Cross-border Deal Structuring: Navigating European Private Credit Complexity

Cross-border deal structuring in European private credit requires navigating diverse legal, tax, and regulatory frameworks across multiple jurisdictions. This article details the complexities of pan-European lending, focusing on critical aspects like security enforcement, managing withholding tax, and ensuring regulatory compliance. Readers will gain insights into optimizing financing structures, including unitranche and syndicated loans, to mitigate risks and enhance returns in multi-jurisdiction deals. Understanding these challenges is crucial for successful investment and recovery strategies.

DD Talks offers authoritative insights into the intricacies of European private credit markets, equipping institutional investors and advisors with essential knowledge for navigating complex deal environments. Our content focuses on practical strategies for regulatory compliance and effective financing structures.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

Executing cross-border deal structuring in European private credit requires navigating multiple legal, tax, and regulatory systems. Understanding these multi-jurisdictional intricacies helps general partners, limited partners, and their advisors mitigate risk and optimize returns. This article addresses primary challenges, from security enforcement and withholding tax to financing structures like unitranche and syndicated loans.

What is Cross-Border Deal Structuring in European Private Credit?

Cross-border deal structuring in European private credit is the process of designing a financing transaction where the lender, borrower, or collateral assets are in multiple countries. This requires a legal and financial framework that accounts for the distinct laws, tax regimes, and regulatory requirements of each jurisdiction to ensure the loan is profitable and enforceable upon default.

Defining Pan-European Lending and Multi-Jurisdiction Deals

Pan-European lending is direct lending that spans several European nations. A multi-jurisdiction deal might involve a Luxembourg-domiciled fund lending to a corporate group with subsidiaries and assets in Germany, France, and Spain. The core challenge is that while capital flows freely, legal and tax systems remain national.

The structure must harmonize disparate requirements. Lenders must create a security package valid and enforceable in each country, manage tax liabilities like withholding on interest payments, and comply with European and local laws. Complexity increases with the number of jurisdictions involved.

Optimizing Tax and Regulatory Compliance for Pan-European Lending

Tax efficiency and regulatory adherence are critical for multi-jurisdiction deals. Poor tax structuring erodes returns, while non-compliance with regulations leads to penalties and operational disruption.

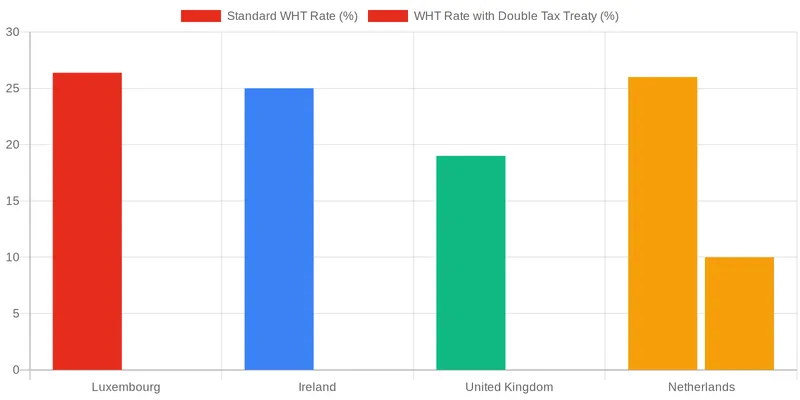

Managing Withholding Tax on Interest Payments

Withholding tax (WHT) is a tax levied by a borrower’s country on interest payments to a foreign lender. Rates can be substantial, directly impacting the lender’s net return. The primary tool for managing WHT is the network of double tax treaties between countries, which often reduce or eliminate this tax.

Structuring the deal to use a favorable treaty is critical. This may involve routing the loan through a holding company or fund vehicle in a jurisdiction with an advantageous treaty network. Formal legal and tax opinions are standard practice to confirm the tax treatment and ensure the structure is sound.

Regulatory Compliance and AIFMD II Implications

The Alternative Investment Fund Managers Directive (AIFMD) governs the regulatory environment for private credit funds in Europe. Upcoming AIFMD II revisions will introduce new rules on loan origination, liquidity management, and reporting, affecting how funds operate across the EU. Fund managers must ensure their structures and marketing comply with these evolving regulations.

This includes the “passporting” regime, which allows a fund manager authorized in one EU member state to manage and market funds across the bloc. Proper European private credit fund structures are needed to leverage these benefits for capital deployment across borders.

| Jurisdiction | Common Security Type | Key Enforcement Consideration |

|---|---|---|

| England & Wales | Share Charge / Debenture | Out-of-court enforcement via an administrator is common and efficient. |

| Germany | Land Charge (Grundschuld) | Requires a notarized deed and registration. Enforcement is a formal, court-supervised process. |

| France | Pledge over Business (Nantissement) | Covers a wide range of business assets but enforcement can be complex and subject to judicial oversight. |

| Spain | Mortgage over Real Estate (Hipoteca) | Highly formalized process requiring public deeds and registration. Enforcement is strictly judicial. |

Structuring for Success: Unitranche and Syndicated Loan Considerations

The choice of financing instrument is fundamental to a multi-jurisdiction deal. Unitranche facilities and syndicated loans are two common structures, each with advantages and complexities in a cross-border context.

Unitranche Financing in Multi-Jurisdiction Deals

Unitranche financing combines senior and subordinated debt into a single loan with a blended interest rate, offering simplicity and speed. In a cross-border scenario, this structure streamlines negotiations by involving a smaller lender group, but the complexity remains in the security package.

The structure requires an intercreditor agreement governing the rights of different lender tranches. When applied across borders, this agreement must function alongside multiple local security documents. The priority of payments and enforcement rights in the intercreditor agreement must be respected under the insolvency laws of each jurisdiction.

Syndicated Loans and Currency Risk Hedging

Syndicated loans involve a group of lenders jointly providing a loan. In a pan-European context, the syndicate may include banks and funds from various countries. This diversifies lender risk but adds administrative complexity, managed by an agent bank.

Currency risk is a critical consideration. If a borrower group generates revenue in multiple currencies (e.g., EUR, GBP, CHF) but the loan is in a single currency, fluctuations can impact the borrower’s ability to service the debt. Currency risk hedging strategies like currency swaps or forward contracts are often integrated into the financing package to mitigate this volatility.

Why Expert Collaboration is Essential for European Deal Structuring

The complexity of pan-European private credit transactions makes expert collaboration necessary. No single party has the knowledge to navigate every legal, tax, and regulatory nuance across multiple countries. Success depends on a network of advisors and industry peers.

The Indispensable Role of Legal and Tax Advisors

Specialized legal and tax counsel in each jurisdiction are part of the deal team. Local lawyers draft and perfect security documents, provide legal opinions on enforceability, and guide the process through local court and registration systems. Tax advisors design structures that mitigate WHT and other tax inefficiencies, ensuring the deal’s economic model is viable.

These advisors work with the lead counsel to create a legally sound, tax-optimized, and commercially practical structure. Their early involvement helps identify roadblocks and design solutions.

DDTalks: Facilitating High-Value Pan-European Deal-Making

Beyond formal advisors, a network of industry peers is a valuable resource. Understanding market conventions, emerging trends, and the experiences of other market participants provides a competitive advantage. Industry forums are important for this.

DDTalks events, like the annual Private Credit Days Europe in London, facilitate this collaboration. They bring together General Partners, Limited Partners, investment bankers, and legal advisors to share insights on these challenges. Panels and workshops cover the practicalities of structuring complex deals, providing access to expertise and partnerships for pan-European private credit transactions, in line with guidance from bodies like the European Banking Authority on financial stability.

Mastering Your Pan-European Strategy

Cross-border deal structuring blends legal and tax engineering with commercial pragmatism. Success in European private credit requires understanding disparate national systems and managing complexity. By prioritizing sound security packages, tax efficiency, and the right financing structure, investors can operate effectively across the continent. A network of expert advisors and industry peers is foundational to this strategy. To deepen your expertise and connect with leaders in European private credit, Request Agenda for our upcoming events or contact us to learn more.

Frequently Asked Questions

What is the main legal challenge in European cross-border deal structuring?

The primary challenge is navigating the diverse national laws for perfecting and enforcing security over assets. While EU regulations provide some harmony, the specific procedures for taking collateral like real estate or shares remain country-specific, complicating any multi-jurisdiction financing. This makes local legal expertise essential for successful cross-border deal structuring.

Why is English or New York law often chosen for pan-European financing agreements?

These common law systems are preferred for their commercial flexibility, extensive legal precedent, and predictability in financial disputes. This provides a stable and well-understood legal framework for the main loan agreement. It gives lenders and borrowers certainty, even when assets are located in various European civil law jurisdictions.

How does cross-border deal structuring address withholding tax issues?

Effective cross-border deal structuring minimizes tax leakage by using tax-efficient lending platforms, often in jurisdictions like Luxembourg or Ireland. Leveraging double taxation treaties between countries is also crucial. The goal is to structure the flow of interest payments to reduce or eliminate withholding taxes, thereby maximizing investor returns.

What defines cross-border deal structuring in the context of European private credit?

This process involves designing a financing transaction where the lender, borrower, or collateral assets are located in multiple European countries. It requires creating a legal and financial framework that accounts for the distinct laws and tax regimes of each jurisdiction. The primary objective of this complex cross-border deal structuring is to ensure the loan is both profitable and fully enforceable.

How critical are local legal advisors in these multi-jurisdiction transactions?

Local legal advisors are absolutely essential for successful European financing. While a lead counsel coordinates the deal, advisors in each relevant country provide opinions on the validity of security, corporate authority, and the enforceability of loan documents under national law. Their input is critical for mitigating legal and operational risks across the continent.

Where can I learn more about advanced European private credit strategies?

Staying updated is key for institutional investors and fund managers. Attending specialized industry events, such as the European private credit conferences hosted by DD Talks, provides direct access to expert-led discussions on multi-jurisdiction financing. You can explore the latest topics and expert speakers by requesting the conference agenda.

0 Comments