Italian NPL Market: Post-gacs Trends and Investment Opportunities

The italian npl market has undergone a significant transformation following the conclusion of the GACS scheme. This article explores the evolving landscape, highlighting the increasing prominence of Unlikely to Pay (UTP) loans and the sustained importance of securitisation as key drivers. Readers will gain insights into post-GACS trends, the strategies adopted by major servicers like doValue and Prelios, and the new investment opportunities emerging for institutional investors navigating non-performing exposures in Italy. Understanding these dynamics is crucial for effective portfolio management and strategic engagement within the Italian distressed debt sector.

DD Talks provides authoritative insights into European private credit and NPL markets. Our content reflects expertise gained from hosting elite B2B financial conferences, connecting industry leaders and facilitating high-value deal-making in distressed debt and structured finance.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

The italian npl market has transformed from a crisis-driven environment to a mature landscape since the GACS scheme ended. Key trends in 2026 include the rise of Unlikely-to-Pay (UTP) assets, new strategies from key servicers, and the persistent role of securitisation, creating new dynamics for institutional investors managing non-performing exposures.

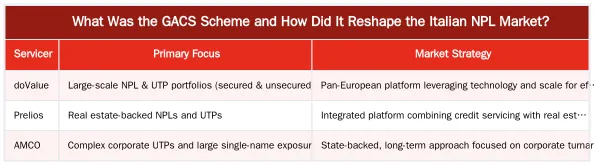

What Was the GACS Scheme and How Did It Reshape the Italian NPL Market?

The GACS (Garanzia sulla Cartolarizzazione delle Sofferenze) scheme was a state guarantee introduced in 2016 to help Italian banks dispose of non-performing loans. It provided a government guarantee on the senior, least risky tranches of NPL securitisations, making them more attractive to institutional investors. This mechanism de-risked transactions and accelerated the cleanup of bank balance sheets across Italy.

The Legacy of GACS: De-risking and Market Catalysis

The GACS scheme catalysed Italy’s distressed debt sector. By mitigating risk for senior noteholders, it unlocked billions in capital and facilitated the transfer of NPL portfolios from banks to specialized investors and servicers. This process reduced the gross NPL stock on bank balance sheets, with institutions like Monte dei Paschi di Siena making extensive use of the facility, and fostered a competitive NPL servicing industry. The scheme’s success attracted international private equity and credit funds, transforming Italy into one of Europe’s most active markets for non-performing exposures.

Beyond GACS: The Current Regulatory Landscape

Since the GACS scheme expired in mid-2022, the market operates without this direct state support for new transactions. The regulatory environment is shaped by European Central Bank (ECB) guidelines on NPL management, which require timely provisioning and disposal. Banks and investors now rely on market-based credit enhancement and structuring techniques for successful securitisations. This places greater emphasis on due diligence, asset quality, and servicer efficiency, creating a mature but more challenging environment.

Navigating the Post-GACS Landscape: Key Trends and Emerging Segments

Post-GACS, the Italian non-performing loan market’s focus has shifted. While legacy NPL disposals continue, activity has moved to more complex asset classes. Investors and servicers are adapting strategies for a new wave of distressed and sub-performing credit, emphasizing assets that require active management to unlock value.

The Rise of UTP Loans: A New Frontier for Investors

The primary trend is the rise of Unlikely to Pay (UTP) loans. Unlike NPLs, which are typically non-viable and liquidated, UTPs are loans to borrowers in financial difficulty who are often still operating. This category’s goal is a proactive turnaround of the borrower, not just recovery through foreclosure. Managing UTPs requires blending credit management with corporate restructuring and industrial expertise. This shift is a core theme when Navigating the NPL and Distressed Debt Landscape in Southern Europe, demanding a more hands-on approach from investors and servicers.

Italian Real Estate as a Driver in Distressed Debt Recovery

A substantial portion of Italian NPL and UTP portfolios is secured by real estate. The Italian real estate market drives recovery values and investment strategies. Investors now focus on the quality of underlying collateral. Strategies often involve active asset management, like completing unfinished construction, repositioning commercial properties, or facilitating residential sales. Real estate market performance directly influences distressed debt portfolio pricing and workout plan viability.

Who Are the Key Players in Italian NPL Servicing and Investment?

The Italian distressed debt landscape is dominated by specialized servicers and institutional investors. Their strategies have evolved for a market transitioning from large-scale NPL disposals to granular UTP workouts. NPL servicing in Italy has consolidated, with a few major platforms managing most assets.

Leading NPL Servicers: doValue, Prelios, and Beyond

Several large servicers lead the market. doValue and Prelios are prominent, managing tens of billions of euros in distressed assets. They offer end-to-end services, from due diligence and portfolio management to legal enforcement and real estate asset management. Their strategies focus on technology-driven efficiency and specialized teams for UTP restructuring. Other servicers cater to niches like unsecured consumer credit or smaller corporate loans. This environment has spurred talk of a new wave of banking consolidation in Italy as specialized entities refine their focus.

AMCO’s Strategic Role in Italian Distressed Debt

AMCO, an asset management company fully owned by the Italian Ministry of Economy and Finance, functions as a de facto Italian bad bank. It acquires and manages large, complex distressed credit portfolios, particularly from banks undergoing restructuring. Its mandate allows a longer-term view on recovery, focusing on industrial turnaround plans for UTP exposures. AMCO’s presence stabilizes the market and makes it a significant counterparty in large transactions, influencing pricing and recovery standards.

What Are the Investment Opportunities and Challenges in Italian NPL Securitisation?

Securitisation is a cornerstone of the Italian distressed debt market, even post-GACS. For banks, it is a tool for balance sheet management; for investors, it offers structured exposure to the asset class. The mechanics of securitisation in Italy are well-established, but the post-GACS environment presents new opportunities and hurdles.

Acquiring NPL Portfolios: Strategies for Institutional Investors

Institutional investors acquire NPL and UTP portfolios through competitive bidding processes organized by banks and their advisors. Successful acquisition requires rigorous due diligence, involving loan data analysis, collateral value assessment, and projecting recovery rates and timelines. Investors must accurately price portfolio risk, factoring in servicing costs and potential legal delays. Post-acquisition, value is created through efficient servicing and proactive asset management, often involving complex negotiations and restructuring, as seen in recent NPL securitization deals.

Navigating Legal and Valuation Challenges in Distressed Debt

Investors face challenges. The Italian legal system, while improved, can still cause lengthy recovery timelines for secured loans, impacting returns. Accurate valuation of underlying collateral, especially for complex real estate or industrial assets, is critical and difficult. The shift to UTPs adds complexity, requiring assessment of business turnaround viability rather than just asset liquidation. Regulatory compliance and reporting standards also add operational complexity for investors.

Expert Outlook: Future Trends and Strategic Insights for the Italian NPL Market

The Italian non-performing loan market in 2026 and beyond continues to evolve, with more sophisticated strategies and new capital sources. Industry forums indicate a focus on specialization, technology, and the convergence of distressed debt and private credit strategies.

The Evolution of Private Credit and Distressed Debt Strategies

A key trend is the blurring line between distressed debt investing and direct lending. As investors become more involved in UTP workouts, they provide rescue financing and new capital for corporate turnarounds. This attracts private credit funds with the flexibility to structure complex financing. Expect further servicer consolidation for economies of scale and more use of technology like AI and data analytics to improve underwriting and recovery. While GACS has ended, discussions on new public-private partnership models or a next-generation Italian bad bank may resurface to address future non-performing exposures, as challenges remain with Stage 2 loans.

Connecting with Industry Leaders at European Debt Summits

Understanding these trends requires direct engagement with market leaders. DD Talks’ European financial conferences bring together general partners, limited partners, investment bankers, and servicers to analyze market data, debate investment theses, and originate deals. The panels and networking provide insight into capital flows and how successful players adapt to the post-GACS reality. According to the Bank of Italy, monitoring credit quality remains a top priority, a theme explored at these events.

Unlock Exclusive Insights at DD Talks’ European Financial Conferences

Navigating the European distressed debt and private credit landscape requires direct access to industry pioneers. DD Talks hosts annual events in financial hubs like London and Madrid for deal-making and networking. Our conferences are a confidential platform for institutional investors, fund managers, and advisors to analyze emerging trends, evaluate opportunities, and build partnerships. Gain the intelligence to capitalize on the evolving Italian market and beyond.

Conclusion

The Italian distressed asset market has transitioned to a new phase defined by the rise of UTPs, the role of real estate, and the strategies of specialized servicers and investors. While the GACS scheme was a catalyst, the market’s current maturity offers different opportunities. Success in 2026 requires expertise in corporate restructuring, active asset management, and understanding the legal and regulatory framework. To learn more about our forums, contact us or Request Agenda for our upcoming events.

Frequently Asked Questions

What was the GACS scheme and how did it impact the italian npl market?

GACS (Garanzia sulla Cartolarizzazione delle Sofferenze) was a state guarantee on the senior tranches of non-performing loan securitisations. This government backing significantly de-risked transactions for investors, which catalyzed the italian npl market by enabling banks to offload billions in bad loans from their balance sheets. The scheme’s success fundamentally reshaped the landscape for distressed debt in Italy.

What are the primary trends shaping the italian npl market after the GACS scheme ended?

Post-GACS, the focus has shifted decisively towards the Unlikely-to-Pay (UTP) loan category, which requires more hands-on corporate restructuring and turnaround expertise. Additionally, there is a growing secondary market for portfolios previously sold under GACS, creating new liquidity events. These trends define the current opportunities within the italian npl market for specialized investors.

Who are the key players in the italian npl market?

The servicing landscape is led by large, specialized firms such as doValue, Prelios, and Gardant, which manage the complex workout and recovery processes. On the investment side, major international private equity funds and distressed debt specialists are highly active. These key players drive transactions and strategy across the italian npl market.

What are ‘Unlikely-to-Pay’ (UTP) loans and why are they important now?

UTPs are a specific Italian loan classification for exposures where a bank believes the borrower is unlikely to meet their credit obligations without intervention. Unlike defaulted NPLs, UTPs often involve still-operating businesses, presenting investors with opportunities for active turnaround management rather than simple liquidation. This makes them a crucial and growing segment of the distressed debt landscape in Italy.

What are the main investment opportunities in Italian NPL securitisation today?

Key opportunities in Italian NPL securitisation now lie in the secondary trading of existing notes and in structuring new deals without state guarantees. Investors are increasingly focused on specialized asset classes like distressed real estate, SME loans, and UTP portfolios. Success requires deep underwriting expertise and strong local servicing partnerships to manage these complex assets effectively.

How can investors get expert insights and network with key players in the European NPL sector?

Gaining direct access to market leaders is crucial for navigating the complexities of European distressed debt. Attending specialized B2B forums, like those organized by DD Talks, provides a platform for high-value networking with top-tier investors, servicers, and advisors. You can learn about upcoming events and discussions by requesting an agenda from our website.

0 Comments