GACS Italian NPL Securitisation: De-risking & Market Impact

The gacs italian npl securitisation scheme, Garanzia Cartolarizzazione Sofferenze, is a state guarantee designed to facilitate the disposal of non-performing loans (NPLs) from Italian bank balance sheets. It de-risks the senior tranche of NPL securitisations, making them attractive to institutional investors and bridging the valuation gap. This mechanism has been crucial in reshaping Italy’s NPL market by stimulating a secondary market for distressed debt. Readers will understand how GACS works, its impact on financial stability, and key considerations for navigating GACS-backed deals, including true sale structures and credit enhancement.

DDTalks provides authoritative insights into European private credit, NPL, and structured finance markets. Our content reflects the expertise gained from hosting premium B2B financial conferences, facilitating high-value deal-making and industry networking among top-tier institutions.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

What is GACS? Defining Italy’s NPL Guarantee Scheme

GACS (Garanzia sulla Cartolarizzazione delle Sofferenze) is an Italian state guarantee scheme to facilitate the disposal of non-performing loans (NPLs) from bank balance sheets. It de-risks the senior tranches of NPL securitisations, making them more attractive to institutional investors and creating a viable market for these distressed assets.

The scheme was introduced in 2016 to help Italian banks clean up their balance sheets without direct state bailouts. By providing a government backstop on the least risky portion of securitised NPL portfolios, GACS bridges the valuation gap between what banks will sell for and what investors will pay. This mechanism is central to managing the gacs italian npl securitisation market.

The Genesis of GACS: Addressing Italy’s NPL Crisis

After the 2008 financial and Eurozone sovereign debt crises, Italian banks accumulated non-performing loans. At its peak, Italy’s gross NPL stock exceeded €340 billion, weighing on bank profitability, capital ratios, and lending capacity. This systemic risk prompted regulatory action from the European Central Bank (ECB) and Italian authorities, requiring a structural solution. GACS was created to accelerate deleveraging by stimulating a secondary market for distressed debt to restore financial stability in Italy’s banking sector.

How Does GACS Work in NPL Securitisation?

The GACS mechanism uses a true sale securitisation for NPLs. An originating bank sells an NPL portfolio to a legally separate Special Purpose Vehicle (SPV). The SPV finances the purchase by issuing asset-backed securities (ABS) to investors. These securities are divided into different risk categories, or tranches.

The government guarantee applies only to the senior tranche, the safest class of notes with first priority on cash flows from the NPL recovery process. The riskier mezzanine and junior tranches absorb initial losses and are typically retained by the originating bank or sold to specialist distressed debt investors. This structure provides credit enhancement to the senior notes, making them suitable for conservative investors like insurance companies and pension funds.

The Securitisation Structure: Tranches and Guarantees

A typical GACS transaction has three tranches. The junior tranche absorbs losses first, followed by the mezzanine tranche. The senior tranche faces potential principal loss only after these are wiped out. The state guarantee on the senior notes is a conditional, first-loss guarantee triggered only after the servicer completes the recovery process on the underlying loans. Rating agencies are crucial, as their assessment determines the senior tranche’s size and rating, a prerequisite for the guarantee.

Eligibility Criteria and Regulatory Oversight

To qualify for GACS, a securitisation must meet specific criteria. The senior tranche must obtain an investment-grade credit rating (BBB- or higher) from an independent, ECB-accepted rating agency before applying the state guarantee, ensuring a baseline portfolio quality. The transaction must also be a “true sale,” transferring the NPLs and their associated risks off the bank’s balance sheet. The scheme is supervised by the European Commission, which has approved its extensions after verifying compliance with EU state aid rules, ensuring the guarantee is priced at market rates.

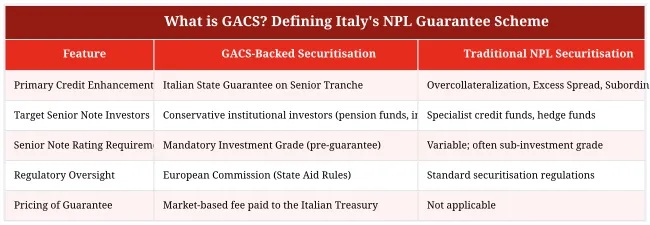

View data as table

| Feature | GACS-Backed Securitisation | Traditional NPL Securitisation |

|---|---|---|

| Primary Credit Enhancement | Italian State Guarantee on Senior Tranche | Overcollateralization, Excess Spread, Subordination |

| Target Senior Note Investors | Conservative institutional investors (pension funds, insurers) | Specialist credit funds, hedge funds |

| Senior Note Rating Requirement | Mandatory Investment Grade (pre-guarantee) | Variable; often sub-investment grade |

| Regulatory Oversight | European Commission (State Aid Rules) | Standard securitisation regulations |

| Pricing of Guarantee | Market-based fee paid to the Italian Treasury | Not applicable |

How Has GACS Reshaped Italy’s NPL Market?

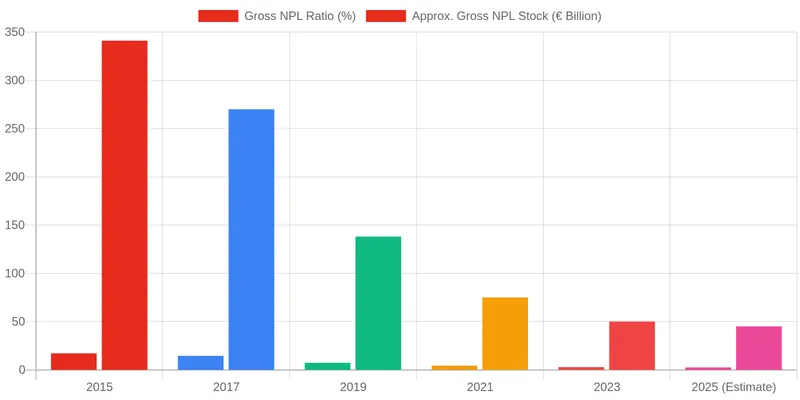

The GACS scheme transformed Italy’s NPL market, helping reduce the gross NPL ratio of Italian banks from 17.1% in 2015 to below 3% by 2024, according to the Bank of Italy. This reduction has strengthened bank capital positions, improved profitability, and enabled new lending.

GACS developed a mature NPL market infrastructure, attracting international investors, specialized legal advisors, and expert servicers. This increased price transparency and liquidity in the secondary market for distressed assets, making Italy’s NPL sector one of Europe’s most active. The gacs italian npl securitisation framework is now a reference for other European nations considering similar support mechanisms.

Driving Down NPL Ratios: A Decade of Transformation

The GACS scheme has guaranteed senior notes on securitisations with a total gross book value (GBV) over €100 billion of non-performing loans. This removal of assets from bank balance sheets drove the sector’s recovery. Specialized servicers manage the process, maximizing recoveries from the underlying loan portfolios—a critical function for the securities’ performance.

View data as table

| Year | Gross NPL Ratio (%) | Approx. Gross NPL Stock (€ Billion) |

|---|---|---|

| 2015 | 17.1% | 341 |

| 2017 | 14.5% | 270 |

| 2019 | 7.3% | 138 |

| 2021 | 4.3% | 75 |

| 2023 | 2.8% | 50 |

| 2025 (Estimate) | 2.5% | 45 |

The Role of AMCO and ‘Bad Banks’ in the GACS Ecosystem

State-owned asset management companies (‘bad banks’) play a significant role. Italy’s AMCO (formerly SGA) is a key player. Although distinct from GACS, AMCO works in parallel, acquiring and managing large NPL portfolios from banks. AMCO has also acted as a servicer or investor in the junior tranches of GACS-backed securitisations, contributing to market stability and providing another channel for NPL resolution.

Beyond GACS: The Future of Italian NPL Securitisation

The GACS scheme has been extended multiple times but is temporary. As the scheme ends, the Italian NPL market is evolving. Focus is shifting from legacy non-performing loans (‘sofferenze’) to other asset classes like Unlikely-to-Pay (UTP) and Stage 2 loans, which have different risk profiles and require more active management and restructuring.

The market’s future will likely involve more private-sector solutions and securitisation structures without a state guarantee. This transition creates challenges and opportunities for investors and servicers, who must adapt to a post-GACS environment. The gacs italian npl securitisation model provides a foundation for this next phase of market development.

Post-GACS Landscape: New Opportunities and Challenges

Without GACS, senior tranche pricing will depend on market appetite and alternative credit enhancement techniques. This creates opportunities for credit funds and specialized investors. The UTP market is notable; these loans are attached to operational borrowers, offering turnaround strategies, not just liquidation. This shift requires blending financial restructuring with industrial expertise. As challenges with Stage 2 loans emerge, new investment theses will be required.

Innovations in European NPL Securitisation Law

European regulatory trends will also shape the future. The EU’s Capital Markets Union initiative and directives for developing secondary NPL markets aim to create an integrated, efficient European distressed debt market. These regulations aim to harmonize legal frameworks, improve data transparency, and facilitate cross-border transactions. As Italy’s market matures, it will align with these pan-European standards, influencing the evolving landscape of NPL securitization in Europe and creating new growth and investment avenues.

Engage with European NPL Experts at DDTalks

Navigating European NPL and distressed debt markets requires access to industry leaders, including GPs, LPs, specialist servicers, and legal advisors. DDTalks hosts closed-door conferences in London and Madrid, providing a platform for networking and deal origination in private credit, structured finance, and NPLs.

Our events deliver insights and facilitate conversations that drive investment strategy. Join peers to discuss the future of NPL securitisation, uncover opportunities in the post-GACS landscape, and build key relationships. To learn more, contact us or Request Agenda for our next event.

Conclusion

The GACS scheme has defined the Italian financial landscape for a decade, enabling banks to de-risk balance sheets and fostering a secondary NPL market. Investor criteria have shifted from relying on the guarantee to analyzing servicer capability and asset quality. As the market prepares for a post-GACS future, participants must develop strategies for UTPs and other credit classes. The critical factor is how private credit enhancement solutions will replace the state guarantee. To stay ahead of these shifts, connect with industry leaders at our forums. Request Agenda or contact us to learn more.

Frequently Asked Questions

What specific criteria must an NPL portfolio meet to qualify for a GACS guarantee?

To be eligible for the GACS guarantee, the underlying non-performing loans must be transferred to a securitisation vehicle (SPV) through a competitive sales process. Furthermore, the senior notes must be assigned a credit rating of at least investment grade (e.g., BBB- or equivalent) from an independent rating agency *before* the application of the state guarantee.

How is the premium for the GACS guarantee calculated to ensure EU state aid compliance?

The guarantee is not a subsidy; originating banks pay a market-rate premium to the Italian Treasury. To comply with European Commission state aid rules, this fee is calculated based on the credit default swap (CDS) spreads of comparable Italian issuers with a credit rating equivalent to the senior notes’ rating. This ensures the pricing reflects market risk and avoids providing an unfair advantage.

By how much did the GACS scheme reduce the gross NPL stock of Italian banks?

The GACS scheme has been a primary driver in deleveraging the Italian banking system. According to the Bank of Italy, from its inception in 2016 until its expiration, the mechanism facilitated the disposal of over €100 billion in gross non-performing exposures, significantly improving bank balance sheets and capital ratios.

What performance triggers can lead to the GACS guarantee on senior notes being enforced?

The guarantee is typically triggered by a failure to meet specific performance covenants outlined in the deal documentation. A key trigger is the Cumulative Collection Ratio (CCR), which measures actual cash collections against an expected business plan. If the CCR falls below a pre-defined threshold for a sustained period, it can constitute an event of default and allow senior noteholders to call upon the state guarantee.

Does the GACS scheme cover Unlikely-to-Pay (UTP) loans?

The original GACS framework was designed exclusively for the securitisation of classified bad loans (sofferenze). While there have been subsequent discussions and legislative efforts to create similar mechanisms for Unlikely-to-Pay (UTP) portfolios, the classic gacs italian npl securitisation scheme was not directly applicable to UTPs, which require a different, more active servicing approach.

What happens to the riskier junior and mezzanine tranches in a GACS deal?

The government guarantee applies exclusively to the senior tranche of the securitisation. The riskier mezzanine and junior tranches must be sold to private market investors without any state support. This structure ensures that private capital bears the first-loss risk, aligning investor interests with the effective workout of the underlying NPL portfolio.

0 Comments