. This comparative analysis is necessary for any pan-European security package. The EU’s Financial Collateral Directive has harmonized rules for financial collateral (cash, financial instruments), but for most asset classes, local law prevails.

Comparative Table: Security Perfection Across Jurisdictions

The following table illustrates key differences in security regimes across major European jurisdictions.

How Do European Insolvency Regimes Impact Cross-Border Lending?

When a borrower with assets in multiple EU countries faces financial distress, the European Insolvency Regulation (EIR) applies. The EIR coordinates insolvency proceedings across member states, preventing creditors from initiating parallel proceedings in different jurisdictions. It determines which country’s courts have jurisdiction to open main insolvency proceedings—typically where the debtor has its “centre of main interests” (COMI).

Main proceedings opened in one member state are automatically recognized across all others. This impacts lenders, as proceedings trigger a stay on creditor actions, including security enforcement. The EIR allows the insolvency administrator to manage the debtor’s entire EU-wide estate. The substantive insolvency law applied is generally that of the state where proceedings are opened, making the COMI determination critical.

Strategies for Mitigating Insolvency Risk

Lenders can mitigate cross-border insolvency risks through several strategies. Thorough due diligence into a borrower’s COMI is essential. Security should be structured to be robust under the local laws of key asset locations. The choice of governing law can influence how claims are treated. These dynamics are a core component of risk management frameworks. Upcoming regulations like AIFMD II may introduce new liquidity and risk management requirements for fund managers, influencing how funds approach insolvency.

DDTalks’ Expert Insights: Real-World Challenges in Cross-Border Lending

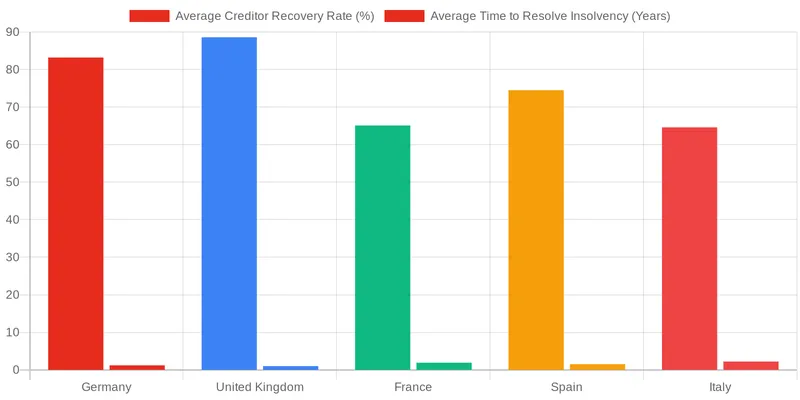

At DDTalks conferences, general partners, limited partners, and legal advisors highlight recurring challenges in cross-border lending. A common pitfall is underestimating the operational and time differences in enforcing security across jurisdictions. A swift out-of-court process in one country can be a lengthy, court-supervised procedure in another, significantly affecting recovery timelines and costs.

Another challenge is the importance of local nuance in due diligence. A superficial understanding of a country’s legal system is insufficient when entering new European markets. Successful managers build networks of local counsel to navigate unwritten rules and court practices not apparent from statutes. This intelligence is used for accurately pricing risk and structuring resilient credit agreements.

Navigating Regulatory Shifts and Market Dynamics

Evolving regulations reshape European financing. The implementation of directives like AIFMD II will impact fund structuring and reporting obligations. The integration of Environmental, Social, and Governance (ESG) criteria into lending decisions introduces new legal and reputational risks. Regulators like the European Securities and Markets Authority (ESMA) note these factors are becoming integral to credit analysis. Understanding these shifts affects deal execution and portfolio management.

Advance Your Pan-European Lending Strategy with DDTalks

A pan-european lending strategy requires current intelligence and industry connections. The complexities of comparative law, cross-border enforcement, and insolvency regimes necessitate continuous learning and networking. DDTalks brings together participants in the European private credit market to share insights for structuring deals and identifying opportunities.

Conclusion

Legal frameworks for cross-border financing in Europe combine EU-level regulations and national laws. A strategic approach requires understanding the interplay between Rome I and Brussels I Regulations, the differences in security perfection between common and civil law systems, and the European Insolvency Regulation. Mastering these legal nuances helps institutional investors and lenders mitigate risk. To learn more, contact us or Request Agenda for our upcoming events.

Frequently Asked Questions

What are the core principles of the EU’s legal frameworks for cross-border financing?

The core principles, established by regulations like Rome I and Brussels I, are freedom of choice and mutual recognition. Parties in a transaction are generally free to choose the governing law and jurisdiction for their contracts. This system creates a predictable legal environment, as judgments from one member state’s court are typically recognizable and enforceable in others, which is fundamental for successful pan-european lending.

Why is creating a single ‘European security interest’ so difficult for pan-European lending?

A single European security interest is challenging because security is tied to national property law, which remains a sovereign matter for each member state. These laws are deeply embedded in diverse legal histories, such as the German Grundschuld versus the English mortgage. Harmonizing this patchwork of national security laws is a complex legal and political task.

How does the Financial Collateral Directive assist in pan-European lending?

The Financial Collateral Directive harmonizes and simplifies the creation and enforcement of security over financial collateral, such as cash and securities. It allows for more efficient enforcement methods, often outside of formal insolvency proceedings. This streamlined process significantly reduces risk and improves efficiency for pan-european lending operations.

Has Brexit complicated pan-European lending structures that use English law?

Yes, Brexit has introduced complexities for financing arrangements governed by English law. While English law remains a popular contractual choice, the automatic recognition and enforcement of English court judgments within the EU under the Brussels Regulation no longer applies. Consequently, structuring a pan-european lending deal now requires reliance on alternative enforcement conventions or specific jurisdiction clauses.

What is a ‘parallel debt’ provision and why is it used in syndicated loans?

A parallel debt provision is a legal technique used in syndicated lending to allow a single security agent to hold and enforce security on behalf of a changing group of lenders. This structure is particularly useful in civil law jurisdictions that may not recognize the common law concept of a trust, thereby ensuring the security remains valid and enforceable for the entire syndicate.

How can our firm deepen its expertise on the latest trends in pan-European lending?

Attending specialized industry conferences is one of the most effective ways to gain expert insights and network with key decision-makers. These events bring together top-tier GPs, LPs, and legal advisors to discuss current market flows, regulatory updates like AIFMD II, and real-world deal structuring. To see how our forums can connect you with industry leaders, you can request the agenda for our next private credit event.

0 Comments