Choosing the Right Domicile: Optimizing European Private Credit Fund Structures

Choosing the right domicile for a European private credit fund is critical for regulatory compliance, tax efficiency, and investor appeal. This article details the strategic considerations when evaluating Luxembourg vs. Ireland, two leading jurisdictions. It compares their distinct fund structures, such as Ireland’s ICAV and Luxembourg’s RAIF and SCSp, alongside their respective regulatory environments under the Central Bank of Ireland and CSSF. Understanding these differences is essential for fund managers seeking optimal EU marketing passport access and robust operational ecosystems.

DDTalks provides authoritative insights into European private credit markets and fund structuring. This content offers practical guidance for institutional investors and fund managers navigating complex domiciliation decisions, drawing on deep industry expertise.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

Choosing the right domicile for a European private credit fund impacts regulatory compliance, tax efficiency, and investor appeal. This article compares Luxembourg and Ireland, the two leading jurisdictions, examining their fund structures, regulatory environments, and practical considerations to inform strategic choices for 2026 and beyond.

Why Luxembourg and Ireland Lead European Fund Domiciliation

Luxembourg and Ireland are Europe’s leading fund domiciles because of their stable political environments, regulatory frameworks aligned with EU directives, and deep professional talent pools. Their commitment to the investment funds industry creates familiarity and confidence among global institutional investors, making them default options for managers accessing European capital.

The Strategic Advantages of EU Fund Hubs

Funds domiciled in either country have access to the EU marketing passport. Under the Alternative Investment Fund Managers Directive (AIFMD), this allows an authorized Alternative Investment Fund Manager (AIFM) to market a fund to professional investors across all EU member states with a single authorization, streamlining capital raising and reducing cross-border administrative burdens.

Their political and economic stability, and commitment to international transparency and anti-money laundering (AML) standards, provide a secure environment for long-term investment vehicles like private credit funds.

Investor Confidence and Specialized Ecosystems

Decades of focus on the funds industry have cultivated sophisticated ecosystems in both Dublin and Luxembourg, including experienced fund administrators, depositaries, legal advisors, and auditors specializing in alternative assets. This expertise ensures efficient fund setup, administration, and compliance. For LPs, this provides confidence in the fund’s governance, a key factor in their allocation decisions.

Key Fund Structures: ICAV vs. RAIF & SCSp Explained

The choice between Ireland and Luxembourg often depends on the legal and tax characteristics of their flagship fund vehicles, which offer distinct advantages for private credit.

Ireland’s ICAV and QIAIF: Flexibility for Global Investors

The Irish Collective Asset-management Vehicle (ICAV) is a corporate fund structure. Its primary advantage for US investors is the ability to “check-the-box” to be treated as a tax-transparent partnership for US federal income tax, avoiding potential tax friction for US-based LPs and GPs.

An ICAV is typically a Qualified Investor Alternative Investment Fund (QIAIF), a regulated vehicle authorized and supervised by the Central Bank of Ireland. The formal approval process provides regulatory certainty and is well-regarded by institutional investors.

Luxembourg’s RAIF and SCSp: Speed and Adaptability

Luxembourg offers the Reserved Alternative Investment Fund (RAIF) and the Special Limited Partnership (SCSp). The RAIF is an AIF not directly supervised by the Luxembourg regulator (CSSF), but by its appointed, regulated AIFM. This accelerates time to market because the fund itself does not require regulatory approval.

The SCSp is a partnership structure similar to common law limited partnerships familiar to UK and US managers. It offers high contractual flexibility, allowing the limited partnership agreement (LPA) to govern fund operations with minimal mandatory legal provisions. This adaptability makes it ideal for bespoke private credit and direct lending strategies.

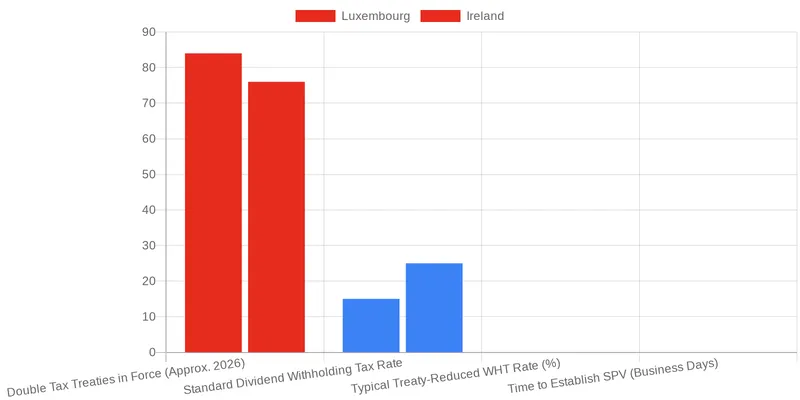

Tax Efficiency and Double Tax Treaties: Which Domicile Wins?

Tax considerations directly impact investor returns. Both Luxembourg and Ireland offer tax-neutral environments for fund vehicles, so the fund itself is generally not subject to tax on its income or gains. Key differentiators are their double tax treaty networks and provisions for certain investor groups.

Optimizing Investor Returns Through Treaty Networks

An extensive double tax treaty (DTT) network is crucial for private credit funds investing across multiple jurisdictions. These treaties can reduce or eliminate withholding taxes on interest payments from portfolio companies, enhancing returns. Both countries have broad treaty networks. The optimal choice depends on the fund’s investment geography and LP domiciles.

US Tax Transparency and Withholding Tax Considerations

The Irish ICAV’s ability to “check the box” is a significant structural advantage for attracting US taxable investors. While a Luxembourg SCSp is also tax-transparent, achieving the same outcome for US investors can require more complex downstream structuring. For non-US investors, both jurisdictions offer efficient vehicles to mitigate tax leakage, but the mechanics differ. A review of withholding tax implications on distributions to LPs in various jurisdictions is necessary.

Operational Substance and Ecosystem: A Strategic Advantage

The practicalities of running a fund are also critical. Operational substance and the quality of the local service provider ecosystem are increasingly important. International tax initiatives, like the OECD’s BEPS project, have increased scrutiny on ensuring fund management activities have economic substance in their domicile.

Meeting Substance Requirements for Private Credit Funds

Substance involves demonstrating that key decisions and risk management functions are performed in the fund’s domicile. This can include local directors, an office, and expert staff. Both Luxembourg and Ireland have clear expectations and infrastructure to help managers meet these requirements. This includes experienced independent directors and third-party AIFMs that provide the personnel and physical presence to satisfy regulatory demands.

The Fund Administration and Legal Advisory Landscape

A private credit fund’s success relies on its operational partners. Both Dublin and Luxembourg host leading fund administrators, depositaries, and law firms. According to the Association of the Luxembourg Fund Industry (ALFI), Luxembourg specializes in private equity and real estate structures, which applies well to private credit. Ireland’s common law system gives it a strong reputation in hedge funds and structures favored by US and UK managers. Expertise in complex loan administration, valuations, and investor reporting is a key strength of both financial centers.

Making the Right Choice for Your Private Credit Fund

Selecting a fund location is not about finding a universally “better” option, but the one that best aligns with a fund’s strategy, investor base, and operational model.

Key Decision Factors for GPs and LPs

Managers should weigh several factors. The geographic location of target LPs is paramount; a strong US investor base may favor Ireland’s ICAV. Investment strategy also matters, as jurisdictions may have more experience with specific asset types. Speed to market can be a deciding factor for opportunistic strategies, potentially favoring Luxembourg’s RAIF. The GP’s comfort with a regulatory approach and existing service provider relationships can also influence the choice. These are core topics covered in our guide on tax and legal considerations for GPs.

Future-Proofing Your Fund Domicile Strategy

The regulatory and tax landscape is constantly evolving. A domicile choice must remain effective for the fund’s life, often ten years or more. This requires selecting a jurisdiction with a proven commitment to the funds industry and the political stability to adapt to future changes like new AIFMD versions or global tax standards. Engaging with legal and tax advisors who understand both jurisdictions is crucial for building a resilient and efficient structure, a theme explored when analyzing direct lending fund structures.

Connect with European Private Credit Leaders at DDTalks

DDTalks conferences provide a platform for GPs, LPs, and advisors to engage in high-level discussions on fund domiciliation, regulatory changes, and deal sourcing.

Join industry leaders to gain insights into the latest trends in fund structuring and European private credit. To learn more about our upcoming events and expert panels, Request Agenda or contact us.

Conclusion

The choice between Luxembourg and Ireland for a private credit fund is nuanced, with no single correct answer. Ireland’s ICAV offers advantages for US investors, while Luxembourg’s RAIF and SCSp provide flexibility and speed to market. A thorough analysis of investor base, investment strategy, tax implications, and operational needs is essential. Weighing these factors helps fund managers establish an efficient foundation for their European investment activities. For deeper insights and networking opportunities, explore the agenda for our next event. Request Agenda.

Frequently Asked Questions

What is the primary advantage of the Irish ICAV structure for a private credit fund?

The Irish Collective Asset-management Vehicle (ICAV) is highly popular because it is a corporate entity that can elect to be treated as a tax-transparent partnership for US tax purposes. This “check-the-box” capability makes it particularly attractive for US-based LPs and GPs, as it avoids a layer of US tax. This is a key consideration when choosing the right domicile for funds with significant US investor interest.

What is the key benefit of the Luxembourg Reserved Alternative Investment Fund (RAIF)?

The RAIF’s main advantage is its speed to market. It is not directly supervised by Luxembourg’s regulator (the CSSF), but is instead supervised through its regulated Alternative Investment Fund Manager (AIFM). This indirect oversight allows for a much faster setup time compared to directly regulated fund structures, a crucial factor for managers prioritizing a quick launch.

From a regulatory perspective, what is the main difference when choosing the right domicile between Ireland and Luxembourg?

The Central Bank of Ireland (CBI) is often perceived as being more rules-based and rigorous in its approval processes, which some managers prefer for its clarity. In contrast, the Luxembourg CSSF is also highly robust but is sometimes seen as more commercially pragmatic in its approach. Both are highly respected, so the decision when choosing the right domicile often depends on the manager’s preference for regulatory interaction style.

How does the investor base influence choosing the right domicile for a private credit fund?

The geographic location and tax status of your Limited Partners (LPs) are critical factors. For instance, the Irish ICAV’s tax election is a major draw for US investors, while certain European or Asian investors may have a preference for Luxembourg structures due to specific tax treaty benefits. Understanding your target LPs is fundamental to choosing the right domicile to maximize investor appeal and tax efficiency.

Which country offers a better tax treaty network for investment funds?

Both Luxembourg and Ireland have extensive and excellent double tax treaty networks, which is a primary reason for their popularity as fund hubs. The choice often comes down to the specific jurisdictions where the fund intends to invest its capital. A detailed analysis is required to see if one country has a slightly more favorable treaty with a particular target investment country.

Where can I discuss fund structuring and the nuances of choosing the right domicile with industry experts?

To gain deeper insights and network with leading GPs, LPs, and legal advisors, consider attending a specialized industry event like those hosted by DDTalks. Our European private credit conferences provide a dedicated forum for high-level discussions on topics like AIFMD II, fund structuring, and domicile selection, allowing you to connect with the experts who navigate these complex decisions daily.

0 Comments