AI in NPL Servicing: Enhancing Recovery and Risk Mitigation

AI in NPL servicing is fundamentally reshaping the non-performing loan market by integrating intelligent systems and advanced data analytics. This technology enables servicers to analyze vast datasets, predict borrower behavior, and optimize recovery strategies more effectively than traditional methods. Leveraging machine learning and predictive modeling, NPL professionals can enhance credit risk analysis, automate routine tasks, and achieve more strategic portfolio management. The adoption of AI tools drives operational efficiency, mitigates risk, and boosts profitability across distressed asset portfolios, particularly within the European market.

DDTalks organizes premium B2B financial conferences, providing platforms for industry leaders to discuss advancements in NPL, distressed debt, and private credit markets. Our events facilitate high-value deal-making and knowledge exchange on critical topics like AI’s impact on financial services.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

The non-performing loan (NPL) market is transforming, with ai in npl servicing driving efficiency and profitability. This shift leverages intelligent systems to analyze complex datasets and predict outcomes more accurately than traditional recovery methods. Artificial intelligence and data analytics offer servicers and institutional investors tools for risk assessment, recovery optimization, and strategic portfolio management, particularly within the European market.

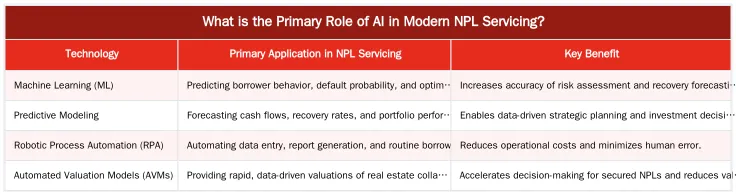

What is the Primary Role of AI in Modern NPL Servicing?

Artificial intelligence in non-performing loan servicing enhances operational efficiency and strategic effectiveness. By processing vast datasets, AI algorithms predict borrower behavior, recommend optimal workout strategies, and automate routine administrative tasks. This moves human servicers from reactive, manual processes to proactive, data-informed decision-making, allowing them to focus on high-value negotiations and complex case management.

Defining AI and Data Analytics in NPL Context

In the NPL context, artificial intelligence refers to systems performing tasks that require human intelligence, like pattern recognition, prediction, and decision-making. Data analytics is the process of inspecting, cleaning, and modeling data to discover useful information and support these decisions. For distressed asset portfolios, often with incomplete or unstructured data, these technologies provide a framework to extract value, identify recovery potential, and mitigate risk across thousands of loans.

Key Technologies Driving Efficiency in NPL Recovery

Key technologies automate processes, generate insights, and improve financial modeling accuracy. From predicting defaults to valuing collateral, technology provides servicers with a granular and forward-looking view of their portfolios.

Machine Learning and Predictive Modeling for Loan Defaults

Machine learning (ML) algorithms are central to NPL management. By analyzing historical loan performance data, borrower information, and macroeconomic indicators, ML-powered predictive modeling identifies patterns signaling a high probability of default or a borrower’s propensity to pay. This enhances credit risk analysis, enabling servicers to segment borrowers and apply tailored communication and workout strategies. Early identification of at-risk loans allows for preemptive action, potentially preventing a loan from becoming non-performing.

RPA and AVMs: Automating Tasks and Valuations

Robotic Process Automation (RPA) handles high-volume, repetitive tasks like data entry, document processing, and standardized communications, freeing skilled personnel for more complex activities. For secured NPLs, Automated Valuation Models (AVMs) use statistical modeling and property databases to provide rapid, cost-effective real estate valuations. This accelerates decision-making for foreclosure or asset disposal by providing up-to-date collateral values.

Implementing AI & Data Analytics for Strategic NPL Portfolio Management

Artificial intelligence and data analytics enable a more sophisticated approach to NPL portfolio management. In the European market, where regulations and economic conditions vary by country, technology provides tools to navigate these challenges. This is relevant for investors and servicers in markets like the Iberian Peninsula, where large NPL portfolios require efficient, scalable management.

Optimizing Workout Strategies with Data-Driven Insights

Data analytics transforms workout strategies from a one-size-fits-all approach to a segmented, personalized process. By analyzing borrower data, AI recommends the most effective action for each loan, such as forbearance, loan modification, or legal proceedings. This data-driven approach informs effective early workout playbooks, maximizing successful resolutions and improving portfolio recovery rates.

Navigating European Regulations with AI-Powered RegTech

The European financial landscape has stringent regulations from bodies like the European Banking Authority (EBA). Regulatory Technology, or RegTech, uses AI to help firms stay compliant. These systems automate compliance monitoring, reporting, and data management, ensuring adherence to rules like GDPR and IFRS 9. By reducing the manual burden of compliance, RegTech minimizes operational risk and helps servicers adapt to regulatory changes.

Navigating the Future: Insights from European NPL & Distressed Debt Forums

DD Talks’ NPL and distressed debt conferences in European hubs like London and Madrid are a platform for industry exchange. Senior executives from institutions such as Blackstone, Goldman Sachs, and Ares Management share experience and strategic insights on integrating technology into their investment and servicing operations.

Expert Perspectives on Technology’s Impact on Deal-Making

Panel discussions and case studies at our events highlight how technology influences deal-making. Investors use advanced analytics for faster, more accurate due diligence on NPL portfolios, identifying previously undetectable value and risks. These discussions show delegates how to leverage AI and analytics for smarter NPL management, transaction sourcing, and execution.

The Role of Loan Servicing Software in a Connected Ecosystem

Loan servicing software platforms are central to this technological shift. These integrated systems are the operational backbone, incorporating AI, ML, and RPA functionalities. The choice of software is a strategic decision impacting operational efficiency, data security, and analytical capabilities. The right platform enables data flow, facilitates automation, and provides reporting tools for managing complex portfolios across multiple jurisdictions.

The Tangible Benefits of AI in NPL Servicing: Enhanced Recovery & Risk Mitigation

Adopting technology in NPL management delivers measurable advantages beyond cost savings, improving how servicers and investors manage risk and maximize returns from distressed assets. Integrating intelligent systems creates a resilient, scalable operational model capable of handling portfolio growth and market volatility.

Quantifiable Improvements in Recovery Rates and Cost Efficiency

By optimizing collection strategies and automating manual work, AI increases recovery rates and lowers operational expenditures. For example, predictive models prioritize accounts with the highest payment likelihood, allocating human resources effectively. According to analysis by firms like McKinsey & Company, financial institutions implementing AI in risk functions see significant improvements in efficiency and effectiveness. This strengthens the bottom line and enhances portfolio performance.

Market Growth of Debt Collection Technology

Increased reliance on these tools is reflected in the expanding debt collection technology market. As servicers and financial institutions seek more sophisticated solutions, demand for AI-powered platforms grows. This market trend shows technology is a core component of a successful NPL servicing strategy. Staying current with these developments, detailed in reports on the debt collection software market, is essential to remain competitive.

Connect with Industry Leaders at Our Next NPL Forum

AI and data analytics are reshaping the NPL and distressed debt landscape. To navigate this evolution, DD Talks’ European conferences provide a venue for servicers, investors, and technology providers to connect, share insights, and forge strategic partnerships.

Join us to learn from the experts driving this transformation and discover the technologies shaping the future of NPL management. To learn more about our upcoming events and secure your place, contact us or Request Agenda for our next NPL & Distressed Debt Forum.

Conclusion

Artificial intelligence and data analytics in non-performing loan servicing have become a practical necessity. These technologies provide tools to enhance efficiency, improve decision-making, and navigate the NPL market. For institutional investors and workout professionals, embracing this technological shift is key to optimizing recovery outcomes and achieving portfolio goals. To stay at the forefront, explore our upcoming forums: contact us or Request Agenda.

Frequently Asked Questions

What is the primary role of ai in npl servicing?

The primary role of ai in npl servicing is to enhance efficiency and effectiveness throughout the recovery lifecycle. By analyzing vast datasets, algorithms can predict borrower behavior, recommend optimal workout strategies, and automate routine tasks. This allows human servicers to focus on complex negotiations and relationship-based resolutions.

How does data analytics improve NPL recovery rates?

Data analytics improves NPL recovery rates by providing servicers with deep, actionable insights into their portfolios. By analyzing historical data, these systems identify patterns, segment borrowers for targeted communication, and forecast the likelihood of success for different workout strategies. This data-driven approach ensures resources are allocated to the most effective recovery paths.

What are the main risks of implementing ai in npl servicing?

The main risks of implementing ai in npl servicing include potential biases in algorithms if trained on unrepresentative data, significant data privacy and security concerns, and high initial implementation costs. Mitigating these risks requires robust governance, continuous model validation, and a strong focus on ethical AI principles to ensure fair outcomes.

What is a practical example of predictive modeling in NPL management?

A key example is using machine learning models to predict the probability of a borrower “self-curing” versus requiring intensive intervention. This allows servicers to prioritize their efforts, focusing workout resources on high-risk accounts while applying automated, lower-cost methods for others. This segmentation significantly improves portfolio management efficiency.

Will intelligent automation completely replace human agents in NPL servicing?

It is unlikely that technology will completely replace human agents in the NPL sector. Artificial intelligence and data analytics are powerful tools that augment human capabilities, handling data processing and automating routine outreach. However, human experts remain essential for managing complex negotiations, building relationships, and making final strategic decisions.

Where can professionals discuss the future of ai in npl servicing?

Professionals can discuss the future of ai in npl servicing at specialized industry events, such as our NPL & Distressed Debt Forums. These conferences bring together institutional investors, servicers, and technology providers to explore market trends and new strategies. You can request an agenda to see the topics and speakers at our next event.

0 Comments