AIFMD II Loan Origination Funds: Navigating New European Direct Lending Rules

AIFMD II loan origination funds face a new harmonized European regulatory framework designed to enhance financial stability and investor protection within the direct lending market. This directive introduces specific requirements for funds primarily originating loans, including stringent leverage limits and mandatory risk retention rules. Fund managers must implement robust credit risk management and conflict of interest policies, ensuring compliance and strategic adaptation. Understanding these changes is crucial for navigating the evolving landscape of European private credit and maintaining operational integrity.

DD Talks organizes premium B2B financial conferences, providing essential insights into European private credit, NPL, and structured finance markets. Our platforms facilitate high-value deal-making and industry networking, connecting top-tier GPs and LPs with critical regulatory updates.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

The updated AIFM directive introduces specific rules for aifmd ii loan origination funds, creating a harmonized framework that impacts the European private credit market. This article analyzes the new requirements for leverage, risk management, and fund structuring, outlining steps for compliance and strategic adaptation.

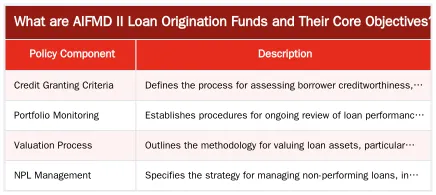

What are AIFMD II Loan Origination Funds and Their Core Objectives?

AIFMD II loan origination funds are Alternative Investment Funds (AIFs) whose primary investment strategy is to originate loans. The rules establish a unified European regulatory framework to enhance financial stability, improve investor protection, and manage systemic risks from private credit and direct lending activities.

Defining ‘Loan Origination Fund’ Under AIFMD II

Under the AIFM directive, a fund is a “loan-originating AIF” if its strategy is mainly to originate loans or if the notional value of its originated loans is at least 50% of its net asset value (NAV). This classification subjects these funds to new, harmonized rules that do not apply to AIFs with other strategies, like acquiring secondary loans.

The Primary Goals of AIFMD II for Direct Lending

The regulations address the increasing role of non-bank lending in the European economy by ensuring fund managers (AIFMs) have systems and controls for underwriting and monitoring credit. Standardized rules on leverage, liquidity management, and risk diversification safeguard investor protection, prevent excessive systemic risk, and create a level playing field for direct lending funds across the EU.

Operational Compliance: Managing Credit Risk and Conflicts of Interest

AIFMD II emphasizes fund managers’ internal policies and procedures. Compliance requires frameworks for managing the credit lifecycle and addressing conflicts of interest.

Implementing Credit Risk Management Policies

AIFMs must implement and maintain detailed policies for credit risk management. Regulators expect a framework covering the credit origination process, from assessment to maturity or disposal. The policies must be documented, reviewed, and implemented for sound lending and portfolio monitoring.

Preventing Asset Stripping and Managing Conflicts of Interest

The directive’s asset stripping rules apply for 24 months after an AIF acquires control of a non-listed company or issuer. These rules restrict distributions, capital reductions, and share redemptions that could undermine the target company’s capital base, preventing predatory strategies that extract value at the company’s expense.

AIFMs must have a conflict of interest policy, especially when the AIFM has relationships with borrowers, sponsors, or other market participants. The policy must identify potential conflicts and establish procedures to manage or disclose them to protect investor interests.

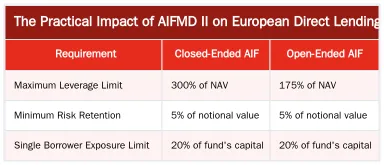

The Practical Impact of AIFMD II on European Direct Lending

AIFMD II will reshape the European direct lending market. The regulations add operational complexity but also increase market maturity and investor confidence. The impact affects fund structuring, investment strategy, and the competitive landscape for private credit.

Shaping Fund Structuring and Investment Strategies

The new rules influence how managers design and operate funds. The preference for closed-ended structures and leverage caps requires some managers to adjust their models. Funds that relied on higher leverage may need to revise return targets or seek alternative financing. The diversification rule encourages broader portfolios over highly concentrated strategies. For more on this, see our guide to direct lending fund structures in Europe.

The framework for aifmd ii loan origination funds creates a more stable and predictable environment, which could attract more institutional capital to the asset class.

Enhancing Investor Protection and Market Transparency

The updated directive enhances investor protection. Requirements for risk management, conflict of interest policies, and asset stripping restrictions improve fund governance and operational integrity. According to the European Securities and Markets Authority (ESMA), these measures foster transparency and trust. Increased transparency standardizes due diligence, simplifies fund comparisons for LPs, and fosters a more efficient market.

Preparing for AIFMD II: Key Steps for Fund Managers

Assessing Current Structures and Identifying Gaps

Managers should perform a gap analysis, reviewing existing fund documentation, internal policies, and operational workflows against the new requirements. This assessment should cover leverage calculations, risk retention procedures, diversification limits, and credit management frameworks. Identifying non-compliance early allows time for corrective actions, like amending fund prospectuses or updating policy manuals.

Leveraging Expert Guidance and Industry Forums

Engaging with legal and regulatory advisors helps ensure correct interpretation and application of the rules. Industry forums provide insights into best practices and market standards. Events like DDTalks conferences offer a platform to hear from regulators, legal experts, and fund managers navigating these changes. For official guidance, consult resources from regulatory bodies like the European Banking Authority (EBA).

Stay Ahead in European Private Credit with DDTalks

The European private credit landscape is shaped by regulatory developments like AIFMD II. DDTalks is a platform for industry leaders to convene, share insights, and form strategic partnerships.

Connect with Industry Leaders at Our Upcoming Events

Our conferences in London, Madrid, and across Europe gather GPs, LPs, and advisors to discuss topics from regulatory compliance to deal sourcing and fund structuring. Attendees can engage in discussions, network, and gain strategic intelligence.

Conclusion

The AIFMD II framework matures the European private credit market by establishing clear rules for leverage, risk management, and investor protection, fostering a more stable and transparent environment for loan origination funds. While requiring operational adjustments, the changes strengthen the asset class and its appeal to institutional investors. Contact us for more information or Request Agenda for our next private credit conference.

Frequently Asked Questions

What is the main objective of the AIFMD II rules for loan-originating funds?

The primary goal is to establish a harmonized European framework for the rapidly expanding private credit market. These rules aim to bolster financial stability, enhance investor protection, and manage potential systemic risks by setting clear standards for leverage, risk management, and operational conduct for aifmd ii loan origination funds.

Are all direct lending funds subject to the new rules for aifmd ii loan origination funds?

The regulations specifically target Alternative Investment Funds (AIFs) where the notional value of originated loans is at least 50% of the fund’s net asset value (NAV). Direct lending funds that fall below this significant threshold may not be subject to the full scope of these specific requirements.

What are the leverage limits imposed on aifmd ii loan origination funds?

The directive imposes specific leverage caps to mitigate systemic risk. Open-ended funds are limited to 175% leverage, while closed-ended funds have a higher limit of 300%, calculated based on the fund’s exposure relative to its Net Asset Value (NAV).

Does the updated AIFM directive require risk retention for originated loans?

Yes, the directive mandates a “skin-in-the-game” approach through risk retention rules. Funds must retain a net economic interest of 5% of the notional value of any loans they originate and then transfer to third parties, ensuring the fund manager’s interests are aligned with those of investors.

Can a loan origination fund be open-ended under the new directive?

Yes, but with strict conditions to manage liquidity risk. An Alternative Investment Fund Manager (AIFM) must prove to national regulators that the fund has a robust and appropriate liquidity management system. Due to the illiquid nature of the underlying assets, most aifmd ii loan origination funds are structured as closed-ended vehicles to prevent potential liquidity mismatches.

How can I learn more about the practical impact of the regulations on aifmd ii loan origination funds?

To gain deeper insights from industry leaders on navigating these new regulations, you can explore the agenda for our upcoming European private credit conferences. Our events bring together top-tier GPs, LPs, and legal advisors to discuss the practical impact of the directive on fund structuring. You can request the full agenda to see the specific topics and speakers.

0 Comments