Predictive Analytics Loan Recovery: Optimizing Distressed Asset Returns

Predictive analytics loan recovery frameworks empower financial institutions to enhance risk assessment and optimize collection strategies for non-performing assets. These advanced models leverage historical data and machine learning algorithms to forecast recovery outcomes, significantly improving portfolio performance. By applying data mining and recovery rate modeling, institutions can accurately estimate expected cash flows from distressed debt and NPL markets. This proactive approach ensures efficient resource allocation and maximizes returns, moving beyond traditional credit scoring methods.

DDTalks specializes in European private credit, NPL, and distressed debt markets, providing insights from leading industry experts. Our conferences facilitate high-value deal-making and strategic discussions on advanced financial analytics.

To explore your options, contact us to schedule your consultation. You can also reach us via: Request Agenda

Predictive analytics loan recovery frameworks provide financial institutions with precise risk assessment, optimized collection strategies, and improved portfolio performance. These frameworks use historical data and machine learning algorithms to forecast recovery outcomes for non-performing assets, with applications in European distressed debt and NPL markets.

What is Predictive Analytics for Loan Recovery and Why Does it Matter?

Predictive analytics for loan recovery applies statistical algorithms and machine learning to historical data to forecast the likelihood and amount of funds recoverable from non-performing loans (NPLs). It enables a proactive, data-informed strategy that optimizes resource allocation and maximizes returns from distressed assets.

Defining Loan Recovery Forecasting with Advanced Analytics

Loan recovery forecasting uses analytical models to analyze datasets containing borrower information, loan characteristics, payment histories, and macroeconomic factors. By identifying patterns preceding successful recoveries, these models predict future outcomes. This allows institutions to estimate recovery rates for loans or portfolios with greater accuracy than traditional methods.

The Strategic Imperative for Financial Institutions and Servicers

Accurate forecasting improves capital allocation by clarifying expected cash flows from distressed assets. It also reduces operational costs by directing collection efforts toward accounts with the highest probability of recovery. Technology’s role in modern NPL servicing, including AI and data analytics, is fundamental to achieving these efficiencies and enhancing risk management frameworks.

How Do Predictive Analytics Models Forecast Loan Recovery?

Predictive loan recovery forecasting is a structured process that transforms raw data into actionable intelligence. It aggregates data to create a validated model for operational workflows. Success depends on data quality and appropriate model selection.

Essential Data for Accurate Recovery Forecasting

Predictive models require comprehensive, high-quality data. Key data sources include:

- Historical Loan Performance: Data on past defaults, payment history, interest rates, loan-to-value (LTV) ratios, and original loan terms.

- Borrower Information: Demographics, credit scores (e.g., FICO), income levels, and employment history.

- Collection Activity Logs: Records of all past collection attempts, including communication channels, timing, and outcomes.

- Collateral Data: For secured loans, information on asset type, valuation, and location is critical.

- Economic Indicators: Macroeconomic data such as unemployment rates, GDP growth, and interest rate trends, which can influence recovery rates.

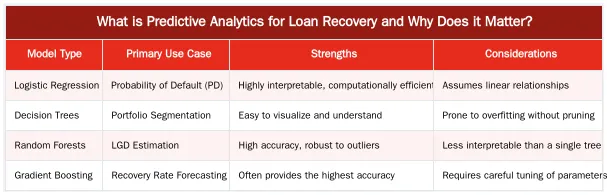

Key Machine Learning Models for Recovery Rate Modeling

Several machine learning models are used for recovery rate and Loss Given Default (LGD) modeling. Model choice depends on business objectives, data complexity, and interpretability needs.

Optimizing Collection Strategies with Predictive Insights

Predictive analytics refines and personalizes collection strategies. This data-driven approach improves servicer efficiency and effectiveness for professionals managing distressed debt portfolios.

Dynamic Portfolio Segmentation for Targeted Action

Predictive models enable dynamic portfolio segmentation, grouping loans by predicted recovery potential. Servicers can create distinct segments:

- High Recovery Potential: Borrowers likely to self-cure or respond to light-touch communication (e.g., automated reminders).

- Moderate Recovery Potential: Accounts that require more intensive, personalized contact from collection agents.

- Low Recovery Potential: Loans where recovery is unlikely, which may be prioritized for sale, legal action, or write-off.

This segmentation enables strategic resource allocation, focusing intensive efforts where they yield the highest return.

Enhancing Loss Given Default (LGD) and Probability of Default (PD) Accuracy

Regulatory frameworks like Basel III require financial institutions to maintain accurate models for Loss Given Default (LGD) and Probability of Default (PD). Predictive analytics enhances these models by incorporating more variables and identifying non-linear relationships that traditional statistical methods might miss. Accurate LGD and PD estimates lead to better risk-based pricing, loan loss provisioning, and capital adequacy calculations. This directly builds more effective recovery strategies for banks and servicers.

Navigating the European NPL Landscape with Advanced Analytics

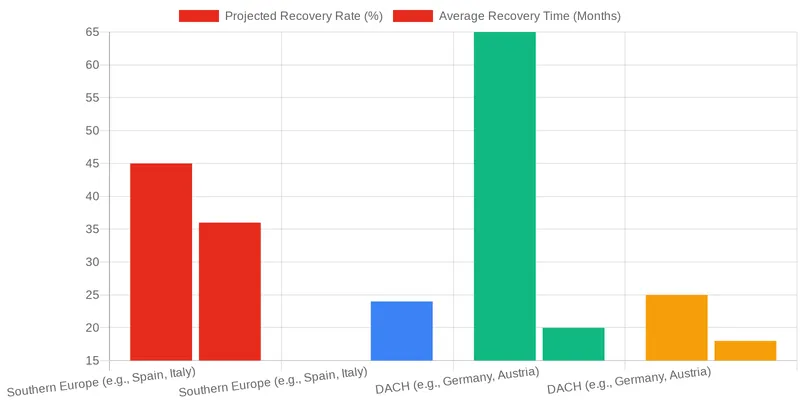

Applying predictive analytics in the European non-performing loan market requires understanding its fragmented nature. Successful implementation depends on adapting models to diverse regulatory and economic environments across the continent.

Regional Nuances in Data and Recovery Models Across Europe

Varying legal frameworks, data privacy regulations (like GDPR), and economic conditions across jurisdictions like the Iberian Peninsula, the DACH region, and Central Europe influence model effectiveness. The legal process for collateral repossession in Spain, for example, differs from Germany, impacting recovery timelines and outcomes. According to the European Banking Authority (EBA), these differences necessitate region-specific models over a pan-European approach.

Predictive Analytics as a Deal-Making Enabler in Distressed Markets

Predictive analytics is a critical tool for due diligence and deal-making. When evaluating NPL portfolios for acquisition, these models provide data-backed valuations and forecast potential returns under various economic scenarios. This analytical rigor supports more confident bidding and deal structuring. Leveraging AI and analytics for smarter NPL management is a strategic asset for identifying and capitalizing on investment opportunities in distressed markets.

Implementing a Predictive Analytics Framework

A successful predictive analytics loan recovery program requires the right technology, skilled personnel, and a clear governance structure. The process is iterative, involving continuous refinement and validation to keep models accurate and relevant.

Key Steps for Successful Implementation

A phased approach is effective for implementation:

- Define Business Objectives: Articulate goals, such as improving collection efficiency, enhancing LGD models, or valuing NPL portfolios.

- Establish Data Infrastructure: Consolidate data from disparate sources into a clean, accessible repository.

- Model Development and Validation: Select, train, and test machine learning models on historical and out-of-sample data.

- Deployment and Integration: Integrate validated models into operational systems like collection platforms or risk management dashboards.

- Monitoring and Iteration: Monitor model performance against actual outcomes and recalibrate as new data becomes available or market conditions change.

Overcoming Challenges in Data Integration and Model Governance

Common hurdles include poor data quality, siloed information systems, and regulatory compliance. A model governance framework is essential to address these challenges. This includes documenting data lineage, ensuring model interpretability (“explainability”), and establishing protocols for model validation and updates. Adherence to data privacy laws, particularly in Europe, is a critical consideration.

Unlock Deeper Insights at DDTalks European Financial Conferences

Advanced analytics in distressed debt and private credit is a central theme at our B2B financial conferences. Our events provide a platform for institutional investors, NPL servicers, and workout professionals to engage with industry leaders from firms like Blackstone, Ares Management, and Goldman Sachs. Join us to explore trends, network with decision-makers, and discover how data-driven strategies are shaping European debt markets.

Conclusion

Predictive analytics for loan recovery is essential for financial institutions. By using historical data and machine learning, organizations can create accurate forecasts, optimize collection strategies with dynamic segmentation, and make informed decisions in the European NPL market. This capability enhances operational efficiency and provides an advantage in portfolio valuation and deal-making. To connect with experts driving these innovations, explore our upcoming events. For more information, contact us or Request Agenda for our next conference.

Frequently Asked Questions

What is the first step in implementing predictive analytics loan recovery?

The foundational step is data aggregation and preparation. This involves gathering historical data on loan performance, borrower characteristics, and past collection activities, then cleaning and structuring this data to be suitable for training machine learning models.

How does predictive analytics loan recovery improve upon traditional forecasting methods?

Unlike traditional methods that rely on simpler metrics, predictive analytics loan recovery uses machine learning to identify complex, non-linear patterns across hundreds of variables. This results in more granular and accurate forecasts of recovery likelihood, timing, and amounts for distressed assets within NPL portfolios.

What machine learning models are used for predictive analytics loan recovery?

Common models include logistic regression for predicting the probability of any recovery and more advanced algorithms like gradient boosting, random forests, and neural networks. These sophisticated models are used to forecast the actual recovery amount or timing with greater precision, which is critical for portfolio valuation.

How can institutions use forecasts to optimize NPL workout strategies?

Institutions use insights from predictive analytics loan recovery to segment NPL portfolios and apply tailored strategies. For example, high-probability recovery accounts can be managed with automated systems, while low-probability, high-value accounts are assigned to specialized workout teams, optimizing resource allocation.

Why is model validation essential for loan recovery forecasting?

Model validation is critical to ensure a predictive model is accurate, reliable, and not just fitted to past data, a problem known as overfitting. It involves testing the model on a separate, unseen dataset to confirm its predictive power before it is deployed for operational decision-making.

How can I learn more about applying these strategies to European NPL markets?

To gain deeper insights from industry leaders on implementing advanced analytics for distressed debt, you can explore the topics covered at our specialized forums. You can request the agenda for our upcoming European NPL and Distressed Debt events to see the full program.

0 Comments