European ABS and Securitisation: Driving Capital Markets Growth

The european abs and securitisation market is experiencing a significant revival, driven by regulatory clarity, evolving bank strategies, and robust investor demand. This resurgence encompasses traditional asset-backed securities and expands into NPL securitisation and private credit structures. Readers will understand the key drivers, including the STS Regulation, its role in credit risk transfer, and how structured finance facilitates capital optimization for banks and provides yield for institutional investors. The article explores the benefits and future outlook for this dynamic market segment.

DDTalks specializes in organizing premium B2B financial conferences, connecting industry leaders in European private credit, NPLs, and structured finance. Our events facilitate high-value deal-making and provide expert insights into market trends and regulatory developments.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

The market for european abs and securitisation is reviving, driven by regulatory clarity, evolving bank strategies, and investor appetite for structured credit. This resurgence moves beyond traditional asset classes, embracing non-performing loan (NPL) transfers and the expanding private credit sector.

What’s Driving the Revival of European ABS and Securitisation?

The revival of Europe’s securitisation market is driven by regulatory certainty from the STS framework, banks’ need for capital relief and risk transfer, and institutional investors’ search for yield. The expansion of non-bank lending, particularly in private credit, has introduced new asset pools for structured finance transactions.

Defining European Asset-Backed Securities and Structured Finance

Securitisation is a structured finance process where an originator pools financial assets and transfers them to a special purpose vehicle (SPV). This SPV issues tradable, interest-bearing securities, known as asset-backed securities (ABS), to investors. Cash flows from the underlying asset pool are used to make principal and interest payments to investors.

In Europe, underlying assets range from residential mortgages (RMBS) and auto loans to credit card receivables, non-performing loans (NPLs), and direct lending portfolios. The process transforms illiquid assets into liquid capital market instruments.

Key Factors Fueling the Market’s Resurgence in 2026

- Regulatory Clarity: The Simple, Transparent and Standardised (STS) Regulation provides a quality label that enhances investor confidence.

- Bank Capital Optimization: Banks use securitisation for credit risk transfer and managing regulatory capital requirements under Basel III and IV, freeing up balance sheet capacity for new lending.

- Investor Demand for Yield: Institutional investors seek the risk-adjusted returns offered by ABS tranches, diversifying from traditional fixed-income assets.

- Growth of Private Credit: The expansion of direct lending has created a new source of assets for securitisation, allowing private credit funds to access capital markets and manage portfolio liquidity.

Unpacking Key Structures: NPL, Synthetic, and Private Securitisation

While traditional securitisations of performing loans remain common, innovation and volume growth come from specialized structures that address bank balance sheet challenges and create financing avenues for non-bank lenders.

NPL Securitisation: De-risking Balance Sheets Across Europe

Non-performing loan securitisation helps banks, particularly in Southern Europe, manage asset quality. In an NPL securitisation, a bank transfers a portfolio of defaulted or sub-performing loans to an SPV, which issues notes to distressed debt investors.

This process removes NPLs from the bank’s balance sheet, improving its regulatory capital position and risk profile. For investors and servicers, these transactions offer returns through workout and recovery strategies. The mechanics of these deals are a topic at industry forums offering in-depth panels on NPL and distressed debt.

The Rise of Private Securitisation and Direct Lending Synergy

Private credit and securitisation are converging. Direct lending funds use private securitisation, or collateralized loan obligations (CLOs), as a financing tool. These are often privately placed with institutional investors.

This provides direct lenders with long-term, matched funding and lets them recycle capital into new loans. For investors, it provides access to diversified portfolios of private corporate credit through rated, tradable securities. This market segment’s growth reflects the institutionalization of private credit, as detailed by S&P Global Market Intelligence.

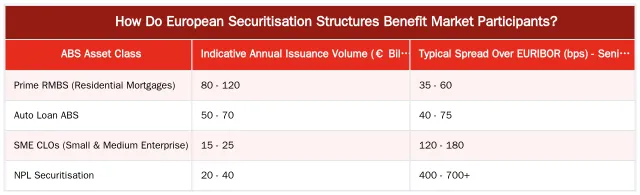

How Do European Securitisation Structures Benefit Market Participants?

Securitisation connects originators seeking capital and funding efficiency with investors seeking tailored risk-return profiles, improving the liquidity of European credit markets.

Capital Relief and Efficient Risk Transfer for Originators

For banks and lenders, securitisation optimizes the balance sheet. Transferring an asset pool’s credit risk to investors reduces an originator’s risk-weighted assets (RWAs). This lowers the regulatory capital requirement, freeing up capital for new lending or shareholder returns.

Securitisation is also a funding source. It gives originators access to institutional capital, reducing reliance on traditional funding like deposits or corporate bonds. This funding diversification enhances financial stability and lending capacity.

Yield Enhancement and Diversification for Institutional Investors

For institutional investors, European ABS offers portfolio diversification. The securities provide exposure to asset classes and credit profiles not otherwise accessible.

The structured nature of ABS, with different risk tranches, lets investors target their desired risk-return profile. Credit enhancement mechanisms provide downside protection, and yields are often higher than on similarly rated corporate bonds.

Expert Perspectives on the Future of European Structured Finance

The european abs and securitisation market is shaped by innovation, macroeconomic conditions, and investor priorities. Insights from industry conferences indicate several key developments.

Key Trends Shaping the European Securitisation Market in 2026

- ESG Integration: Demand is growing for securitisations backed by green assets, like electric vehicle loans or energy-efficient mortgages. Clear standards for “green securitisation” will catalyze growth.

- Technological Advancement: Blockchain and data analytics improve transparency and efficiency in servicing and reporting, making the asset class more accessible and reducing operational risks.

- Expansion of Asset Classes: Securitisation will be applied to new asset classes, including intellectual property rights, fund subscription lines, and other non-traditional revenue streams.

Financial news outlets like Bloomberg’s structured finance section cover these dynamics.

Insights from Leading European Structured Finance Conferences

DDTalks events connect the structured finance community for deal-making and strategic discussions. Panels and workshops cover challenges and opportunities in structuring NPL deals, financing direct lending portfolios, and navigating the regulatory environment.

Attendees learn from the institutions originating, structuring, and investing in these securities. Understanding the European private credit and direct lending landscape is essential for operating in the securitisation market.

Connect with European Securitisation Leaders at DDTalks Events

Europe’s structured finance markets offer opportunities for deal origination, capital deployment, and strategic partnerships. DDTalks’ conferences in London and Madrid bring together influential players in private credit, NPLs, and structured finance.

Engage with leading GPs, LPs, investment bankers, and legal advisors. To learn more, contact us or Request Agenda for our next summit.

Conclusion

The European securitisation market is a vital component of the continent’s capital markets. Supported by a regulatory framework and the needs of banks and investors, its growth is accelerated by NPL and private credit innovation. To explore these developments, contact us or Request Agenda for our next event.

Frequently Asked Questions

What key factors are driving the revival of European securitisation?

The revival is driven by key factors like increased regulatory clarity from the Simple, Transparent and Standardised (STS) framework and banks’ strategic need for capital relief. Additionally, persistent investor demand for yield and the growth of private credit have introduced new, diverse asset classes suitable for structured finance transactions.

How does private securitisation differ from public ABS deals?

Private securitisation involves structuring and placing securities directly with a select group of institutional investors, bypassing a public offering. This approach allows for greater customisation and confidentiality compared to public ABS deals. While these private transactions offer less liquidity, they provide tailored solutions for both originators and sophisticated investors.

What are the primary benefits of european abs and securitisation for market participants?

For originators like banks and non-bank lenders, the primary benefit of european abs and securitisation is efficient risk transfer and access to alternative funding sources, which provides valuable capital relief. For institutional investors, these structures offer access to diversified, often higher-yielding credit assets that may not be available in public markets.

What is a Simple, Transparent and Standardised (STS) securitisation?

An STS securitisation is a deal that meets specific criteria for quality and transparency under a European Union regulatory framework. This designation is designed to build confidence in the market by ensuring structures are straightforward and easy to understand. By achieving the STS label, transactions receive preferential regulatory capital treatment, making them more attractive to both banks and investors.

Are Non-Performing Loans (NPLs) a significant part of the European structured finance revival?

Yes, Non-Performing Loans (NPLs) are a cornerstone of the revival in European structured finance, especially in Southern Europe. Government-backed guarantee schemes have been instrumental in making these complex asset-backed securities viable for a wider investor base. The successful structuring of NPL deals has helped banks clean up their balance sheets and recycle capital.

How can I connect with leaders shaping the future of European ABS and securitisation?

DDTalks provides a premier platform for connecting with the leaders driving the market forward. Our specialised conferences in key European financial hubs like London and Madrid gather originators, arrangers, and investors to discuss critical trends in European ABS and securitisation. You can network with key decision-makers and gain insights by requesting the agenda for our next event.

0 Comments