Credit Enhancement Techniques: Optimizing Sub-performing Loan Securitisation

Understanding credit enhancement techniques is crucial for mitigating risk in sub-performing loan securitisations. This article details how these mechanisms improve the credit profile of asset-backed securities (ABS) by creating buffers against potential losses. It explores essential structural methods like overcollateralization and senior-subordinated structures, alongside financial tools such as cash reserve funds. Applying effective credit enhancement techniques is vital for transforming sub-performing loan portfolios into investment-grade assets, thereby attracting institutional investors and securing favorable credit ratings in structured finance markets.

DDTalks provides expert insights into European private credit and structured finance, facilitating high-value deal-making and industry networking. Our content reflects the deep expertise shared at our premier conferences, offering practical guidance on complex financial strategies like securitisation.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

What Are Credit Enhancement Techniques in Securitisation?

Credit enhancement techniques are financial and structural mechanisms in securitisation that improve the credit profile of asset-backed securities (ABS). Their purpose is to mitigate investor loss risk by creating a buffer to absorb shortfalls from the underlying asset pool, increasing the likelihood of timely principal and interest payments.

These methods enable assets with lower intrinsic credit quality to become investment-grade securities. Credit enhancements make ABS more attractive to institutional investors and are essential for achieving desired credit ratings.

The Imperative for Sub-Performing Loans

For portfolios of sub-performing loans (SPLs), robust credit support is critical. SPLs, defined as loans 30 to 90 days past due, exhibit higher and more unpredictable default and loss characteristics than performing assets. Their inconsistent cash flows make it difficult to structure a securitisation that meets the payment requirements of senior-rated securities without significant risk mitigation. Enhancements provide the protection to bridge this credit quality gap, making the securitisation of these assets feasible.

How Do Key Credit Enhancement Mechanisms Work in Practice?

Credit support mechanisms in structured finance are either structural or financial. A securitisation often layers multiple methods to create a structure capable of withstanding economic stress scenarios.

Structural Enhancements: Overcollateralization and Senior-Subordination

Structural enhancements are built into the legal framework of the securitisation. Common forms are overcollateralization and subordination.

- Overcollateralization (OC): This involves pledging a pool of assets with a principal value greater than the total face value of the securities issued. For example, a special purpose vehicle (SPV) might issue €100 million in bonds backed by a pool of sub-performing loans with a nominal value of €115 million. This €15 million in excess collateral provides a 15% buffer to absorb initial losses before they affect the bondholders.

- Senior-Subordinated Structure (Credit Tranching): This method creates multiple classes, or tranches, of securities with different payment priorities. In a cash flow waterfall, senior tranches receive principal and interest payments first. Losses from the underlying asset pool are allocated first to the most junior (equity) tranche, then the mezzanine tranches, and finally to the senior tranches. This sequential loss absorption protects the higher-rated securities.

Financial Enhancements: Excess Spread and Reserve Funds

Financial enhancements involve setting aside cash flows or funds to cover potential losses.

- Excess Spread: This is the net interest margin remaining after paying interest to bondholders and covering servicing fees. If the underlying loans generate an average interest of 8% and the issued bonds pay an average coupon of 5%, the 3% difference (less fees) is the excess spread. This surplus cash flow can cover losses or be trapped in a reserve account to build credit support.

- Cash Reserve Fund: This account is funded at closing, typically with a portion of the issuance proceeds. It serves as a source of liquidity to cover temporary payment shortfalls to investors. If losses exceed the available excess spread, the reserve fund can be drawn upon to ensure the senior notes remain current.

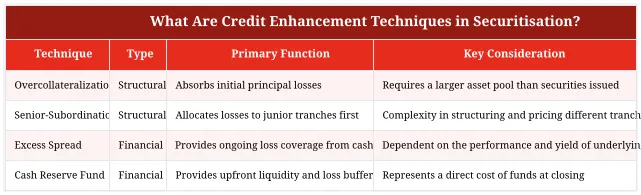

View data as table

| Technique | Type | Primary Function | Key Consideration |

|---|---|---|---|

| Overcollateralization | Structural | Absorbs initial principal losses | Requires a larger asset pool than securities issued |

| Senior-Subordination | Structural | Allocates losses to junior tranches first | Complexity in structuring and pricing different tranches |

| Excess Spread | Financial | Provides ongoing loss coverage from cash flow | Dependent on the performance and yield of underlying assets |

| Cash Reserve Fund | Financial | Provides upfront liquidity and loss buffer | Represents a direct cost of funds at closing |

Evaluating Credit Enhancement: The Role of Rating Agencies and Investor Confidence

The success of a securitisation, particularly one backed by sub-performing assets, depends on earning the confidence of institutional investors. Credit rating agencies are pivotal, providing an independent assessment of the credit risk for each tranche. Their analysis focuses on the adequacy and resilience of the credit enhancement structure.

Rating Agency Methodologies and Criteria

Rating agencies like S&P Global, Moody’s, and Fitch Ratings use quantitative models and qualitative analysis to evaluate securitisations. The process involves stress-testing the transaction’s cash flows under adverse scenarios. For an SPL portfolio, this includes modeling higher default rates, lower recovery rates, and payment delays. The agency determines the level of credit enhancement required for a tranche to achieve a specific rating (e.g., AAA, AA, A). A tranche must withstand these stresses and still make timely payments to receive a high rating. For more information, review S&P Global’s general principles on credit ratings.

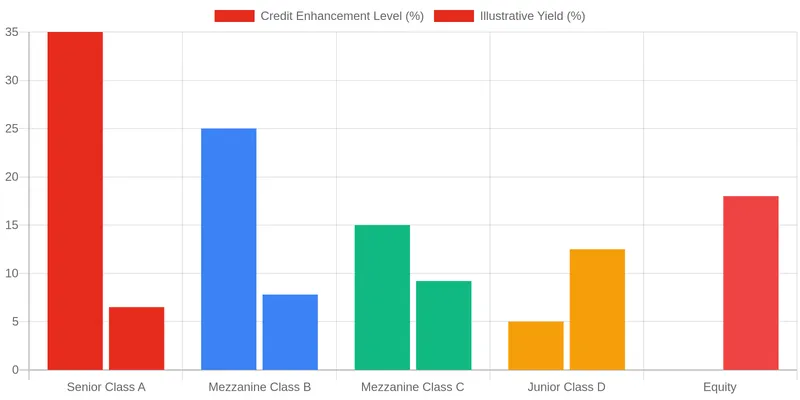

View data as table

| Tranche | Credit Enhancement Level (%) | Target Rating | Illustrative Yield (%) |

|---|---|---|---|

| Senior Class A | 35.0% | AAA | 6.5% |

| Mezzanine Class B | 25.0% | AA | 7.8% |

| Mezzanine Class C | 15.0% | A | 9.2% |

| Junior Class D | 5.0% | BBB | 12.5% |

| Equity | 0.0% | Not Rated | 18.0%+ |

Building Trust: Enhancements as a Cornerstone of Marketability

A transparent credit enhancement package is key to a marketable security. It gives investors a clear understanding of the protections in place and the conditions for potential losses. This clarity is essential for pricing risk and making informed investment decisions. In the European market, where forums like those hosted by DDTalks often center on risk-adjusted returns, a robust enhancement structure allows issuers to access a broader pool of capital at more favorable funding costs. It transforms a high-risk asset pool into investable products for different risk appetites.

Optimizing Securitisation: Strategic Implications for European Private Credit

Credit enhancement is strategic for originators and the European private credit and distressed debt markets. These mechanisms enable capital recycling, balance sheet management, and new investment opportunities from complex asset pools.

Unlocking Liquidity and Capital Relief for Originators

For banks, NPL servicers, and other financial institutions, securitisation helps manage their balance sheets. By packaging and selling sub-performing loans via true sale securitisation structures, originators transfer credit risk to capital markets investors. This process generates liquidity, reduces regulatory capital requirements, and frees up capacity for new lending or investment. Credit enhancement makes this risk transfer possible at an economically viable cost, a key goal for those seeking to unlock liquidity and capital relief through securitisation.

Investment Opportunities in Enhanced Sub-Performing Loan Portfolios

For institutional investors like pension funds, insurance companies, and private credit funds, securitised SPLs offer access to higher-yielding assets. The credit tranching enabled by enhancement structures lets investors select a risk-return profile fitting their mandate. A conservative investor might purchase the highly-rated senior tranche for its protection and stable return. A specialized distressed debt fund might invest in the junior or equity tranches for potentially higher returns. This risk segmentation is crucial for market function, a key theme for professionals mastering non-performing loans and related asset classes.

The Future of Credit Enhancement in European Structured Finance

The European structured finance landscape is evolving due to regulatory shifts, technological advancements, and market dynamics. Credit enhancement techniques for complex assets like sub-performing loans are adapting. As of 2026, key trends are influencing risk mitigation in this sector.

Adapting to Evolving Regulatory Landscapes

European regulations, including the Securitisation Regulation and frameworks like Basel IV, emphasize transparency, risk retention, and asset quality. These rules influence how credit enhancements are structured and sized. Scrutiny on the alignment of interests between originators and investors often leads to greater risk retention by the originator, which acts as a form of credit support. Future adjustments to frameworks like AIFMD II could further impact how alternative investment funds engage with and structure these securities.

Innovation in Risk Mitigation for Complex Assets

Integrating data analytics and machine learning allows for more dynamic, data-driven approaches to credit enhancement. Advanced models can predict default and recovery more accurately for granular loan portfolios, allowing more precise calibration of overcollateralization or reserve fund levels. New structures are emerging that blend traditional methods with features like performance-based triggers, which can adjust credit support over a transaction’s life based on the SPL portfolio’s performance. These innovations make the securitisation of complex assets more efficient and resilient.

Advance Your Expertise at Premier European Structured Finance Events

Understanding sub-performing loan securitisation and credit enhancement requires deep knowledge and industry connections. Our B2B financial conferences in European hubs like London and Madrid provide a platform to engage with leading dealmakers, investors, and advisors.

Attendees participate in data-driven panels on structuring trends, network with GPs and LPs, and uncover opportunities in the private credit and distressed debt markets. To learn more about our upcoming events, Request Agenda or contact us.

Conclusion

The effectiveness of credit enhancement in a sub-performing loan securitisation determines its success. Investors must decide if the layered protections are sufficient to withstand plausible economic stress. Originators must structure these enhancements efficiently to achieve desired capital relief and funding costs. As the European market for distressed and sub-performing assets matures, sophisticated risk mitigation will remain critical for unlocking value and maintaining market liquidity. Engagement with industry experts is essential to stay ahead of these developments. Request Agenda for our next event or contact us to explore partnership opportunities.

Frequently Asked Questions

What level of subordination is typically required for a senior tranche of sub-performing loans to achieve an investment-grade rating?

Achieving an investment-grade rating, such as BBB or higher from agencies like Fitch or S&P Global, for a senior tranche backed by sub-performing loans often requires significant subordination, frequently ranging from 30% to 50% of the total capital structure. This level is substantially higher than for performing loan securitisations due to the increased expected losses and cash flow volatility. The exact percentage is determined by rating agency models that stress test the underlying collateral’s recovery rates and timing.

How does overcollateralization in a Spanish NPL securitisation differ from that in a performing loan ABS?

In a typical Spanish Non-Performing Loan (NPL) securitisation, the required overcollateralization (OC) can exceed 10-15%, meaning the asset pool’s value is significantly higher than the notes issued. This contrasts sharply with performing loan asset-backed securities (ABS), where OC might be as low as 2-5%. This higher buffer for NPLs is crucial to absorb potential losses from uncertain recovery amounts and timing, a key risk factor analyzed by institutions like DBRS Morningstar in their European NPL ratings.

What specific triggers can divert excess spread into a reserve account in an SPL transaction?

In sub-performing loan transactions, excess spread is often controlled by performance-based triggers that, if breached, divert cash flow to build credit support. Common triggers include a cumulative default rate exceeding a predefined threshold (e.g., 15%) or a delinquency rate for a specific bucket (e.g., 60+ days) rising above a certain level. Once activated, these mechanisms “trap” cash that would otherwise flow to junior noteholders, redirecting it to a reserve fund or to accelerate principal payments on senior notes.

Are third-party guarantees a common form of credit enhancement for recent European distressed debt securitisations?

While third-party guarantees from monoline insurers were prevalent before the 2008 financial crisis, they are now rare in European distressed debt and NPL securitisations. The market overwhelmingly relies on internal credit enhancement techniques like subordination, overcollateralization, and excess spread. This structural self-reliance is preferred by investors and rating agencies, who now place greater emphasis on the intrinsic quality and structure of the deal itself rather than on an external financial guarantee.

How is the quality of the loan servicer considered a form of credit enhancement?

The quality and track record of the special servicer is a critical, albeit qualitative, form of credit enhancement in any NPL or SPL deal. A highly reputable servicer with a proven workout strategy for a specific asset class, such as those discussed at DD Talks’ NPL & Distressed Debt Forums, can significantly increase expected recoveries. Rating agencies explicitly factor servicer quality and historical performance data into their analysis, as an effective servicer directly mitigates losses and improves the cash flow available to the securitisation trust.

0 Comments