Tax and Legal Considerations for Gps: Optimizing European Direct Lending Structures

Navigating the tax and legal considerations for GPs in European direct lending is crucial for optimizing fund performance and ensuring compliance. General Partners must address complex issues like permanent establishment risk, withholding taxes on interest payments, and the varied treatment of carried interest. Effective fund structuring, including strategic fund domicile and robust substance requirements, is essential to mitigate tax leakage. Compliance with EU directives such as ATAD and DAC6, alongside careful transfer pricing strategies, helps manage regulatory challenges and preserve investor returns in the evolving European market.

DDTalks provides authoritative insights into European private credit and direct lending markets. This analysis reflects the deep expertise required to navigate complex financial regulations and optimize investment strategies for institutional investors and General Partners operating across Europe.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

The European direct lending market offers opportunities, but navigating its tax and legal considerations for gps is critical. This guide analyzes the tax and regulatory challenges General Partners face, from permanent establishment risk and withholding taxes to fund domicile and carried interest. It explores strategies to optimize fund structures, ensure compliance with EU directives like ATAD and DAC6, and mitigate risks in 2026 and beyond for institutional investors.

What are the Key Tax and Legal Considerations for European GPs?

For General Partners in European direct lending, primary tax and legal issues involve mitigating tax leakage and ensuring regulatory compliance across jurisdictions. A significant risk is creating a Permanent Establishment (PE), where a fund’s activities in a country trigger local corporate taxation on its profits, even if the fund is domiciled elsewhere. This can arise from on-the-ground deal sourcing, portfolio management, or other key functions.

GPs must also manage withholding taxes on interest payments from borrowers, which can erode investor returns. The tax treatment of carried interest for the management team varies between countries, impacting profitability. The choice of fund domicile and demonstrating sufficient operational substance are critical for accessing treaty benefits and complying with anti-avoidance rules. These issues are foundational to a tax strategy for a European direct lending fund.

Navigating Permanent Establishment Risk and Withholding Taxes in Europe

Proactive management of PE risk and withholding tax is fundamental for GPs investing in Europe. Failure can lead to unexpected tax liabilities, double taxation, and administrative burdens. Understanding triggers and implementing mitigation strategies is a critical component of value preservation for limited partners (LPs).

Understanding PE Triggers and Consequences for Direct Lending Funds

A Permanent Establishment can be created by a fixed place of business (e.g., an office) or a dependent agent who habitually concludes contracts for the fund. For direct lending funds, PE risk is increased by the presence of investment professionals involved in deal origination, negotiation, and ongoing portfolio management. If a tax authority determines a PE exists, a portion of the fund’s profits attributable to it will be subject to local corporate income tax.

To mitigate this, GPs must structure their operations to ensure decision-making authority resides in the correct entity and location. Establishing substance in the fund’s domicile—with qualified personnel, physical offices, and documented board-level decisions—is essential to defend against PE challenges from other European tax authorities.

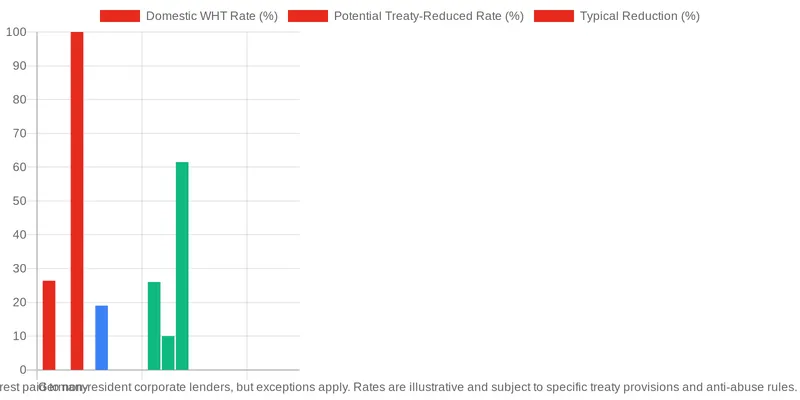

Mitigating Withholding Tax Leakage on European Investments

Withholding tax (WHT) on interest income is a source of tax leakage. Rates vary across Europe, and while many jurisdictions offer exemptions, the requirements are complex. The main tool for reducing WHT is the network of double tax treaties, which can lower or eliminate the tax for qualifying investors. Accessing treaty benefits requires the fund to meet criteria, including being the beneficial owner of the income and having sufficient substance in its domicile country.

Structuring investments through holding companies or financing vehicles in favorable treaty jurisdictions is a common strategy. The table below illustrates how treaty benefits can reduce tax leakage on interest payments.

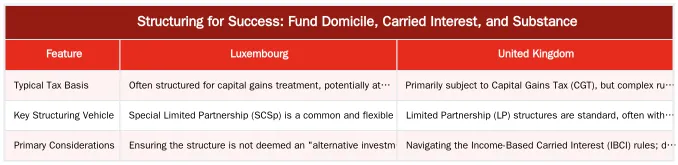

Structuring for Success: Fund Domicile, Carried Interest, and Substance

Fund structuring is key to tax efficiency in European direct lending. Choices regarding fund domicile, carried interest management, and operational substance impact net returns for both LPs and the GP.

Optimizing Fund Domicile and Substance Requirements for European Funds

Fund domicile selection is driven by the legal and regulatory framework, tax neutrality, and investor base. Jurisdictions like Luxembourg and Ireland are popular for their stable political environments, treaty networks, and fund regimes like the AIFMD framework. Our guide on European Private Credit Fund Structures explores these options.

Choosing a domicile is not enough. Tax authorities, guided by EU directives and OECD principles, scrutinize “letterbox” entities. Demonstrating economic substance is required. This involves having local directors with relevant expertise, physical office space, local employees, and making and documenting key management and commercial decisions within that jurisdiction. Failure to establish substance can result in denied treaty benefits and exposure to tax in higher-tax jurisdictions.

Carried Interest Taxation Across Key European Jurisdictions

The taxation of carried interest—the GP’s share of fund profits—is a sensitive area. Treatment varies, influencing how GP entities and executive compensation plans are structured. The goal is to achieve capital gains treatment, which is taxed at a lower rate than ordinary income. Jurisdictions like Luxembourg offer partnership structures that can facilitate this, provided conditions are met. In the UK, capital gains treatment is possible, but the “Income-Based Carried Interest” rules are complex and risk recharacterization as trading income.

The Impact of ATAD, DAC6, and Transfer Pricing on Direct Lending Funds

The European regulatory landscape is evolving to increase tax transparency and combat tax avoidance. EU directives like the Anti-Tax Avoidance Directive (ATAD) and the Directive on Administrative Cooperation (DAC6) have operational consequences for direct lending funds. These rules, discussed at DDTalks events, require GPs to be diligent in their structuring and reporting.

Understanding ATAD and its Anti-Avoidance Rules for Funds

ATAD introduced minimum standards for corporate tax rules across the EU to counter tax avoidance strategies. For direct lending funds, relevant provisions include:

- Interest Limitation Rules: These rules cap the amount of net interest expense a company can deduct in a tax period, typically at a percentage of its EBITDA. This can impact leveraged fund structures and the tax efficiency of intra-group financing.

- General Anti-Abuse Rule (GAAR): This allows tax authorities to disregard arrangements that are not “genuine” and have been put in place for the main purpose of obtaining a tax advantage.

- Hybrid Mismatch Rules: These neutralize the tax effects of arrangements that exploit differences in the tax treatment of an entity or instrument between two jurisdictions.

GPs must analyze their fund and holding structures for compliance with these rules, as detailed by bodies like the European Commission.

DAC6 Reporting Obligations and Transfer Pricing Considerations

DAC6 imposes mandatory reporting on intermediaries (and sometimes taxpayers) for cross-border arrangements with “hallmarks” of potential tax avoidance. Standard fund structuring techniques, like using holding companies in low-tax jurisdictions or certain financing arrangements, can trigger a reporting obligation. GPs need processes to identify and report these arrangements to tax authorities, a topic covered by experts from firms like PwC.

Transfer pricing rules are a critical focus. All intra-group transactions, especially loans between fund entities, must be on an “arm’s length” basis, meaning terms are comparable to what unrelated parties would agree to. Transfer pricing documentation is essential to defend these transactions against challenges from tax authorities.

Proactive Compliance and Strategic Planning for GPs in 2026

In a changing regulatory environment, a “set it and forget it” approach to fund structuring is not viable. Proactive compliance and strategic planning are essential to mitigate risk and capitalize on opportunities. This requires internal processes and engagement with industry experts to stay ahead of legislative changes.

Best Practices for Ongoing Tax Compliance and Risk Mitigation

Maintaining compliance requires a systematic approach. GPs should implement a framework with key practices:

- Regular Tax Health Checks: Periodically review the fund structure and operations to ensure they remain compliant with the latest tax laws in all relevant jurisdictions.

- Substance Monitoring: Continuously document and verify that the fund’s domicile and key entities meet evolving substance requirements. This includes board minutes, employee records, and office leases.

- Documentation Management: Maintain meticulous records for transfer pricing, DAC6 reporting, and decisions supporting the commercial rationale of the fund’s structure.

- Investor Due Diligence: Ensure robust Know Your Customer (KYC) and tax transparency reporting (e.g., FATCA/CRS) processes are in place for all LPs.

These steps build a defensible position, as detailed in our European regulatory guide for direct lending funds.

The Value of Expert Networks and Industry Events for Regulatory Foresight

The complex European tax and legal framework means firms cannot operate in a vacuum. Engaging with a network of legal counsel, tax advisors, and peers is critical for foresight into regulatory shifts. Specialized industry events provide value.

Forums like DDTalks’ private credit conferences gather professionals who shape and interpret these regulations. Panels and workshops on topics like the impact of AIFMD II or cross-border tax planning provide GPs with access to expert analysis and case studies. This environment allows fund managers to test strategies, understand best practices, and build relationships to navigate future challenges.

Stay Ahead: Join Europe’s Leading Private Credit Discussions

Navigating the tax and regulatory landscape of European direct lending requires continuous learning and networking. The challenges of permanent establishment, withholding tax, and EU directives are best addressed with insights from industry experts.

DDTalks brings together GPs, LPs, legal advisors, and institutional investors to discuss these issues. Join our community to gain the foresight to optimize your fund structures and protect returns. To learn about our upcoming events in London, Madrid, and across Europe, Request Agenda or contact us.

Frequently Asked Questions

What is the most significant tax risk for a General Partner (GP) in European direct lending?

The primary risk is inadvertently creating a ‘permanent establishment’ (PE) in a high-tax jurisdiction where the fund is not domiciled. If a GP’s core activities, like deal sourcing or management, are deemed to create a PE in a country like Germany or France, the fund’s profits could face local corporate taxes. This issue is a central component of the tax and legal considerations for gps operating across multiple European markets.

How does a fund’s domicile choice impact its tax and regulatory profile?

The choice of fund domicile, such as Luxembourg or Ireland, is critical for tax efficiency and regulatory compliance. These jurisdictions offer tax-neutral fund vehicles and possess extensive double tax treaties, which are essential for minimizing withholding taxes on interest payments from portfolio companies. A well-chosen domicile simplifies cross-border investment and aligns with investor expectations.

What is ‘carried interest’ and how is its taxation handled in Europe?

Carried interest is the GP’s share of the fund’s profits, typically 20% above a specified hurdle rate. Its tax treatment varies significantly by country; some jurisdictions tax it as a lower-rate capital gain, while others treat it as higher-rate income. This variability makes the GP’s own location a key factor in their overall tax and legal planning.

How do the EU’s Anti-Tax Avoidance Directives (ATAD) affect direct lending funds?

ATAD is a set of EU directives designed to combat corporate tax avoidance, directly impacting fund structures. For GPs, key provisions include interest limitation rules that can restrict a portfolio company’s ability to deduct interest payments on loans. The directives also target hybrid mismatches, requiring careful structuring of financial instruments to remain compliant.

Why is ‘economic substance’ a critical legal issue for a fund’s holding companies?

Tax authorities increasingly scrutinize holding companies to confirm they have genuine economic substance, such as dedicated offices, employees, and independent management. A lack of demonstrable substance can lead to the denial of treaty benefits, like reduced withholding taxes, and may result in significant penalties. Maintaining proper substance is a cornerstone of sound regulatory and tax strategy for general partners.

How can GPs stay updated on the latest tax and legal considerations for direct lending in Europe?

Staying current requires continuous engagement with industry experts and regulatory updates like AIFMD II. Attending specialized forums, such as those focused on European private credit, provides direct access to high-level discussions on market practices and compliance challenges. You can explore the key topics and expert speakers by requesting the agenda for our upcoming conference.

0 Comments