Managing Currency Risk: Safeguarding Returns in European Credit

Managing currency risk is essential for institutional investors navigating multi-jurisdiction European private credit deals. This article details strategies for mitigating foreign exchange (FX) exposure, including forward contracts, currency swaps, and multi-currency facility structuring. It explains how to protect investment value against adverse rate movements in key pairs like EUR/GBP and EUR/CHF. Understanding transactional exposure and implementing robust FX hedging programs are critical for safeguarding returns and stabilizing transactions across diverse European markets, from the UK to the DACH region.

DDTalks specializes in B2B financial conferences, providing platforms for industry leaders to discuss critical topics like private credit, NPLs, and structured finance. Our events facilitate high-value deal-making and offer insights into complex financial challenges, including effective currency risk management.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

Managing currency risk is critical for institutional investors and fund managers in multi-jurisdiction European private credit deals. Adverse foreign exchange (FX) rate movements can erode returns and destabilize transactions. This article explains currency exposure in the European market, outlines hedging strategies like forward contracts and swaps, and details how to structure credit facilities and risk frameworks to protect investment value.

Understanding Currency Risk in European Private Credit Deals

Currency risk in European private credit is the potential for investment losses from exchange rate fluctuations. This exposure occurs when a fund’s base currency, like the Euro (EUR), differs from the loan’s currency, like the British Pound (GBP) or Swiss Franc (CHF). An adverse rate movement between funding and repatriation can diminish interest income and principal returns, impacting fund performance.

What is Foreign Exchange Risk in Private Credit?

Foreign exchange (FX) risk is the mismatch between a fund’s capital commitment currency (e.g., EUR) and its loan currency (e.g., GBP). For example, if a Euro-denominated fund lends in British Pounds, a depreciating GBP means interest and principal repayments are worth less when converted to Euros. This transactional exposure is a primary concern in direct lending.

Key currency pairs introducing this risk in European deals include EUR/GBP, EUR/CHF, and EUR/SEK, each influenced by distinct monetary policies and economic factors. Their volatility requires management to safeguard investor returns.

Why European Multi-Jurisdiction Deals Amplify FX Exposure

Pan-European investing magnifies currency exposure. A fund operating across Europe may have assets in the UK, Switzerland, the Nordics, and Central and Eastern Europe (CEE), while domiciled in a Eurozone country like Luxembourg or Ireland. Each jurisdiction’s currency creates multiple layers of FX risk within a single portfolio.

Varying economic cycles, interest rate differentials, and political events across regions like Iberia, the DACH region, and France compound this complexity. A diversified portfolio, while beneficial for credit risk, creates complex currency exposures that require sophisticated risk mitigation.

Key FX Hedging Strategies for European Private Credit

To counter currency volatility, fund managers use hedging strategies, typically derivative instruments that lock in exchange rates or protect against adverse movements. Instrument choice depends on the deal’s duration, cost, and the fund’s risk appetite.

Forward Contracts and Currency Swaps Explained

A forward contract is an agreement to buy or sell a foreign currency on a future date at a predetermined exchange rate. It is effective for hedging known future cash flows, like a scheduled interest or principal payment. Locking in the rate eliminates uncertainty about the future cash flow’s value in the fund’s base currency.

A cross-currency swap is used for longer-term exposures, like the entire life of a loan. In a swap, two parties exchange principal amounts in different currencies at the start and reverse the exchange at maturity. During the loan’s term, they also exchange fixed or floating interest payments in their respective currencies. This transforms a foreign-currency loan into a base-currency loan for the fund.

Exploring Natural Hedges and Currency Options

A natural hedge is when a fund’s assets and liabilities are in the same foreign currency. For example, a fund might raise capital from UK-based Limited Partners (LPs) in GBP to finance a loan to a UK-based company. Matching inflows and outflows in the same currency mitigates net exposure to EUR/GBP fluctuations. Creating perfect natural hedges across a diverse portfolio is operationally challenging.

Currency options offer flexibility. A currency option gives the holder the right, but not the obligation, to buy or sell a currency at a specified price (the strike price) on or before a certain date. Unlike a forward contract, it is not an obligation. Options provide downside protection while allowing the fund to benefit from favorable currency movements, but this flexibility costs an upfront premium.

Structuring Multi-Currency Facilities & Hedging Programs

Mitigating currency exposure requires deal-level structuring and a fund-level risk management framework. Flexible credit facilities and a clear hedging policy allow managers to address FX risk systematically across their portfolios.

Designing Effective Multi-Currency Credit Facilities

A multi-currency facility is a loan agreement allowing a borrower to draw funds in several pre-agreed currencies. This structure benefits both borrower and lender. For the borrower, it provides operational flexibility to match funding with revenue streams in different countries. For the lender, it centralizes currency exposure management. Loan documentation specifies the mechanics for drawing, repaying, and calculating interest in each currency, often with clauses that pass hedging costs to the borrower.

The table below compares common hedging instruments used within these facilities.

Implementing an FX Risk Management Framework

An effective FX risk management framework involves several key steps:

- Policy Definition: Establish a clear policy defining the fund’s risk tolerance, hedging objectives, and approved instruments.

- Exposure Identification: Identify and quantify all currency exposures across the portfolio regularly.

- Strategy Selection: Choose appropriate hedging tools based on the exposure’s nature and duration.

- Execution and Monitoring: Execute hedges with approved counterparties and monitor their effectiveness against market movements.

Developing these European private credit risk management frameworks is a core competency for cross-border lenders.

Costs, Covenants, and the Bottom Line of FX Hedging

Hedging reduces risk but has costs. An analysis requires weighing the direct and indirect costs of hedging against potential losses from unhedged currency exposure. Currency movements can also impact loan covenants.

Analyzing the Costs and Benefits of Hedging Strategies

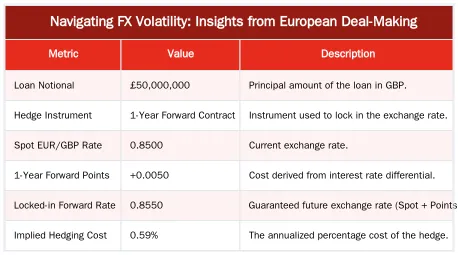

The cost of a forward contract is embedded in the forward rate, determined by the interest rate differential between the two currencies—known as interest rate parity. Other costs include transaction fees and the bid-ask spread. For swaps and options, collateral requirements can tie up capital. The key is to evaluate whether the cost of this “insurance” is justified by the risk being mitigated. A cost-benefit analysis is required for each transaction.

The table below illustrates a simplified cost analysis for a hypothetical hedge.

How Currency Fluctuations Impact Loan Covenants

Adverse currency movements can cause a borrower to breach loan covenants. Financial covenants, such as Debt-to-EBITDA or interest coverage ratios, are often calculated in the borrower’s local currency. If the debt is denominated in a foreign currency (e.g., EUR debt for a UK company), a weakening of the local currency (GBP) inflates the debt’s value on the balance sheet. This can cause a covenant breach, triggering default clauses. Proactive cross-border deal structuring must account for these dynamics by setting covenant levels with sufficient headroom for currency volatility.

Mitigate Risk & Maximize Returns at Our Conferences

The topics discussed here are central to the discussions at our European private credit conferences. We bring together GPs, LPs, and financial advisors to share solutions and form strategic partnerships.

Connect with decision-makers in European credit. To learn about our upcoming events in London, Madrid, and other financial hubs, contact us or Request Agenda for our next private credit forum.

Conclusion

Managing foreign exchange exposure in European private credit is necessary to preserve returns and portfolio stability. By understanding risk, using hedging instruments like forwards and swaps, and embedding risk management into deal structuring, fund managers can navigate cross-border complexities. The strategies outlined provide a framework for protecting capital against currency market volatility. To further your expertise, explore our upcoming events. Request Agenda today.

Frequently Asked Questions

What is the most common method for managing currency risk in European private credit?

The most common approach involves using derivative instruments like forward contracts and currency swaps. A forward contract locks in a future exchange rate for a specific transaction, while a cross-currency swap can exchange principal and interest payments in different currencies over the loan’s term. These tools are fundamental for managing currency risk and providing return certainty.

How does a ‘natural hedge’ contribute to managing currency risk in a multi-jurisdiction deal?

A natural hedge occurs when a fund’s revenues and costs are in the same foreign currency, reducing exposure without derivatives. For example, a EUR-denominated fund can borrow in GBP to finance a UK-based asset that generates revenues in GBP. This strategy of matching assets and liabilities in the same currency is a core principle of managing currency risk effectively.

How do multi-currency facilities help with managing currency risk?

A multi-currency facility is a credit line that allows a borrower to draw funds in several pre-agreed currencies. This provides significant operational flexibility, enabling the borrower to match the currency of its debt with its revenue streams. By doing so, it directly reduces foreign exchange exposure and simplifies the process of managing currency risk across different European jurisdictions.

Who typically bears the cost of FX hedging in a private credit transaction?

The cost of hedging is a key negotiation point but is most often borne by the borrower. Lenders require hedges to be in place to protect their returns in their base currency. These costs are then factored into the borrower’s overall cost of capital as a necessary expense for mitigating foreign exchange volatility.

How does foreign exchange volatility affect the value of collateral?

When collateral is located in a different currency jurisdiction from the loan, its value can fluctuate significantly due to FX movements. Lenders mitigate this risk by requiring higher over-collateralization, resulting in a lower loan-to-value (LTV) ratio. They may also include specific covenants that can be triggered by adverse currency shifts to protect the lender’s position.

Where can I learn more about advanced strategies for mitigating currency exposure?

To gain deeper insights from industry leaders on this topic, you can explore the agenda for our upcoming European private credit conferences. Our expert-led panels cover detailed strategies for navigating FX volatility and structuring resilient deals. You can request the full agenda to see the specific sessions and speakers.

0 Comments