Synthetic Vs True Sale Securitisation: Navigating NPL Risk Transfer

The distinction between synthetic vs true sale securitisation for Non-Performing Loans (NPLs) lies in how risk and assets are transferred. True sale securitisation involves the legal transfer of NPL portfolios to a Special Purpose Vehicle (SPV), removing them from the originator’s balance sheet. Conversely, synthetic securitisation transfers only the credit risk associated with NPLs, often using credit default swaps, while the assets remain with the originator. Both methods facilitate capital relief and balance sheet management for financial institutions, but differ significantly in operational complexity, regulatory capital treatment, and investor exposure to underlying assets. Understanding these differences is crucial for effective NPL securitisation strategies.

DDTalks provides expert insights into complex financial instruments like NPL securitisation. Our platform connects institutional investors, NPL servicers, and structured finance professionals at premium European conferences, fostering informed decision-making and high-value deal-making in distressed debt markets.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

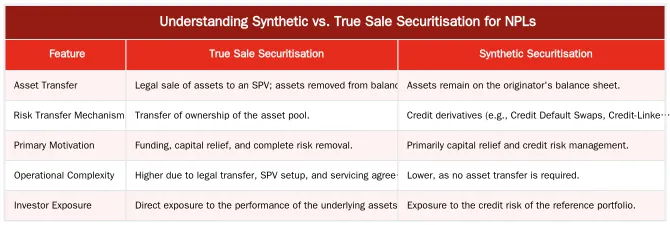

Understanding Synthetic vs. True Sale Securitisation for NPLs

The distinction in the synthetic vs true sale securitisation debate is how assets and risk are treated. True sale securitisation involves the legal sale and physical transfer of assets off an originator’s balance sheet, whereas synthetic securitisation transfers only the credit risk associated with those assets using derivatives, while the assets remain with the originator.

What is True Sale Securitisation?

In a true sale securitisation, a financial institution (the originator) pools a portfolio of assets, such as non-performing loans (NPLs), and sells them to a legally separate Special Purpose Vehicle (SPV). This transaction is a “true sale,” meaning the originator legally derecognises the assets from its balance sheet. The SPV issues asset-backed securities (ABS) to investors, using the proceeds to pay the originator for the NPL portfolio. This structure isolates the assets from the originator’s credit risk.

What is Synthetic Securitisation?

Synthetic securitisation achieves risk transfer without the legal sale of assets. The originator keeps the NPL portfolio on its balance sheet but transfers the credit risk to investors through credit-linked notes or credit default swaps (CDS). The originator (the protection buyer) pays a premium to investors (the protection sellers), who agree to cover specified losses on the NPL portfolio. This method is preferred for its operational simplicity and ability to manage risk on assets that are difficult to transfer legally.

How Do These Securitisation Structures Work for NPLs?

The operational mechanics for managing NPL portfolios differ between true sale and synthetic structures. The choice of structure impacts legal execution, investor engagement, and ongoing servicing requirements.

The Mechanics of True Sale for NPL Portfolios

In a true sale NPL transaction, the originating bank identifies and pools a portfolio of non-performing loans. This portfolio is sold to a newly created SPV. To fund the purchase, the SPV issues several tranches of notes (e.g., senior, mezzanine, junior) to institutional investors. Cash flows from the recovery and workout of the NPLs pay interest and principal on these notes according to their seniority. This structure provides investors with direct exposure to the performance of the underlying NPL assets.

Implementing Synthetic Structures for NPL Risk Transfer

In a synthetic NPL transaction, the bank retains the loans. It enters into a credit derivative contract with investors, often through an SPV that issues credit-linked notes. The bank pays a fee to the investors, who agree to absorb losses on the NPL portfolio up to a certain amount. If credit events occur within the reference portfolio, the investors’ capital is used to compensate the bank. This allows the bank to achieve significant risk transfer and capital relief without the operational complexity of a legal asset sale.

View data as table

| Feature | True Sale Securitisation | Synthetic Securitisation |

|---|---|---|

| Asset Transfer | Legal sale of assets to an SPV; assets removed from balance sheet. | Assets remain on the originator’s balance sheet. |

| Risk Transfer Mechanism | Transfer of ownership of the asset pool. | Credit derivatives (e.g., Credit Default Swaps, Credit-Linked Notes). |

| Primary Motivation | Funding, capital relief, and complete risk removal. | Primarily capital relief and credit risk management. |

| Operational Complexity | Higher due to legal transfer, SPV setup, and servicing agreements. | Lower, as no asset transfer is required. |

| Investor Exposure | Direct exposure to the performance of the underlying assets. | Exposure to the credit risk of the reference portfolio. |

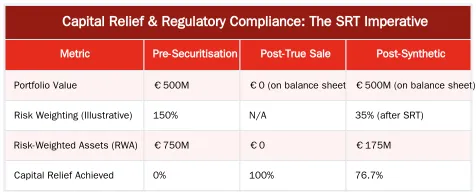

Capital Relief & Regulatory Compliance: The SRT Imperative

For European banks, a primary driver for securitisation is achieving regulatory capital relief. Both transaction types can accomplish this, but they must meet criteria for Significant Risk Transfer (SRT) as defined by regulators. Failure to demonstrate SRT means the bank cannot reduce the risk-weighted assets (RWAs) associated with the portfolio, nullifying the capital benefit.

Achieving Capital Relief: Which Method is Superior?

The effectiveness of each method depends on the originator’s goals. A true sale structure provides more definitive capital relief because the assets are removed from the balance sheet. This can also generate immediate liquidity. Synthetic structures, while not generating funding, can be more efficient for RWA reduction, especially for large, granular portfolios where a true sale would be operationally burdensome. The decision hinges on the trade-off between funding needs and capital optimization efficiency. See our guide on unlocking liquidity and capital relief.

Navigating Significant Risk Transfer (SRT) in Europe

Under the EU Securitisation Regulation, originators must prove to their competent authority that a “significant” amount of credit risk has been transferred to third parties. The European Banking Authority (EBA) provides quantitative thresholds and qualitative requirements to assess SRT. For instance, the regulation requires that the risk-weighted exposure amounts of the mezzanine tranches held by the originator do not exceed 50% of the risk-weighted exposure amounts of all mezzanine tranches. Both synthetic and true sale structures must be designed to meet these tests, ensuring the thickness of the transferred tranches is sufficient to satisfy regulators like the ECB or national authorities.

View data as table

| Metric | Pre-Securitisation | Post-True Sale | Post-Synthetic |

|---|---|---|---|

| Portfolio Value | €500M | €0 (on balance sheet) | €500M (on balance sheet) |

| Risk Weighting (Illustrative) | 150% | N/A | 35% (after SRT) |

| Risk-Weighted Assets (RWA) | €750M | €0 | €175M |

| Capital Relief Achieved | 0% | 100% | 76.7% |

Strategic Implications for European Financial Institutions

The decision between a synthetic or true sale approach is critical to a financial institution’s balance sheet management strategy. This choice is influenced by regulatory pressures, market appetite for risk, and internal operational capabilities. DD Talks facilitates discussions among top-tier institutions on these strategic calculations.

Optimizing Balance Sheets and Risk Management

Financial institutions use these securitisation techniques to manage capital ratios, reduce concentration risk, and free up capacity for new lending. A true sale is employed when a bank exits a non-core asset class or geography. A synthetic transaction allows a bank to manage the risk of a core portfolio while maintaining customer relationships and the underlying assets. This flexibility is crucial for navigating the European NPL landscape, a topic we explore when navigating the evolving NPL landscape.

Investment Opportunities in European NPL Securitisation

Both structures offer distinct opportunities. True sale NPL securitisations provide direct access to asset-backed cash flows, appealing to distressed debt funds and specialised credit investors with workout expertise. Synthetic securitisations, particularly the junior and mezzanine tranches, attract investors seeking higher yields for taking on leveraged credit risk. These instruments are often favoured by hedge funds and private credit firms. The choice of synthetic vs true sale securitisation shapes the risk-return profile available to the market, influencing capital flows across Europe.

Future Trends and Expert Insights in NPL Securitisation

The European securitisation market is evolving, shaped by macroeconomic shifts, technological innovation, and a dynamic regulatory environment.

The Evolving Landscape of European Securitisation

In 2026, there is a resurgence in private securitisation and bespoke structured finance solutions. Many deals are now structured as bilateral transactions between a bank and a single institutional investor or a small club of investors. This allows greater flexibility in structuring and faster execution. Macroeconomic factors, such as rising interest rates and slowing economic growth, are expected to increase NPL formation, fueling the need for securitisation tools. Explore our analysis on The Revival of European ABS and Private Securitisation Structures.

Preparing for Regulatory Shifts and Market Dynamics

Market participants are monitoring potential regulatory adjustments. Discussions around easing aspects of the EU Securitisation Regulation aim to make the framework more efficient and competitive globally. As reported by authorities like ESMA, there is support for a more streamlined process, which could boost market activity. You can read more on how the EU markets watchdog supports moves to ease securitisation rules.

Connect with Industry Leaders at DD Talks Events

DD Talks provides a platform for professionals in the European private credit, NPL, and structured finance markets to connect, share insights, and originate transactions.

Explore Upcoming European Financial Conferences

Our events in financial hubs like London and Madrid bring together general partners, limited partners, investment bankers, and workout specialists. These forums facilitate networking and provide intelligence on market trends, regulatory developments, and investment strategies. To connect with decision-makers, Request Agenda for our upcoming NPL & Distressed Debt Forums.

Conclusion

The choice between synthetic and true sale securitisation depends on the objective. For institutions prioritizing funding and asset disposal, a true sale is the logical path. For those focused on capital efficiency and risk management without asset disposal, a synthetic structure offers an alternative. To join these strategic conversations, contact us or Request Agenda for our next event.

Frequently Asked Questions

How does risk transfer differ between synthetic and true sale NPL securitisations?

In a true sale, both the NPL assets and their associated credit risk are sold to a Special Purpose Vehicle (SPV), achieving full balance sheet removal for the originator. In a synthetic structure, the NPLs remain on the originator’s balance sheet; only the credit risk is transferred to investors, typically via credit derivatives. This distinction is critical for achieving Significant Risk Transfer (SRT) under regulations like the Capital Requirements Regulation (CRR).

What makes synthetic securitisation an efficient tool for capital relief on NPLs?

Banks favour synthetic structures for NPLs to gain regulatory capital relief without the operational complexity and costs of a true asset sale. By transferring the credit risk, a bank can reduce its risk-weighted assets (RWAs) as stipulated by Basel III frameworks, freeing up capital for new lending. This is particularly effective for portfolios where the legal transfer of thousands of individual loans would be prohibitively expensive.

Under IFRS 9, does a true sale offer a cleaner accounting outcome for NPLs?

Yes, a properly executed true sale provides a definitive accounting outcome by achieving full de-recognition of the NPL portfolio from the originator’s balance sheet under IFRS 9. This clean break directly reduces a bank’s reported NPL ratio, a key metric for regulators and investors. A synthetic transaction, while providing capital relief, does not remove the assets themselves from the balance sheet.

How do investors participate in the risk and return of a synthetic NPL deal?

Investors typically purchase credit-linked notes (CLNs) issued by an SPV, which are tranched by risk level such as junior, mezzanine, and senior. The proceeds from these notes are held in a collateral account and invested in highly-rated securities. Investors receive a premium for bearing the credit risk of the underlying NPL portfolio; if portfolio losses exceed a pre-defined threshold, the collateral is used to reimburse the originating bank.

Why have government guarantee schemes like Italy’s GACS historically favoured true sale structures?

Italy’s GACS (Garanzia sulla Cartolarizzazione delle Sofferenze) was designed for true sale securitisations because its primary goal was to physically remove NPLs from bank balance sheets to restore financial stability. The government guarantee applied only to the senior tranche of securities issued by the SPV, which required a legal sale of the assets to be effective. This structure provided investors with confidence and helped create a functioning secondary market for Italian NPLs.

What are the primary operational challenges when structuring a synthetic vs true sale securitisation for distressed assets?

True sale securitisations involve significant operational hurdles, including extensive due diligence on thousands of loans, complex legal transfers of title, and establishing a new servicing arrangement for the SPV. In contrast, the main challenge for a synthetic deal is accurately modelling the NPL portfolio’s expected loss and pricing the credit protection, as the originator continues to service the assets and manage the operational risk.

0 Comments