Impact of AIFMD II: Reshaping European Fund Structuring

The impact of AIFMD II will significantly reshape European alternative investment funds, introducing a harmonized regulatory framework across the EU. This directive amends rules for fund structuring, operational compliance, and investment strategies, particularly affecting private credit. Fund managers must understand the implications for loan origination funds, enhanced delegation rules, and new reporting requirements to ensure compliance by 2026. The directive aims to bolster investor protection and financial stability through mandatory liquidity management tools and stricter substance requirements.

DDTalks provides expert insights into these complex regulatory shifts, drawing on extensive experience hosting premium B2B financial conferences. Our events facilitate high-level discussions among industry leaders on European private credit, NPLs, and structured finance, ensuring practical understanding of regulatory changes.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

The impact of aifmd ii will reshape alternative investment funds with a harmonized, stringent regulatory framework across the European Union. This directive, an evolution of the original Alternative Investment Fund Managers Directive, amends rules affecting fund structuring, operational compliance, and investment strategies. Fund managers, particularly in private credit, must understand these changes to delegation, reporting, and loan origination for compliant operations in 2026 and beyond.

What Are the Key Changes Introduced by AIFMD II?

AIFMD II amends the existing framework to enhance investor protection, integrate sustainable finance considerations, and ensure financial stability. Key changes include harmonized rules for loan-originating funds, stricter delegation and substance requirements, enhanced data reporting, and a mandatory framework for liquidity management tools to handle market stress.

AIFMs must select and implement at least two liquidity management tools (LMTs) from a harmonized list, such as redemption gates or notice periods, to manage investor redemptions during market volatility. The directive also clarifies the scope of ancillary services AIFMs can provide and strengthens supervisory data through more detailed reporting obligations. These updates reflect lessons from the original directive’s implementation and align with financial market trends, as detailed in ESMA guidelines and legislative proposals.

How Does AIFMD II Impact Loan Origination Funds?

AIFMD II introduces a harmonized framework for loan origination funds. Previously governed by disparate national regulations, these funds now face unified EU rules to manage their specific risks, formalizing the regulatory approach to the private credit market.

Loan-originating AIFs must implement policies for granting credit, assessing credit risk, and administering loan portfolios. A key requirement is the prohibition on originating loans to financial undertakings. The directive also introduces a risk retention rule, requiring funds to retain 5% of the notional value of loans they originate and sell on the secondary market. This “skin-in-the-game” provision aligns fund manager and investor interests and promotes prudent lending.

New Rules for Leverage and Risk Diversification

To mitigate systemic risk, AIFMD II establishes leverage limits for loan-originating funds. These limits differ for open-ended and closed-ended funds, reflecting their liquidity profiles. Open-ended funds face stricter leverage caps. The directive also imposes a diversification requirement, limiting a fund’s exposure to a single borrower to 20% of its capital if the borrower is a financial undertaking, an AIF, or a UCITS.

Strategic Implications for European Fund Structuring

AIFMD II has strategic implications for how managers structure and market funds in Europe. The choice of fund domicile, vehicle, and operational setup requires careful consideration for compliance. The harmonization of loan origination rules, for example, may make certain jurisdictions more attractive for private credit strategies.

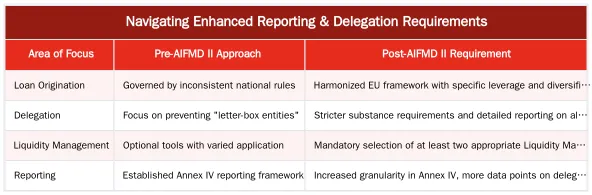

Managers must reassess existing structures for new requirements in depositary functions, delegation, and liquidity management. Enhanced reporting and substance rules may lead firms to bring more functions in-house or re-evaluate third-party provider relationships.

Adapting Fund Structures for AIFMD II Compliance

The updated directive will influence the choice between fund vehicles. While AIFMD II applies broadly, managers may also consider structures like the revised ELTIF 2.0 framework, which offers benefits such as a retail-focused marketing passport but has its own investment rules. The decision will depend on the fund’s strategy, target investor base, and geographic focus. The table below outlines fund structuring requirements.

DDTalks’ Insight: The Future of Private Credit Under AIFMD II

As organizers of Europe’s premier private credit and distressed debt conferences, we see the impact of aifmd ii as a key regulatory change for the industry. The formalization of rules for loan-originating funds provides clarity, creates a level playing field, and can bolster investor confidence. It also introduces operational complexities that managers must address.

Heightened substance and reporting requirements will likely favor larger managers with sophisticated compliance infrastructure. Others will need to review their operational models and partnerships. These regulatory shifts are a central theme at our events, where leading GPs, LPs, and legal advisors discuss market trends and regulatory changes. Understanding these dynamics affects deal-making and fundraising. For more context, explore our guide on European Private Credit Fund Structures.

Preparing for AIFMD II: Conference Insights and Networking

Preparing for these changes involves direct engagement with peers and experts. DDTalks forums in London, Madrid, and across Europe provide a platform for these conversations. Our agendas address regulatory and market challenges, offering insights from institutions like Blackstone, Ares Management, and Goldman Sachs. Networking at these events allows managers to share best practices and build professional relationships.

Secure Your Place at Europe’s Leading Private Credit Forums

Navigating AIFMD II requires strategic insight and peer-to-peer knowledge sharing. At DDTalks events, you gain direct access to industry leaders, regulators, and legal experts in European private credit. Engage in discussions, build connections, and clarify how to adapt your fund structures.

Explore our upcoming events and secure your delegate pass. Request Agenda for sessions addressing the challenges and opportunities of AIFMD II. For more information, contact us.

Conclusion

AIFMD II is a key regulatory change for European alternative investment funds, requiring strategic adaptation from fund managers. Understanding its rules for loan origination, delegation, and reporting is necessary for compliant fund structuring. The directive emphasizes transparency and risk management. To gain insights and navigate this landscape, engage with industry leaders at DDTalks conferences. Request Agenda for our next event or contact us to learn more.

Frequently Asked Questions

What is the single most significant impact of AIFMD II on direct lending funds?

AIFMD II introduces specific, harmonized rules for loan-originating funds, including requirements for leverage, risk diversification, and preventing conflicts of interest. The impact of aifmd ii is that it formalizes the regulatory approach to this key private credit segment, requiring these European fund structures to operate with greater risk management scrutiny.

How do the new delegation rules in AIFMD II affect fund managers?

The updated directive strengthens the oversight of delegation arrangements, requiring managers to provide more detailed justifications and reporting to national regulators. This change ensures that sufficient substance and decision-making functions remain within the EU-based AIFM, preventing the creation of ‘letter-box’ entities and increasing accountability.

What is the impact of AIFMD II on reporting and pre-marketing activities?

The directive enhances the existing Annex IV reporting framework, demanding more granular data on portfolios, risk exposures, and delegation arrangements. For pre-marketing, the rules are clarified and tightened to create a more standardized process. The overall impact of AIFMD II is to increase transparency for regulators and create a more uniform approach to fund distribution.

How does AIFMD II address liquidity management for open-ended funds?

The directive mandates that Alternative Investment Fund Managers (AIFMs) managing open-ended funds must select and implement at least two appropriate liquidity management tools (LMTs) from a harmonized list. This ensures managers are better prepared to handle redemption pressures without resorting to fire sales of assets, thereby promoting greater financial stability.

What is the expected timeline for the impact of AIFMD II to be fully felt?

EU member states are required to transpose the AIFMD II directive into their national laws, with most provisions set to apply from early 2026. Fund managers should begin preparing now for these changes. The full impact of AIFMD II will become clearer as national competent authorities implement the rules and market practices adapt accordingly.

How can our firm learn more about navigating these regulatory changes?

Understanding these complex regulatory shifts is crucial for strategic planning in the private credit and alternative investment space. Our conferences feature expert-led panels dedicated to dissecting the practical implications for fund structuring and deal-making. You can explore these topics in depth by visiting our website to request the agenda for our upcoming European private credit forums.

0 Comments