Corporate Loan Underwriting: Mastering European Mid-market Debt

To underwrite corporate loan in the European mid-market, lenders must employ a multi-faceted process for risk assessment and financial viability. This guide details essential stages, from comprehensive credit analysis and rigorous due diligence to advanced financial modeling and strategic covenant structuring. It emphasizes navigating Europe’s diverse regulatory landscapes and market conditions, crucial for effective cash flow analysis, collateral valuation, and overall risk assessment. Mastering the ability to underwrite corporate loan agreements in this complex environment ensures sustainable debt repayment and mitigates cross-border challenges.

DDTalks specializes in organizing premium B2B financial conferences focused on European private credit, NPLs, and structured finance. Our events facilitate high-value deal-making and provide expert insights into complex market dynamics, supporting professionals in navigating the intricacies of European financial markets.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

To underwrite a corporate loan in the European mid-market, lenders use a multi-stage process to manage risk. This guide details the steps from credit analysis and due diligence to financial modeling and structuring loan agreements. It covers the financial metrics, best practices, and regulatory and market considerations for lending to mid-market companies across Europe.

What is Corporate Loan Underwriting in the European Mid-Market?

Corporate loan underwriting is the process lenders use to assess a borrower’s creditworthiness and determine loan risk. Its purpose is to verify the borrower’s ability to repay the debt on the proposed terms. This involves evaluating the company’s financial health, business model, management team, and market position.

The European mid-market adds complexity due to diverse legal systems, fragmented regulatory environments, and varying economic conditions across countries. Underwriters must navigate cross-border nuances, from local insolvency laws to directives like the Alternative Investment Fund Managers Directive (AIFMD II). The process requires financial acumen and an understanding of regional market dynamics to structure a profitable and sustainable loan.

The Foundational Steps: Credit Analysis and Due Diligence

Credit analysis and due diligence are fundamental to identifying risks and assessing the borrower’s capacity to service its debt.

Comprehensive Credit Analysis: Assessing Borrower Capacity

Credit analysis reviews historical financial statements (typically 3-5 years) and projections to assess financial stability. Focus areas include cash flow analysis to assess liquidity and the primary source of repayment.

The evaluation uses the “5 C’s of Credit”:

- Character: The borrower’s reputation and track record of meeting financial obligations.

- Capacity: The ability to repay the loan, primarily measured by historical and projected cash flows (e.g., EBITDA).

- Capital: The amount of equity the owners have invested in the business, indicating their commitment.

- Collateral: Assets pledged as security for the loan, providing a secondary source of repayment.

- Conditions: The economic and industry environment in which the business operates, as well as the intended purpose of the loan.

Rigorous Due Diligence for European Mid-Market Firms

Due diligence validates information from the credit analysis. Financial due diligence confirms financial statements, while operational due diligence assesses business processes and supply chains. Legal due diligence in Europe involves checks on corporate structure, contracts, and compliance with national and EU regulations. Understanding the opportunities and risks in European middle-market lending is part of this stage. Assessing the management team provides insight into the company’s strategic direction and execution.

Financial Modeling & Risk Assessment: Quantifying European Mid-Market Debt

Financial modeling and risk assessment translate data into a view of debt capacity and potential vulnerabilities. This stage quantifies the borrower’s ability to perform under various scenarios to inform loan structure.

Key Financial Models for Loan Underwriting

Financial modeling tests assumptions about a company’s future performance. Common models for mid-market loans include a three-statement model (Income Statement, Balance Sheet, Cash Flow Statement) to project financial health. A Discounted Cash Flow (DCF) analysis is often used to determine the business’s intrinsic value and inform collateral valuation.

Sensitivity analysis and scenario planning model different outcomes—a base case, an upside case, and a downside case—to understand how events like a 10% revenue drop or rising input costs would impact debt service. This stress testing helps set covenant levels and define the loan’s risk profile.

Identifying and Mitigating European Market Risks

Risk assessment extends beyond financials to the market environment. Evaluated risks include sector-specific issues like technological disruption, regulatory changes, geopolitical factors, and currency fluctuations. Mitigation strategies can involve requiring business insurance, hedging, or structuring flexible loan terms. Developing European private credit risk management frameworks is part of this process.

Structuring for Success: Covenants, Collateral, and European Nuances

Loan structuring translates analysis and modeling insights into a legal framework. It defines the terms, conditions, and security package to align lender and borrower interests and mitigate lender risk. The nuances of European legal systems make this stage complex.

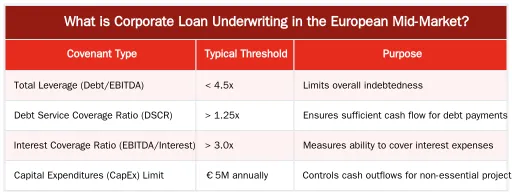

Crafting Effective Loan Covenants for European Deals

Covenants are a tool for monitoring financial health and controlling risk during the loan term. They are contractual agreements requiring the borrower to perform certain actions (affirmative covenants) or refrain from others (negative covenants).

Financial covenants set performance thresholds. Key metrics include:

- Debt Service Coverage Ratio (DSCR): Measures cash flow available to pay current debt obligations. A typical minimum DSCR is 1.25x.

- Leverage Ratio: Compares total debt to EBITDA, capping the amount of debt a company can take on.

- Loan-to-Value (LTV): Used when specific assets are pledged as collateral, limiting the loan amount relative to the asset’s appraised value.

Despite the trend towards covenant-lite lending in Europe, a defined covenant package provides early warning signs of financial distress.

Valuing Collateral and Legal Documentation in Europe

Collateral valuation provides a secondary source of repayment in a default. It involves appraising pledged assets like real estate, accounts receivable, or inventory. In Europe, perfecting a security interest varies by jurisdiction, making the process complex. Underwriters must work with local legal counsel to ensure the lender’s claim is enforceable. Drafting legal documentation—the loan agreement, security agreements, and guarantees—must reflect the agreed terms and comply with all applicable laws.

Why Expert Insight is Crucial for European Mid-Market Lending

Navigating the European mid-market requires current market intelligence. The landscape evolves with regulatory shifts, economic trends, and changing investor appetites. Access to a network of industry leaders provides an advantage.

Navigating Market Dynamics with Industry Leaders

Forums uniting General Partners (GPs), Limited Partners (LPs), and legal advisors provide insights for underwriting corporate loans. Specialized events offer real-time data on deal structures, market terms, and emerging risks not found in public filings. Understanding how peers structure deals in response to interest rates or geopolitical events helps underwriters manage risk and remain competitive. This collaborative intelligence, noted by institutions like the European Banking Authority, helps maintain a healthy credit market.

The rise of private credit introduced underwriting approaches that emphasize cash flow and enterprise value over hard assets, differing from traditional bank lending.

Mastering European Mid-Market Underwriting: Key Takeaways

Underwriting a corporate loan for a European mid-market company requires financial analysis, due diligence, and risk assessment. It demands an understanding of the borrower and Europe’s legal and economic environments. By focusing on structuring, documentation, and learning from market leaders, lenders can manage risk and build lending relationships. Staying connected to market expert networks is essential.

For insights on the European private credit landscape and to connect with industry leaders, explore our upcoming events. Request Agenda for our next conference or contact us.

Frequently Asked Questions

What is the first step to assess a European mid-market corporate loan?

The initial step is a comprehensive credit analysis, starting with a detailed review of the borrower’s historical and projected financial performance. This involves assessing cash flow stability, profitability, and balance sheet strength to determine the capacity to service debt within the specific economic context of its European market.

What key financial metrics are analyzed when you underwrite a corporate loan?

Key metrics include EBITDA, Debt Service Coverage Ratio (DSCR), and leverage ratios like Debt/EBITDA. To properly underwrite a corporate loan, analysts must stress-test these metrics under various economic scenarios relevant to the borrower’s European operating region. This quantitative rigor is fundamental to assessing repayment capacity.

Why is covenant structuring so important when you underwrite a corporate loan?

Covenants are crucial risk management tools that act as early warning signals if a borrower’s performance deteriorates, allowing lenders to take corrective action. Structuring appropriate financial and operational covenants is a core part of the skill needed to underwrite a corporate loan effectively, protecting the lender’s capital.

What non-financial factors are considered during due diligence?

Beyond financials, due diligence involves assessing the quality of the management team, the company’s competitive position, and the resilience of its business model. It also includes a thorough review of the legal and regulatory landscape in the specific European country, which can significantly impact risk.

How do you underwrite a corporate loan considering diverse European regulations?

Underwriting in Europe requires a country-by-country approach to legal and regulatory diligence. Lenders must analyze local insolvency laws, collateral perfection requirements, and any specific industry regulations, such as those impacted by AIFMD II. This localized expertise is essential to accurately underwrite a corporate loan and structure an enforceable agreement.

Where can I learn more about advanced European mid-market lending strategies?

For deeper insights into direct lending strategies and the latest market trends, industry professionals often attend specialized forums. You can explore the agenda for our upcoming European private credit conferences to connect with leading GPs, LPs, and advisors. To see the full list of topics and speakers, you can request the agenda here.

0 Comments